Abhay (age 30) is planning to buy a term insurance plan. He believes as he grows older his responsibilities would increase. He plans to buy a house, marry his college sweet heart and start a family. He is looking for a term insurance plan with an option to increase his life coverage with time.

Here's a plan which Abhay can look at: - Aegon Life's iTerm Insurance

Recently the plan was reintroduced and here are some of its features:

| Features |

Details |

| Financial security to family in his absence |

- Choice of Life cover till the age of 80 years;

- Flexibility to opt for the whole or part of the total death benefit pay-out as regular monthly income;

- Flexibility to opt for a part of/whole of the death benefit pay-out as a lump-sum benefit to take care of immediate liabilities and expenses

|

| Increase in life insurance coverage as per increasing life stage responsibilities |

- Option to increase your life cover on marriage (50% of original total sum assured), and

- On birth / adoption of child (25% of the original total sum assured on the birth/adoption of 1st child and 2nd child)

Note: The Policy Premium payable shall be increased by the premium corresponding to the Additional Sum Assured. |

| Flexible premium payment |

- Pay premiums every year or in a lump-sum as Single premium;

- Pay your yearly premiums either Annually, Semi-annually or Monthly

|

| Additional protection against Accident, Terminal illness, Critical illness and Disability |

- Inbuilt Terminal illness benefit;

- Additional coverage by choice of add-on riders.

Note: On diagnosis of any terminal illness (as defined under section I.3 of the policy document), an amount equal to 25% of the Total Sum Assured will be paid immediately as a lump-sum. Later the total death benefit will be reduced by the amount equal to the benefit paid under this clause. |

| Tax benefits |

The premiums paid and benefits received are eligible for tax benefits under Section 80(C) and Section 10(10)D, upon fulfilment of the conditions laid down for availing such benefits |

(Note: The table is for illustration purpose only)

(Source: PersonalFN Research)

To explain further,

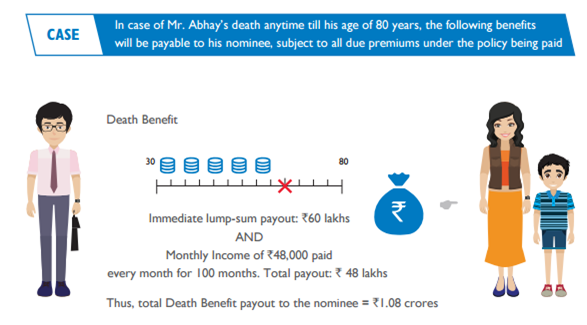

Mr Abhay is a 30 year old non- smoker. His plan details were:

- Total Sum Assured: Rs 1 Crore

- Lump-sum sum assured: Rs 60 lakhs

- Income benefit sum assured: Rs 40 lakhs

- Policy Term: 50 years (coverage till age 80 years)

- Premium Payment Term: 50 years

- Annualized Premium: Rs 8,676 (excluding taxes and cess)

- Monthly premium: Rs 755 (excluding taxes and cess)

(Source: Brochure of Aegon Life iTerm Insurance Plan)

In case of death of the Life Assured during the policy term, provided all due Premiums have been paid, the nominee will receive the Total Sum Assured which shall be payable in the following manner:

- Lump-sum Sum Assured will be paid immediately

- 1.2% of the Income Benefit Sum Assured will be paid monthly for 100 months.

At the time of death claim, the nominee will have the flexibility to opt for the Total Sum Assured to be paid in one single lump-sum immediately. The Policy will terminate on payment of the above benefits.

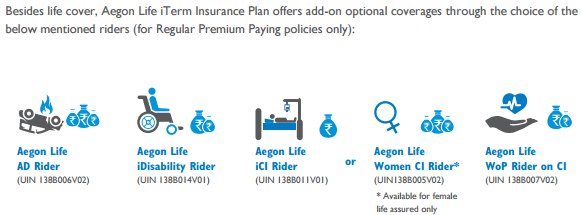

Moreover, the plan offers several add-on optional coverages (riders) as follows:

(Source: Brochure of Aegon Life iTerm Insurance Plan)

The eligibility conditions and additional features are as follows:

| Entry Age |

Minimum - 18 years (last birthday);

Maximum - 65 years (last birthday) |

| Maturity Age |

Maximum - 80 years (last birthday) |

| Policy Term |

Minimum - 5 years and Maximum - 62 years

Policyholder can opt for any Policy Term between 5 years and 62 years, subject to maximum maturity age of 80 years |

| Premium Payment Term |

Single Pay / Equal to Policy Term |

| Total Sum Assured |

Minimum - Rs 25 lakhs;

Maximum - No limit, subject to underwriting |

| Premium Payment Mode |

Single, Annual, Semi-Annually and Monthly |

| Surrender Benefit |

Only available for Single Pay (lump sum premium) |

| Maturity Benefit |

Not Available |

(Note: The table is for illustration purpose only)

(Source: PersonalFN Research)

To Conclude…

At the outset, the product looks appealing and seems efficient in terms of cost to benefit. A pure term insurance plan with a lump sum death benefit pay-out option is advisable. The aim here is to give the nominee the option to invest the proceeds as per his/her need.

But, at PersonalFN we believe that it would be wise not to commingle your life insurance cover with your general insurance cover, and likewise

opt for a critical illness insurance plan and personal accident plan separately. This may give a slight advantage in terms of cost to benefit and choose from promising respective policies.

Add Comments