(Image Source: Image by Mediamodifier from Pixabay)

(Image Source: Image by Mediamodifier from Pixabay)

Worrisome news of a higher-than-expected rise in retail inflation has added to the woes in an already ailing economy. The consumer price index (CPI) rose to 7.35% in December 2019, the highest since July 2014 reading of 7.39%.

Food prices, which have around 40% weightage in the CPI basket, rose to 14.12% as compared to -2.65% in December 2018 and 10.1% in November 2019. This increase was mainly driven by sharp rise of 60.5% in vegetable prices. The prices of pulses, meat and fish, and eggs soared as well.

Table 1 : Components of Food Price Index with highest surge in prices

| Description |

Inflation Rate (%) |

| Consumer Food Price Index |

14.12 |

| Vegetables |

60.50 |

| Pulses and products |

15.44 |

| Meat and fish |

9.57 |

| Egg |

8.79 |

| Spices |

5.76 |

| Fruits |

4.45 |

| Milk and products |

4.22 |

Data as of December 2019

(Source: MOSPI)

Factors causing uptick in inflation rate

Unseasonal rains in the month of October and November had damaged vegetable and pulses crop which resulted in the spike in prices.

Crude oil prices surged on expectations that OPEC nations might cut production and easing of US-China trade tensions. As a result, fuel and light inflation rose to 0.7% after contracting in the last four months.

Transport and communication index of CPI spiked by 4.8% due to hike in telecom tariffs.

Prices of other components of CPI such as health, education, personal care, and recreation and amusement have also increased.

Graph 1 : Retail inflation moved up beyond RBI's comfort zone

Data as of December 2019

(Source: MOSPI, RBI, PersonalFN Research)

The inflation has now breached the RBI's comfort zone of 2-6% inflation rate. This is the third consecutive month that CPI has moved beyond the central bank's medium-term inflation target of 4%.

In the 5th bi-monthly monetary policy statement for 2019-20, the RBI had kept the policy rate unchanged at 5.15% and the reverse repo rate at 4.90%, taking cognisance of rising CPI inflation. Further, the MPC decided to continue with the "accommodative stance as long as it is necessary" to revive growth, while ensuring that inflation remains within the target.

Table 2 : Series of policy rate cuts by RBI in 2019 to address growth concerns

| Month |

Repo Policy Rate |

Policy rate cut (Basis points) |

Monetary Policy Stance |

| Feb-19 |

6.25% |

25 |

Neutral |

| Apr-19 |

6.00% |

25 |

Neutral |

| Jun-19 |

5.75% |

25 |

Accommodative |

| Aug-19 |

5.40% |

35 |

Accommodative |

| Oct-19 |

5.15% |

25 |

Accommodative |

| Dec-19 |

5.15% |

Status quo |

Accommodative |

| Total |

|

135 |

|

Data as of December 5, 2019

(Source: RBI)

India's GDP growth came in lower at 5% in Q1 FY 2020 and 4.5% in the Q2 of FY2020. CSO's first advanced estimate has pegged GDP growth at 5% for 2019-20. In order to support growth, the RBI cumulatively reduced policy rates by 135 bps in 2019. Rise in inflation is likely to further hit consumption growth which forms a major part of the GDP.

Though the prices of vegetables are expected to soften due to pick-up in arrivals from the late Kharif season and imports, prices of other food components may remain high. Additionally, revision in rail fares and an anticipated rise in crude oil prices, due to geopolitical risk, are likely to push inflation towards the upper band of the inflation target.

The path to inflation and interest rates...

The future course of policy rate actions by RBI will, of course, depend on the incoming data prints, mainly inflation. The RBI in its last bi-monthly monetary policy statement for 2091-20 mentioned that the inflation outlook is likely to be influenced by several factors:

-

Food inflation, mainly prices of vegetables and pulses

-

Incipient price pressures seen in other food items such as milk, pulses, and sugar are likely to be sustained

-

Inflation expectations of households polled by the Reserve Bank survey

-

Volatility in the domestic financial market

-

Domestic demand

-

Crude oil prices

The MSP (Minimum Support Price) hike announcement for rabi (winter-sown) crops is likely to exert pressure on food inflation. Similarly, the 'fuel & light' category will remain predisposed to the movement in international oil prices.

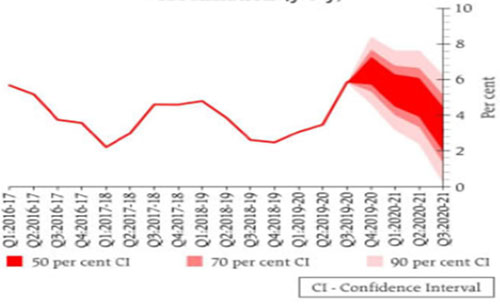

Graph 2 : RBI's quarterly projection for CPI inflation (y-o-y)

(Source: RBI's 5th bi-monthly monetary policy statement for 2019-20)

Taking into consideration the aforesaid factors, the RBI has revised its CPI inflation projection upwards to 5.1-4.7% for H2:2019-20 (from 3.5-3.7% estimated for H2:2019-20) and 4.0-3.8% for H1:2020-21, with risks broadly balanced.

The Union Budget 2019 will be closely watched for its impact on inflation and GDP growth before further monetary policy action. It appears unlikely that the RBI will reduce policy repo rate in its 6th bi-monthly monetary policy statement for 2019-20 (scheduled on February 6, 2020), but it could maintain its accommodative stance.

The RBI observed that though credit market transmission is delayed, it is on the uptake. As per the RBI, the transmission is expected to improve going forward as: (i) the share of base rate loans, interest rates on which have remained sticky, declines; and (ii) MCLR-based floating rate loans, which typically have annual resets, become due for renewal.

After the introduction of the external benchmark system, most banks have linked their lending rates to the policy repo rate of the Reserve Bank ...and this augurs well for transmission to lending rates, as per the RBI.

How to approach debt mutual funds now?

At the outset, we seem to have bottomed out as regards the rate cut cycle, and thus investing at the longer end of the yield curve could prove less rewarding and risky (may encounter high volatility) in the foreseeable future. Most of the rally at the longer end of the yield curve has already come about since the time RBI started reducing policy rates.

However, taking into account that policy repo rates could move either way --- given the "accommodative stance as long as it is necessary" --- maintained by RBI in last monetary statement, allocating a small portion of the debt portfolio to a Dynamic Bond Fund may be considered, provided you are willing to take some extra risk.

A Dynamic Fund holds the mandate to invest across maturity debt papers. The fund manager assesses where interest rates are headed to build the portfolio across the yield curve.

On the other hand, if you are not willing to take extra risk, you'll be better off if you deploy your hard-earned money in shorter duration debt mutual funds. But ensure you approach even short-term debt funds with your eyes wide open and pay attention to the portfolio characteristics and quality of the scheme.

A fact is, many debt mutual funds across maturity profiles are grappling with downgraded and toxic debt papers which heightens the investment risk. So, prefer the safety of principal over returns. Stick to debt mutual funds where the fund manager does not chase returns by taking higher credit risk. Further, assess your risk appetite and investment time horizon while investing in debt funds.

Editor's Note: If you wish to select worthy mutual fund schemes, I recommend you to subscribe to PersonalFN's unbiased premium research service, FundSelect.

Additionally, as a bonus, you get access to PersonalFN's popular debt mutual fund service, DebtSelect.

Each fund recommended under FundSelect goes through our stringent process, where they are tested on both quantitative as well as qualitative parameters.

Every month, PersonalFN's FundSelect service will provide you with insightful and practical guidance on equity mutual funds and debt schemes - the ones to Buy, Hold, or Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Add Comments