Citing the upside risks of inflation, the RBI has kept policy rates unchanged at its third bi-monthly monetary policy review. However, it has reiterated that its policy stance remains accommodative. The Central Bank also continues to be committed to addressing the liquidity related concerns of the system.

Food inflation poses a threat…

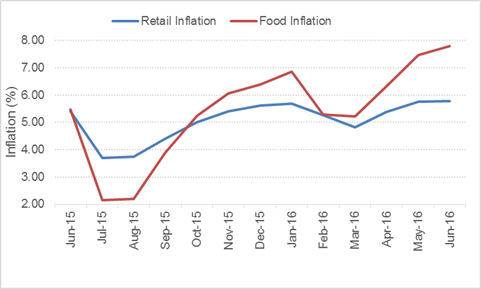

Data as on August 02, 2016

(Source: BSE, PersonalFN Research)

Background to the third bi-monthly monetary policy

In Q2 of the Calendar Year (CY) 2016, growth in the advanced economies were plagued with... and the outlook remained hazy. In the U.S., inventories have depleted, considered a negative, however, substantial job market data partially negated the effects of it. Uncertainty increased in Europe with Brexit and the European banking system witnessed some stress, adding to the woes of the European policy makers. On the other hand, Japan remained under pressured due to a stronger Yen. Industrial production had cooled and a considerable rise in the deflationary risks were the biggest challenges and called for the announcement of the monetary and fiscal stimulus.

For emerging markets, Q2 was a mixed bag. China managed to report stable growth thanks to high stimulus measures initiated by the authorities. Despite a smaller rise in the orders, adverse weather conditions, and lacklustre exports curtailed the manufacturing activity. Although the threat of recession has receded considerably in Brazil and Russia, policy uncertainties and benign commodity prices continue to pose a challenge.

Activities in global trade slowed in the first half of CY 2016. In the recent times, equities and currencies with an exception of the Pound Sterling have managed to stabilise, indicating that the market has absorbed the news of Brexit. That being said, negative bond yields on Government bonds of many countries, weakness in crude oil prices, and the high demand for gold indicate that risk aversion still persists.

Back home conditions improved. After receiving deficient monsoon for two consecutive years, the country has so far received extremely satisfactory rainfall. Until the first week of August, India received the cumulative rainfall of 103% of long-period averages. Around 80% of the country received normal to excess rainfall. After a rickety start, Kharif sowing gathered momentum, especially in pulses. Considering overall developments, it seems the Kharif production targets set by the Agricultural Ministry are achievable.

There have been some early signs of revival in manufacturing activities. Consumer demand and industrial output picked up indicating some resurgence. Business confidence remained high, and marketing budgets of corporates witnessed incremental allocations.

However, retail inflation remains elevated in recent times and, measured by the movement of Consumer Price Index, reached a 22-month high in June. Even after considering the seasonality and the impact of low base effect, inflation was driven mainly by higher food prices. On the positive side, services inflation softened a bit. After falling for 18 months, exports surged by 1.27% in June. Major constituents of the export basket showed the turnaround. On the other hand, non-oil-non-gold imports declined.

On this backdrop, the RBI retained its GDP estimates at 7.6% for FY 2016-17.

Liquidity Conditions...

Higher Government expenditure helped counterbalance the unusually high currency demand in June and July. In June, the average daily injection by RBI amounted to Rs 37,000 crore. However, in July and August, the operations shifted from the injection of liquidity to the absorption of the surplus. On an average, it sucked in Rs 14,100 crore every day in July and Rs 40,500 crore in August (upto August 8, 2016). Taking a step towards achieving a neutral liquidity position, in the long run, the RBI has injected Rs 80,500 crore so far. It has estimated that it will take about a year or two to get the system in a liquidity neutral position. Those who find it a bit tough to comprehend the liquidity part, here's the explanation.

The RBI manages cash requirement in the system at two levels—temporary liquidity requirements and durable liquidity needs. To address short-term demand-supply mismatches, it injects money into the system as and when required through various instruments. You may consider these as temporary adjustments. However, as far as the durable liquidity goes, traditionally, the RBI has been leaving the system cash-starved in the long run. However, under Dr Rajan, it decided to end this practice. Now, the aim of the RBI is to bring the system in a neutral position—cash-starved situation makes it difficult for the productive sectors of the economy to borrow while excess liquidity situation may be inflationary.

Under the governorship of Dr Rajan, it has often taken a hawkish stance on the policy rates. By deciding to bring the permanent liquidity position to a neutral level, the RBI has passed on a clear message. The economy won't be starved for credit requirements, however, unless the overall circumstances become favourable, rates won't be lowered.

Monetary policy at glance:

- RBI kept the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.5%

- The cash reserve ratio (CRR) of scheduled banks also remained unchanged at 4% of net demand and time liabilities (NDTL)

- The Central Bank continue to provide liquidity as required, but its aim remained to progressively lower the average estimated liquidity deficit in the system from one per cent of NDTL to a position closer to neutrality.

- Consequently, it left the reverse repo rate under the LAF unchanged at 6%, and the marginal standing facility (MSF) rate and the Bank Rate at 7%.

Policy rationale:

- So far in FY 2016-17, inflation has risen at a faster-than-estimated pace. Although RBI remains optimistic about achieving the inflation target of 5% by March 2017, it has flagged some significant risks as well.

- The expectation of non-food-non-fuel inflation remains high. Moreover, in the fuel category too, if the decline in the crude oil prices proves to be temporary and contrary to the expectations if food prices remain elevated, the inflationary pressure will mount further, exacerbating the situation.

- The implementation of the 7th Pay Commission is going to have an inflationary impact on house rents due to an increment in allowances. RBI believes, although it can be considerate to the one-time impact on the house rents, it will have to ensure that it doesn't translate this into the generalised inflation.

Outlook:

For the stance of the RBI to remain accommodative, the positive impact of above-average monsoon has to translate into lower food prices and the trend of disinflation in services must continue in the future. Among other factors, RBI will closely monitor the impact of 7th Pay Commission on the inflation.

Impact on capital markets:

Since all RBI announcements were in line with the expectations, equity and debt markets didn't react negatively. Rather, bond yields have fallen sharply over the last few weeks. The Government has committed to curtailing the inflation at 4% with a 2% margin for error on the upside as well as on the downside for next 5 years. Currency stability, tight fiscal management, and negative yields in many advanced economies have made Indian bonds attractive to global investors.

Equity markets have seen some profit booking over the last few days. However, more than the monetary policy announcements, other factors have been responsible for the decline in equity indices. Given the quality of corporate earnings in Q1, FY 2016-17; valuations looked overstretched for many stocks. As a result, the momentum that was positive so far seems to have reversed, tasting the disappointment.

Beyond monetary policy:

This being his last monetary policy review in the present term, Dr Rajan touched upon a whole host of issues while speaking to media.

Banks are on the right track to resolving NPAs...

On the on-going conundrum of Non-Performing Assets (NPAs) of the banking system, Dr Rajan opined that the RBI has successfully embedded the culture of cleanup of loans the process of recovery. The response to various windows and the approach of bankers and borrowers to look upon them has improved in the recent past. The mindset of the system has changed from delaying the process of recognition of bad loans to solving the problem of bad loans. It has also made an observation, the pace of generation of new NPAs has slowed considerably in last two quarters. Although the high provisioning may continue for a few more quarters, as the economy resumes its high-grow path, the situation would improve further. On the whole it believes, banks have adequate tools to resolve the problem of NPAs decisively, and it sees most of them moving in the right direction.

Indian currency appears a lot more stable...

India's currency was in doldrums when Dr Rajan took the charge in September 2013. To shore up the Indian Rupee , RBI allowed banks to accept FCNR (Foreign Currency Non-Resident) deposits. Billions of US$ flew in India as the terms of the scheme were attractive. In 2016, these deposits will mature. There were concerns about the possible outflow of US$ on account of repayment. Quelling the concerns, the RBI exuded confidence in handling the situation deftly. Dr Rajan briefed the media that, it has already hedged 80% of its positions in the forward market. Indian has adequate reserves of US$ 365 billion to set off the outflows of about US$ 26 billion.

GST is revolutionary...

RBI also acknowledged that the passage of GST is a positive for the economy. The possibility of GST lifting the GDP growth by 2% can't be ruled out consider the benefits it brings in, which include unified market conditions, improvement in efficiencies, and reduced transportation costs among others. When asked about the impact of GST on the inflation, RBI Governor expressed that it's prudent to assume that GST will increase inflation, but whether it will be a short-term disruption or a long-term phenomenon that needs to be monitored. The RBI also added that 52% of the Consumer Price Index (CPI) won't be affected by the implementation of GST.

A word about Dr Rajan's tenure:

Proponents and opponents of Dr Rajan's policy actions and his hawkish stance on inflation speak with equal vigour. Although he has always denied having any rift with the Government, this has become evident on many occasions. All said and done, the Government notified that the inflation target of 4% for next 5 years should be treated as its admission that, Dr Rajan's policies were congruent with the developmental and reformist agenda of the Government. He introduced some institutional changes to the monetary framework of India that will go a long way to providing stability and help prepare for the global adversities.

Approach investors need to adopt:

PersonalFN believes, investors would be better off if they avoid speculating on any event. Instead of basing your investment decisions on significant macroeconomic developments, you should focus on your financial goals. An asset allocation plan that takes into account your financial goals and risk appetite should guide all your investing decisions. PersonalFN offers unbiased mutual fund research services and unlike many other mutual fund advisors, its advice is backed by solid research and diligent monitoring.

Add Comments