Impact

When you go to a shopping mall, the transaction is quite simple. You look for the things you want to buy, check the price tag and offers, and pay the cashier for your purchases. The end. It's hassle-free and the store manager doesn't inquire about your personal details, buying habits, colour preferences, etc.

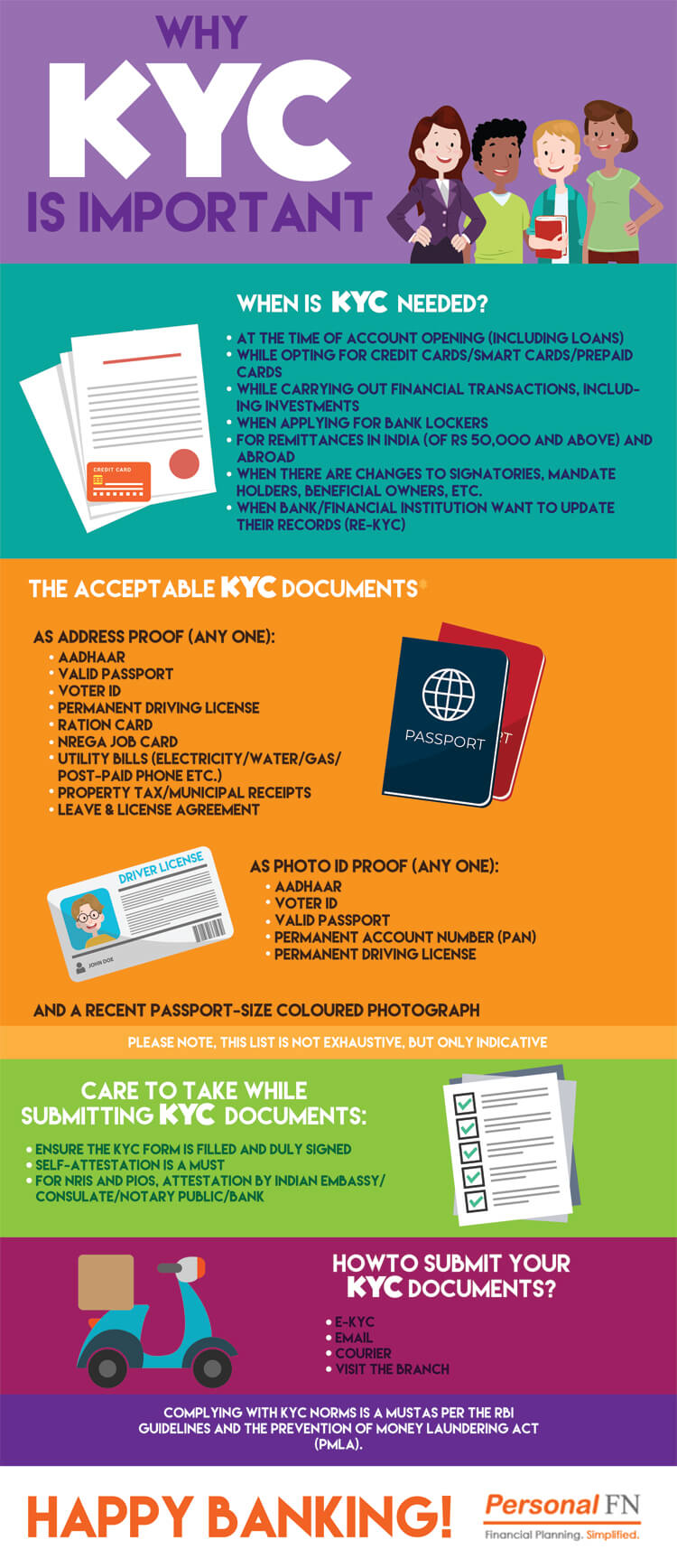

But when you go to a bank or any other financial institution, this includes a mutual fund or an insurance house, you will be asked to divulge bits of personal information. This process is called Know Your Client (KYC). So every institution, from a bank to an insurance company or a stock brokerage house, would like you to be KYC-compliant.

Why KYC?

When a financial transaction is accomplished by money obtained through illegal means or performed as an attempt of avoiding tax; the Government loses revenue. On the other hand, the ownership of any asset obtained by deceiving authorities can be morally hazardous. In brief, the Government has to know the source of money and pattern of ownership for every financial transaction. The KYC records help specifically in this endeavour.

KYC—Evolution and refinement of the process

To begin with, Securities and Exchange Board of India (SEBI) had not provided a specific KYC format. As a result, different intermediaries and manufacturers of financial products were using dissimilar formats. Plugging the loopholes, SEBI standardised the form and processes. It has also centralized the KYC registration through KYC Registration Agencies (KRAs). Furthermore, it's now mandatory for intermediaries and product manufacturers to obtain additional information necessary under uniform KYC guidelines, which were not mandatory to be provided earlier. About 2 years have elapsed since and many KYCs forms are pending due to the requirement of additional information.

Based on information provided to KRAs, KYC statuses can be broadly classified into 7 categories:

- KYC-Registered

- KYC-on Hold

- KYC- Under Process

- KYC- Rejected

- KYC- Not Available

- MF-KYC Registered

- KYC-Deactivated

Currently, there are a number of cases where the KYC records show the status 'on hold'. Mutual funds are allowing investors to transact as long as the status of their KYC status isn’t marked 'rejected'.

Therefore, it is expected that Asset Management Companies (AMCs) should clear up all pending cases by November 01, 2015.

What does this imply for investors?

If your KYC status is anything other than 'KYC-registered', you will be disallowed to buy mutual fund units whether fresh, additional, or through switches.

Supplementary KYC

Besides, under Foreign Account Tax Compliance Act (FATCA) all investors will have to provide information on the following:

- Beneficiary Ownership—'Beneficial Owner' is one who may or may not have the title in his / her name but will enjoy the benefits of ownership.

- The Gross Annual Income earned by an individual

- The Net worth; which is net of all assets,investments reduced by liabilities

The deadline to comply with additional requirements is December 31, 2015. What is noteworthy is the aforementioned KYC details are a part of the common application form and not handled at the KRA level.

PersonalFN is of the view that additional information sought under FATCA will help track the ownership details and sources of funds. Having said this, many investors may be uncomfortable with revealing details such as net worth. The related authorities along with the regulator will have to assure the investors about the non-misuse of information. It remains to be seen how it affects new, fresh investments in mutual funds.

PersonalFN believes frequent changes, although for the good of all stakeholders, may affect the investment environment negatively. This can lead to a climate of ill feeling where investing in financial products could be seen as a hassle. At the moment though, the situation at the grassroots appears fairly positive.

Add Comments

| Comments |

venkat1926@gmail.com

Apr 09, 2016

registering KYC is pain in the neck. The Mutual fund organisations ask self attested copies of documents and ALSO ORIGINAL DOCUMENTS for checking. Of course if you have time to spare you can take the original documents and copies to the nearest branch of mf AMC and get it done. Who has time for this. What about senior citizens. who have the guts to send original documents by post or courier. This procedure becomes more tortuous if the individual is a foreign resident. KYC have to accept self attested copies of documents which I think is the policy of the Government. |

siddharthaguha7@yahoo.com

Nov 07, 2015

Why should FATCA be applicable to us the individual retail investor? I can understand KYC but apart from the Beneficial ownership the other things should be available from other sources.Or is should be made applicable to investments above a certain limit every year. |

1