| S&P BSE Sensex* |

Re/US $ |

Gold Rs/10g |

Crude ($/barrel) |

FD Rates (1-Yr) |

37,556.16 |219.31

0.59% |

68.63 |0.12

0.17% |

29,577.00 | -292.00

-0.98% |

71.80 |-2.23

-3.01% |

5.00% - 7.00% |

Weekly changes as on August 02, 2018

BSE Sensex value as on August 03, 2018

Impact

We might be entering an era of currency wars.

This isn’t a sensational headline published in a business newspaper, but the cautionary voice of the RBI governor.

At the third bi-monthly monetary policy review meet, the RBI governor, Dr Urjit Patel said,

“We have already had a few months of turbulence behind us and it looks like it is likely to continue… for how long I don’t know. But the trade skirmishes evolved into tariff wars and we are possibly at the beginning of currency wars”

The RBI has assured to "run a tight ship on the risks” that it controls– to ensure that India’s macroeconomic stability is maintained even during turbulent times. And it seems to have started marching towards its objective well in time.

At the policy review, RBI retained the GDP growth projection for FY 2018-19 at 7.4%, but the Monetary Policy Committee (MPC) took a decision to hike policy repo rate (policy rates) by 25 basis point (bps) to 6.5%.

The RBI has hiked policy rates in the wake of rising inflation and the chances of it remaining elevated is even in the second half of FY 2018-19.

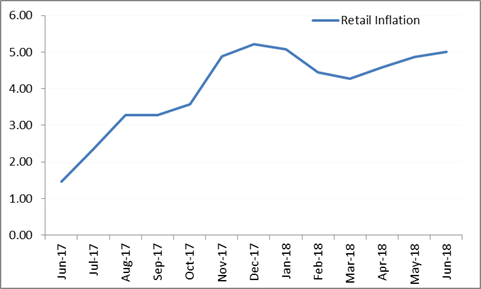

It aims to achieve the inflation target of 4% in the medium term. In comparison to this, the retail inflation, which is denoted by the movement of the Consumer Price Index (CPI), hovered at 5% in June. The retail inflation has been more than 4% from November 2017 onwards.

Inflation heading upwards…

Data as of July 12, 2018

(Data Source: MOSPI)

What is keeping inflation high?

Higher fuel prices (triggered by heated crude oil prices in the international markets), higher housing inflation, and rising prices in the footwear and clothing segment, are some of the reasons for the elevated cost of living for urban and rural masses.

In addition, the implementation of the 7th Pay Commission, which in effect has increased the money supply, too, has pushed inflation up. Higher Housing Rent Allowance (HRA) has resulted in a consistent increase in housing inflation. In June 2018, CPI inflation adjusted for the impact of HRA was 4.6%.

Where does RBI expect inflation to go?

The RBI estimates the CPI inflation-adjusted for the impact of HRA would remain in the range of 4.7% to 4.8% in the second half of FY 2018-19 and would hover at 5% in the first quarter of FY 2019-20.

The impact of higher Minimum Support Prices (MSPs) has already been factored into inflation projections. The sowing area under Kharif crops is 7.5% lower in 2018 as compared to what it was in 2017.

From the beginning of monsoon season this year until July 31, 2018, out of 36 sub-divisions, 28 sub-divisions covering over 80% of India’s total territory received normal or excess rainfall, while only 8 sub-divisions reported deficient rainfall.

Skymet, a private weather forecasting agency, anticipates monsoon to be below-normal this year at 92% of Long Period Average (LPA) of 89 cm, on account of an El Nino phenomenon. So far rainfall across the country has been 94% of LPA.

Taking cues, possibly, even the Indian Meteorological Department (IMD) could downgrade its forecast, although for now, the IMD is hopeful of the precipitation in August and September.

However, due to more water stock at major water reservoirs, Rabi crop season is likely to see increased sowing. But if rainfall isn’t as expected, it will have bearing on food prices and translate into higher retail inflation. Therefore, the RBI is likely to monitor these developments closely.

What’s been the impact of the RBI monetary policy on debt markets?

Even though the RBI has hiked policy rates, it’s been a purely data-driven decision.

On the positive side, the central bank hasn’t changed its stance from neutral to hawkish.

But raising rates successively in two review meetings, also means that the RBI is going aggressively to counter inflation and achieve the inflation target of 4%.

Now, depending on the data collated in the future, the central bank could hit a pause button.

The liquidity position for most part of June and July remained in surplus and the weighted average call rates remained slightly below policy rates.

The yield on India’s 10-year sovereign benchmark bond has also fallen about 13 bps over the last one month. A gradual rise witnessed in the yields post-policy also appears benign.

For now, it looks like debt markets aren’t worried about the liquidity pressures nor are they necessarily sensing any immediate risk to India’s economic progress. That being said, they are cautious about rising inflation and risk to current account deficit and fiscal deficit. These factors suggest that RBI’s policy stance was well-anticipated and well-received by the market.

What should investors do?

Selecting the right category of debt mutual funds is crucial.

PersonalFN is of the view that, one should still be very careful and cautious while investing at the longer end of the yield curve. To put it simply, investing in long-term debt funds (holding longer maturity debt papers) can be risky in the near-term.

Currently, shorter maturity papers are more attractive and fund houses, too, are aligning their portfolio accordingly.

Ideally, you’ll be better off if you deploy your hard-earned money in short-term debt funds; but ensure you’re giving due importance to your investment time horizon, asset allocation, and diversification.

Consider investing in short-term debt funds for an investment horizon of upto 2 years.

If you have an investment horizon of less than 1 year, low duration and money market funds would be the preferred choice.

And if you have an extremely short-term time horizon (of less than 6 months), you would benefit from investing in liquid funds and ultra-short duration funds.

Remember that investing in debt funds is not risk-free.

[Read: 5 Facets To Look Into While Investing In Debt Mutual Funds]

A few highly rated corporate deposits and bonds may also yield better returns than bank FDs. But make sure you study the company’s financials before investing, as the risk of default can’t be ignored. This will save you from financial shocks. Recently a few banks too have increased their deposit rates, so do take note.

[Read: Factors To Look At While Investing In Bank FDs]

A sensible and astute investment strategy paves the path to wealth creation. This is the best for your long-term financial well-being.

|

Editor's note:

Want to know of a time-tested strategy to invest in equities when the Sensex has tested hit its peak?

Looking for “high investment gains at relatively moderate risk”?

Want to invest based on a strategy adopted by some successful investors?

PersonalFN’s “The Strategic Funds Portfolio for 2025” is the answer!

You will get a ready-made portfolio of top equity mutual funds schemes for 2025 that would you multiply your wealth like never before over the long term. Subscribe now!

Here are the key benefits of holding a strategic portfolio brings along:

✔ Your portfolio will be optimally diversified;

✔ Would reduce the need for constant churning;

✔ The risk to your portfolio would reduce;

✔ You can benefit from a variety of investment strategies;

✔ Create wealth cushioning the downside; and

✔ Potentially outperform the market;

To know more about PersonalFN’s Strategic Portfolio For 2025, click here!

Happy Investing!

|

Are You Avoiding Meeting A Financial Planner? You Are Making A Grave Mistake!

Impact

Ashwin is a self-made person. He lost his father when he was 10 years old in a road mishap and mother died of a heart attack when he was 18. Unfortunately, he didn’t have money to treat her at a good hospital.

To complete his graduation and post-graduate studies in science, he worked part-time.

He did an advanced course in IT and secured a high-paying job with a multinational company.

At 35, he owns a house and car, which he bought on loans, and aspires to offer his son all amenities that he always missed. His wife is a teacher with a primary English school and supports the household budget.

Ashwin has a trait that causes him more pain than he realizes — he refuses to ask for help from anyone. Partially, his tough life experiences have made him so, but his “self-made” approach has made him adamant too.

Whenever he falls sick, he avoids going to a doctor. He tries remedies on his own and if he’s still unwell, only then he sees a doctor.

Similarly, he refuses to seek the help of financial planners and takes all investment-related decisions based on his own logic, which is often flawed due to lack of knowledge in financial matters.

To read more, please click here.

Why Gold Is Losing Some Lustre of late?

Impact

People working in a sales department bear the tremendous pressure of achieving targets.

Some employees are as precious as gold to organisations.

With their consistent performance, they not only cement their position in the organisation but they earn a lot of respect as well.

But, none of this is permanent.

Working in the sales department is just like working on daily wages.

If you don’t earn for a day, you might have to survive on what you earned yesterday.

But how about consistently falling short of revenue targets for a year and sitting on zero revenue for the last four months?

Organisations will show even to superstars of yesteryears the door.

At present, investors are playing the role analogous to that of an organisation.

And one of the most ancient asset class, gold, has come under severe pressure—just as a non-performing salesperson.

To read more, please click here.

Will Capping Mutual Fund Commissions Help You?

Impact

At a popular mutual fund brokerage house with a pan-India presence, commissions soared to a massive 78% in FY 2017-18.

On the other hand, the banks grew their revenue from mutual fund distribution in the range of 65% to 140% on a Year-on-Year (Y-o-Y) basis last fiscal.

Did your mutual fund portfolio record such an impressive performance?

Irrespective of how your investments do, mutual fund distributors earn their commissions.

[Read: How Mutual Fund Distributors And Banks Cheat You ]

Radically, mutual funds have gained popularity in 2017, which probably contributed to the sharp spike we’ve witnessed in the commission income of distributors.

To read more, please click here.

Want To Clock Returns Higher Than The Sensex? Read This!

Impact

You may have read some of these shouting headlines “Sensex at an All-Time High”; “Party time on Dalal Street” …and many more enthralling headlines.

But how many of you really make good money or outperforming the benchmark index?

If you aren’t aware, consider this as a wake-up call.

A fact remains that not all stocks and mutual funds have generated wealth in the last few months or years. A number of them have underperformed or displayed a meek performance.

True, no mutual fund scheme can beat its peers consistently. But any scheme that consistently underperforms the benchmark and its peers may not be a suitable one for your portfolio.

To read more, please click here.

New Fund Offer

Axis Equity Hybrid Fund: A Worthy Proposition?

Axis Equity Hybrid Fund (AEHF), a scheme from the stable of Axis Mutual Fund, is an open-ended hybrid scheme investing predominantly in equity and equity related instruments.

Under normal circumstances, AEHF will invest a predominant portion (65-80%) of its asset in equity and equity related instruments (viz. equity shares, equity warrants, foreign equities, equity derivatives, and instrument that give the holder the right to receive equity shares on pre-agreed terms such as convertible preference shares and convertible debentures/bonds).

To read the complete note, click here.

Fund Of The Week

Why HDFC Equity Fund Disappointed Its Investors

HDFC Equity Fund needs no introduction— it's popular with a performance track record spanning more than two decades. However, despite being one of the largest equity funds in India, HDFC Equity Fund is fast losing its charm after a substantial slowdown in performance over the last few years.

Traditionally a flexi-style fund, it has always had the privilege to switch market cap exposure depending on available opportunities. However, the fund preferred to be inclined more towards large caps along with significant exposure to mid-caps. Keeping in mind the fund's historical strategy, the fund house has classified HDFC Equity Fund under Multi-cap Funds category, which allows it to diversify across market caps without limitations to any specific segment. This is very much in line with its historical investment style.

To read the complete note, click here.

Tutorials…

10 Benefits Of Filing Your IT Return On-Time

Best Tax Saving Mutual Fund For 2018-19: Are ELSSs The Best Option?

Financial Terms. Simplified.

Core Inflation: Core inflation is the change in costs of goods and services, but does not include those from the food and energy sectors. This measure of inflation excludes these items because their prices are much more volatile. It is most often calculated using the consumer price index (CPI).

(Source: Investopedia)

Quote: "The Stock Market is designed to transfer money from the Active to the Patient.”‒Warren Buffett