Anil, a small-time retailer, was taken up with the recent stock market craze. Curious about all the hype, he too wanted to try his hand at investing.

He knew the risks involved and considered investing in less-volatile balanced funds. Recently, he had read that balanced funds were a good option to start with. However, there were so many balanced funds available for investment.

Which one should he choose?

Of course, he knew the importance of analysing performance over multiple periods, check risk ratios and all. But, Anil wanted an easy way out and decided to consult with his elder brother, Mukesh, who was a shrewd businessman and had a better knowledge of investments.

He directed Anil to check the mutual fund star ratings and to invest in 5-star rated funds. Anil, however, was expecting a recommendation. Abruptly, Mukesh suggested Reliance Regular Savings Fund - Balanced Option.

Happy with this information, Anil decided to check the star rating of this balanced fund. He was surprised to see that one mutual fund rating agency rated the scheme’s regular plan 3-star, while the direct plan was rated 4-star. Another rating firm gave both the plans of the balanced fund a 4-star rating. On further research, a well-known credit rating firm gave the fund a 3-star.

This left Anil even more confused. Should he trust the star ratings? If so, which research firm should he trust?

Mutual fund star ratings have always been a bone of contention. While the rating firms stand by their individual methodologies to rank schemes, amateur investors can easily be misled in choosing the wrong fund, by merely looking at the ratings.

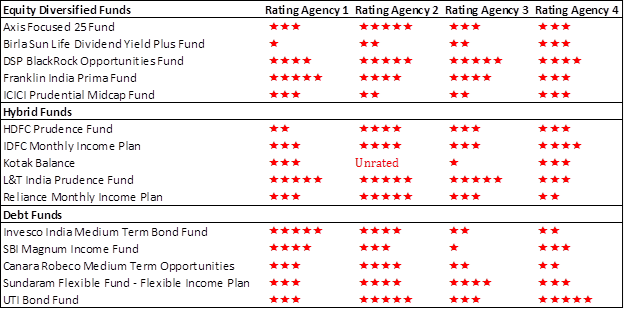

We randomly select different funds, across categories, to check how they were rated across mutual fund rating agencies. Take a look at the difference in ratings below:

Multiple Ratings That Leave You Bamboozled

Data as on July 24, 2017

Note: Data of only regular plans considered

Please do not base investment decisions using this data. Consult an investment adviser.

(Source: PersonalFN Research)

In certain cases, there is a stark contrast in ratings. While some schemes are rated 5-star by one agency, another rating firm has given these a 3-star or 2-star rating. Some rating agencies rank the direct plans and regular plans individually (for some strange reason). Therefore, you may even come across a scheme where the direct plan is rated a 4-star, while the regular plan secures a 3-star by the same rating agency.

The deviance in star ratings is more prominent in debt funds. This difference is mainly because of the weightage given to different parameters. Some agencies may give a higher weightage to risk parameters such as the credit rating of securities in the portfolio and other risk factors, while others may give a higher weightage for performance.

Most of these ratings focus on quantitative parameters such as returns, risk-return trade off, corpus size, portfolio turnover, etc. Some give a high weightage to recent performance or often consider point-to-point returns. But more importantly, most neglect (sometimes completely) the qualitative parameters, which in our opinion, are also of utmost importance.

In order to have a more holistic view of mutual funds, it is imperative that the quantitative as well as qualitative parameters are both considered in the rating process. These qualitative parameters form an inseparable part of the analysis of mutual funds, as the quantitative parameters form the outer layer of a scheme, while the main core of a mutual fund is formed by its qualitative parameters.

Qualitative parameters are able to produce more robust ratings as it takes into account a host of factors mentioned here under, to reflect more consistent performing mutual funds.

Remember, recognising the qualitative parameters go a long way in maintaining the financial health of your portfolio and support wealth creation over the long-term.

Let’s understand the qualitative parameters that add to the long-term investment objective of wealth creation:

- Fund Manager’s experience: Knowing the fund manager’s experience in fund management will be valuable. It is noteworthy that the fortune of the fund will be closely linked to the way he/she manages the fund, and this is a function of the experience that he carries in the field of fund management and equity research.

- Number of schemes to fund manager ratio: Many mutual fund houses frequently launched too many similar products, so that they could gather more Assets Under Management (AUM). Eventually, this leads to the fund manager being over-burdened in managing these multiple mutual funds, which can result in lower efficiency of the fund manager by focusing on the need of his/her investors.

- Proportion of AUM performance: Some fund houses constantly engage in an exercise of increasing their AUMs, through frequent product launches. Well, that may be good in a way, but does not necessarily reveal that a fund house with a larger AUM, is good for you as an investor. Fund houses where a significant proportion of their AUM is performing better should be rated higher.

- Unique schemes: Frequent product launches, with an aim to increase AUM, in our opinion just do not make much sense. The fund launched has to be unique, otherwise, it is simply a “old wine in a new bottle”.

- Investment Systems and Processes: The mutual fund house’s ideology is reflected through this factor. The fund’s instrument (stock / debt papers) picking is also a function of the investment systems and processes followed, which eventually links to the fortune of the fund.

PersonalFN follows a stringent scoring model,which ensures that the scheme is tested on various quantitative as well as qualitative parameters, and is accordingly compared and scored vis-à-vis its peers. The schemes able to pass through our rigorous test and achieve the maximum composite score on all parameters (based on pre-specified weightages) will get higher star rating.

Recently,

the market regulator took cognizance of the fact that fund ratings vary across rating agencies. The Securities and Exchange Board of India (SEBI) has decided to make them more accountable by asking them to register under SEBI (Research Analysts) Regulations, 2014. But, the registration as a research analyst is not necessary for the platforms offering ranking services in the public domain. However, they may still need to give out a set of disclosures.

Star ratings can be indicatively used while selecting winning mutual fund schemes; but, they can no way be the conclusive aspect. Instead, doing a need-based analysis is necessary wherein you take into account your risk appetite, investment objective, investment horizon and financial goals, before you zero down on mutual fund schemes.

Anil just realised that in life, there are no shortcuts. He needs to make that extra effort to pick the right scheme and generate long-term wealth.

However, there is another option. He can

take the help of an investment adviser or opt for PersonalFN’s unbiased mutual fund services backed by a stringent mutual fund ranking methodology.

Like Anil, if you want to generate long-term wealth, you may try various

unbiased mutual fund research services offered by PersonalFN.

Recently, we’ve released an

Ultimate Strategic Portfolio for 2025 of diversified equity mutual fund schemes that offer a high-reward potential. We strongly recommend you opt for this service if you have an investment time horizon of 7-8 years and have a high risk appetite.

Add Comments