Rohit met Rahul, his child-hood friend for lunch yesterday. Rahul is a well-known Architect in town and Rohit works for an Investment Bank. After hours of tête-à-tête on varied subjects, what kept them going was discussion about their retired life. They envisioned owning neighbouring bungalows at Andaman and leading a peaceful and serene life by the coast.

Rohit met Rahul, his child-hood friend for lunch yesterday. Rahul is a well-known Architect in town and Rohit works for an Investment Bank. After hours of tête-à-tête on varied subjects, what kept them going was discussion about their retired life. They envisioned owning neighbouring bungalows at Andaman and leading a peaceful and serene life by the coast.

But there were some obvious questions:

“Will the retirement fund last till my last breath?”

“Is living a blissful life during golden years, really be possible?”

Rohit, being an investment banker, was smarter. He was saving adequately and investing; though was not sure if that would be enough for his retirement. He held life is unpredictable and always fearful about his future.

Have such questions bothering you too? Yes, read on…

Worrying about post retirement life is common.

But to fulfil this vital life goal, engaging in prudent retirement planning is essential!

You also ought to save enough for the rainy days. God forbid, but if a contingent event strikes on––example: loss in business; medical emergencies; or you are detected with life threatening disease–––your hard-earned money kept as contingency reserve will come to your rescue.

Noel Whittaker rightly says, “Life is full of uncertainties. Future investment earnings and interest and inflation rates are not known to anybody. However, I can guarantee you one thing... those who put an investment program in place will have a lot more money when they come to retire than those who never get around to it.”

So, ensure you have contingency fund in your retirement plan. It is also advisable to maintain 6 to 12 months of your expenses to compensate for unforeseen events. This will ensure that your retirement savings do not get eroded.

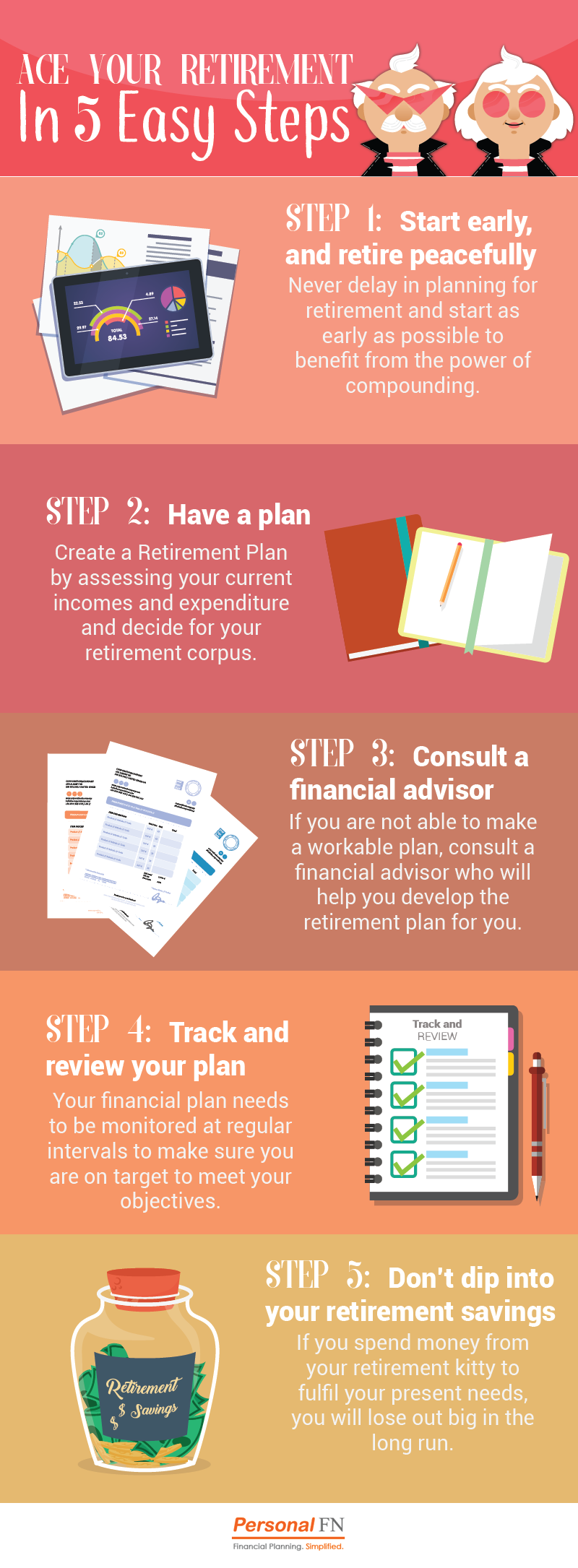

Steps to blissful retirement

Retirement Planning can give you the opportunity to spend the golden years of life the way you want and with the same lifestyle that you enjoy today.

However, you must recognise that engaging in prudent retirement planning is the key to remain financially secured and maintain a comfortable standard of living even in the later years of your life, where you may not draw regular flow of income.

You see, planning for retirement can keep you financially independent even during your golden years, taking care of day-to-day expenses as well as any medical emergencies that may arise as your age progresses.

“Planning is bringing the future into the present so that you can do something about it now”, says Alan Lakein,

Hence, create a retirement plan by following some simple steps…

Step #1: Determine the Retirement Corpus

Unless you know where you are headed, it is very difficult to get there.

In retirement planning as well, it is important to have a target in mind which you wish to achieve in order to live life comfortably in the second innings of your life.

To arrive at some corpus amount, you might need to make certain estimations and assumptions. You have to first work out at what age do you wish to retire, what is your life expectancy (based on family history and health conditions), how much you spend every month, inflation that you expect on these expenses, pre and post retirement rate of return that you expect on investments, among a host of other factors.

Thereafter you can compute the corpus required for your retirement. You could take the help of PersonalFN’s online retirement calculator to arrive at this target figure.

In case of Rohit, his current age is 45. He earns Rs 1,50,000 p.m. and also earns around Rs 1,00,000 every year as incremental bonus. Mr Rohit wishes to retire at age 55.

The details of expenditures and goals are as under:

- Current household expenditure is Rs 50,000 per month.

- He spends Rs 1,25,000 per annum on an annual vacation with his family (excluding the above)

- Medical expenses are around Rs 25,000 a year

- He first wishes to maintain the same standard of living post-retirement.

- His life expectancy is assumed to be 85 years

Rohit is adequately insured and has created a contingency corpus of 12 months of living expenses and is maintaining this corpus in liquid funds and partly as cash in the bank.

As he is nearing retirement, Rohit is worried about how much corpus he would need to live a comfortable retired life and whether or not he will be able to build this corpus in his remaining 10 working years.

Case Facts and Estimated Retirement Corpus

| Rohit’s age |

45 years |

| Age at Retirement |

55 years |

| Life Expectancy |

85 years |

| Present Household expenditure (per month) |

Rs 50,000 |

| Amount spent on an annual vacation |

Rs 1,25,000 |

| Annual Expenditure on healthcare |

Rs 25,000 |

| Inflation rate for household expenses |

7% |

| Inflation rate for vacation and medical |

10% |

| Pre-Retirement Return |

15% |

| Post-Retirement Return |

6% |

| Corpus Required at Retirement |

Rs 5,46,36,468 |

(The table is for illustration purpose only)

As per calculation, Rohit will require a retirement corpus of Rs 5.4 crore to maintain his current standard of living during golden years.

He needs to make efficient use of assets, invest in productive asset classes and investment avenues therein, whereby he can counter inflation and build the above retirement corpus. But to own a bungalow in Andaman––as he wishes to––much more effort and resources need to be allocated. Plus, liabilities need to be reduced or rather repaid, so as to not have any debt obligations and live a blissful retired life.

Step #2: Start Early, and Retire Peacefully

An often-heard excuse for putting off retirement planning is “I have enough time to go before I retire, so why rush?”

Unfortunately, many individuals fail to realise that procrastination is their biggest enemy when it comes to making retirement plans. In fact, starting early and ensuring that you have sufficient time on your side is the key to successful retirement planning.

It is imperative for you to understand that being young provides you a benefit that is not available to all, 'time'.

Moreover, as you grow older, your risk taking capability decreases. Besides, starting late is disadvantageous since it gives you lesser time to grow your retirement kitty. There is even a possibility that you may fall well short of your target. We will illustrate this with the help of an example:

Mr X needed Rs 25 lakhs at the time of retirement to buy a house. He can either start saving for it now or postpone it for future. The expected return on investment is assumed 12% p.a. And here, in the table below, 3 scenarios are presented, each showing time left before Mr X retires:

|

Case I |

Case II |

Case III |

| Retirement corpus required (Rs) |

25,00,000 |

25,00,000 |

25,00,000 |

| No. of years left before retirement |

30 |

20 |

10 |

| Expected returns on investments (%) |

12 |

12 |

12 |

| Annual investment needed to fulfil the goal (Rs.) |

9,249 |

30,979 |

1,27,197 |

| Monthly investment needed to fulfil the goal (Rs) |

708 |

2,502 |

10,760 |

(The table is for illustration purpose only)

In Case I, the monthly investment amounts to approximately Rs 708 to achieve Mr X’s target amount; however, with passage of time, it grows exponentially.

As a result, if he starts investing for retirement as in case II, 20 years before the due date, Rs 2,502 will be the monthly investment amount.

Finally, in case III, when he is just 10 years away from his retirement, the monthly investment required will be Rs. 10,760.

So, lesser the time at your disposal, the higher the amount has to be set aside for meeting your retirement goal. Not only can this be hard on the wallet, but may not be a feasible option for some. As a result, the retirement corpus might have to be toned down or endure a lower retirement corpus.

Moral of the story: Not only does it pay to start early, delaying the same can cost you dearer.

Step #3: Follow your Asset Allocation

Exposure to different asset classes is imperative in building your retirement portfolio. You can’t afford to put all your eggs in basket; there is risk involved.

Different asset classes i.e. equity, debt, gold have different attributes which help in maintaining the required balance in one’s retirement portfolio. By following your asset allocation, we refer to investing into each asset class, based upon your risk profile and the number of years left before the goal befalls.

For example, if your retirement is more than 10 years away, then depending on your risk profile, your retirement funds can be allocated predominantly in equity, and 15% to 10% exposure to debt and gold respectively.

If your retirement is more than 5 to 7 years away, you can have 45% to 60% exposure to equity, with upto 10% in gold and the rest in debt.

However, if you are retiring in less than 3 years, it is advisable to redeem from equity investments and shift towards debt / fixed income instruments that are not impacted by market volatility.

You must remember that merely following a suitable asset allocation alone will not help you reach your goals unless you invest in sound and appropriate investment venues.

Step #4: Choose suitable Health Insurance Policy

Insurance is a must in retirement planning.

As one grows old the number of physical ailments that one might suffer from also increases. While you might believe that something will not ‘happen to you’ – that is often exactly what your neighbour is thinking.

Hence it is extremely important for you to have a suitable and adequate health insurance cover ––commonly known as mediclaim.

Apart from this, it is also wise to opt for a personal accident and critical illness policy from an early age.

Plus, you can maintain a separate contingency fund worth Rs 5–10 lakh for medical emergencies.

Step #5: Track and review your plan

Once retirement plan is drawn prudently and is executed, it needs to be tracked and monitored at regular intervals (at least once a year) to make sure you are on target to meet your objectives.

Any changes in the income, expenses, retirement age etc. needs to be incorporated in the plan. Also, make sure the retirement plan is agile to the fundamental changes in market scenario.

End note…

Hence, to make sure that you have enough money for your retirement or golden years of life, start early and plan your retirement today! Do not wait for long thinking you have enough time. Remember, the early bird gets a bigger worm.

If you wish to learn more about retirement planning , we recommend you to subscribe to PersonalFN’s The Retirement Letter.

In The Retirement Letter, we will chalk out an entire retirement strategy for you! We will tell you how to...

- Zero in on the exact amount you will need every month after retirement

- Manage your cash flows - all your expenses and your savings

- Save your taxes and invest that money on other money making options

- …and much more!

But if you need handholding in your retirement planning , reach out to our experienced investment consultant, for an independent and unbiased advice. You will experience a holistic approach to plan for your retirement. This service includes:

- Quantification of your Retirement goal

- Your personal Risk Profile Analysis

- Analysis of your overall financial situation including investments, insurance, incomes, expenses, assets and liabilities

- Charting an ideal Asset Allocation for you

- Developing a detailed financial plan including cash flows and making recommendations of investment instruments to achieve your Retirement goal

- Reviewing your overall existing portfolio and recommending changes as needed

For more information on PersonalFN’s Retirement Planning Service, contact us at (022) 61361200 or write to us at info@personalfn.com. We will be happy to help you!

Ensure that you don't delay your retirement planning a moment longer! Remember, the sooner you start, the more corpus you will be able to build!

Happy Retirement Planning; and

Happy Investing!

Add Comments