Many a times you get so engrossed in fulfilling your social and business obligations that you completely ignore the importance of planning for your future needs. To be sure, planning for your future is as important as providing for your current requirements. So what are the future events you need to plan in advance? The most obvious answers to this question would be - buying a house, or providing for your childs education and marriage or even planning for a foreign tour. While there is no denying that all these events are important and must be pre-planned; there is another very important financial planning activity, and evidently the most overlooked one i.e. planning for your retirement.

The main reason why retirement planning is normally overlooked could be that, people typically find solace in their savings. Yes, you might have saved a bulk of money in your banks savings account and in fixed deposits. You might also have investments in some avenues like stocks and mutual fund schemes. And then, if you are salaried, there is the added windfall on retirement in the form of your Employee Provident Fund (EPF). But whether these savings and investments will be enough to cater to your needs after you retire, is what you have to ascertain.

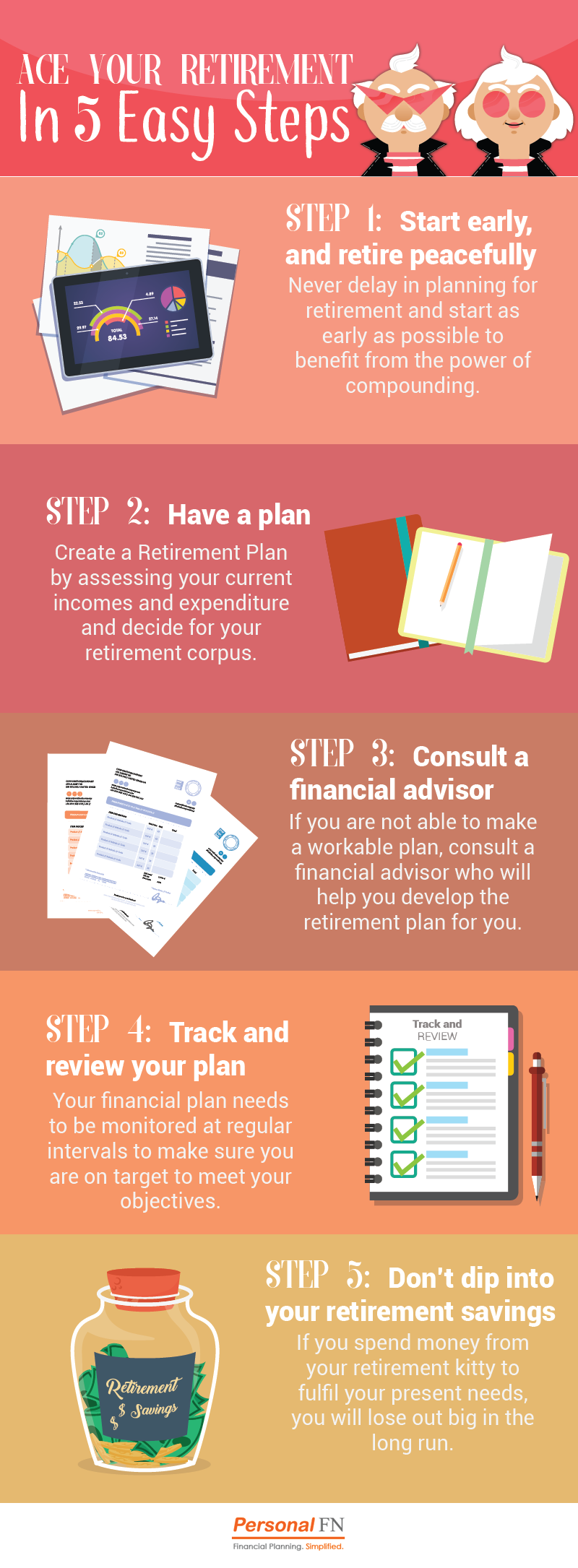

We outline 5 steps, which can help you determine the amount that will be required by you to take care of your post-retirement needs.

Step 1: Decide the age at which you wish to retire

While the most common retirement age is 60 years, it actually depends a lot on you. You may want to work beyond 60 years of age or conversely may wish to retire at 55; basically its a matter of choice. Estimating your retirement age is an important step because after this age your regular income stream will stop or at least reduce considerably (in case you are eligible for pension) and you have to depend on your savings and investments to take care of your needs.

Once you have zeroed in on your retirement age, deduct it from your current age; the purpose is to find out the years left for your retirement. This is also the timeframe you are left with to plan for retirement. For instance, if you are 25 years old at present and you plan to retire at the age of 50 years, you have 25 years (50 less 25) to plan for retirement.

Step 2: Determine your post-retirement expenses

If you haven’t provided yourself with enough money at the time of retirement, it is bound to impact your post-retirement lifestyle. So its important that you make an accurate estimate of how much amount you will require, to maintain your present lifestyle after you retire. For this, first ascertain your annual expenses at present. Then factor in inflation to calculate how much your present expenses will amount to at the time of retirement. This is the amount you will need every year to meet your post-retirement expenses.

Assume that your present annual expenses amount to Rs 120,000. If you have 25 years to retire and expect the rate of inflation to be around 7%; then after adjusting for inflation, your annual expense then will be approximately Rs 651,292.

Step 3: Get a check on your annual savings and find their future value

How much you are able to save every year, after meeting all your expenses, plays a crucial role in building your retirement corpus. Your saving is the surplus amount that is left after deducting your annual expenses from your net salary. The ideal way is to earmark a portion of your savings towards retirement. This part of your saving should be treated as sacred and should not be disturbed unless it is very urgent.

After estimating how much amount you will be able to save annually towards your retirement corpus, the next step is to find out its future value. To determine this, you have to factor in the expected rate of return on your investment. This is the value of your savings or investments at the time of retirement. For instance, if you are able to save Rs 100,000 annually for your retirement, and you invest this amount in an avenue, which earns you 10% rate of return p.a., then after 25 years (which is the number of years left for retirement), you will have a retirement corpus of approximately Rs 9,834,706.

Step 4: Find out whether your savings can cater to your post-retirement expenses

To extend the above illustration, let us assume that you invest your retirement corpus (in this case Rs 9,834,706) to generate a post-retirement income. The investment is made in an avenue that offers, say, 10% rate of return annually (rate of return may vary depending on your choice of investment avenue). So, at the end of every year, you will receive Rs 983,471 as return from your investment. This is your post-retirement income from your investments.

If your post-retirement income is higher than your post-retirement expenses (in this case Rs 651,292, from Step 2), your savings/investments are enough to cater to your post-retirement needs. But if they are lower, then you have to make prior arrangements to plug this shortfall.

Step 5: Engage the services of a financial planner

Admittedly, the above steps may appear confusing and complicated to the average individual. However, they aren't all that difficult if they are conducted with the help of an honest and competent financial planner. Your financial planner should be able to come up with a relatively accurate retirement corpus, which can help you negotiate retirement. More importantly, he can advise you, based on your risk profile, how you can go about investing your savings so that you can achieve your retirement corpus.

Investors who want a step-by-step feel of retirement planning can visit Personalfns retirement calculator. The calculator works based on the steps explained above and gives all the information, necessary for your retirement planning.

Finally, remember that in the process of determining your retirement corpus, you have to make few crucial assumptions such as rate of inflation or rate of return on your investments. These factors are not fixed and are bound to fluctuate over time, thus impacting your calculation. Besides, aspects like how much you can save or spend every year is also subject to fluctuations. With an increase in your salary, your saving and spending capacity also increases. For this reason you must regularly review your calculations to ensure that you are always on track to achieve your retirement corpus. Hopefully, your financial planner is well prepared to help you with this.

Add Comments