(Image source: Photo created by rawpixel.com - freepik.com)

(Image source: Photo created by rawpixel.com - freepik.com)

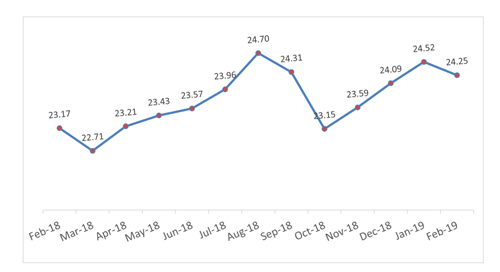

Assets managed by the mutual fund industry have grown from Rs. 23.17 trillion in February 2018 to Rs. 24.25 trillion in February 2019. This represents a 4.66% growth in assets over a year.

Graph: AUM of the Indian Mutual Fund Industry (Rs in Trillion)

Data as on February 2019

(Source: www.amfiindia.com)

So, can you depend on Debt fund investments to provide higher returns than bank FDs?

Yes, but at an elevated risk.

[Read: Is Your Investment In Debt Mutual Fund At Risk?]

In fact, the senior citizens are choosing debt mutual funds because they have managed to provide better returns than vanilla FD and other government schemes without considering the risk involved.

Current bank FD rates for a year are in the range of 5.75% to 6.85%, and for senior citizens, the investment rates banks are offering are 6.25% to 7.35%. Even the government schemes for retirement schemes like the NPS, SCSS, PPF, and KVP provide 8%, 8. 7%, 8%, and 7.7%, respectively.

Table: Performance of Top Short duration and Ultra short duration Funds

Data as on March 26, 2019

(Data Source: ACE MF)

Please note, this table only represents the best performing Debt Funds based solely on past returns and is NOT a recommendation.

Mutual Fund investments are subject to market risks. Read all scheme related documents carefully.

Past performance is not an indicator for future returns. The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

Over a span of one-year time frame, in the Ultra short duration category, Franklin India Ultra-Short Bond Fund, Reliance Ultra Short Duration Fund, and DHFL Pramerica Ultra Short Term Fund have been the top three performers on the list of funds that have done well in the past.

But for a period of five years, ICICI Prudential Ultra Short Term Fund, Franklin India Ultra-Short Bond Fund, and Invesco India Ultra Short Term Fund have generated a better CAGR

And in the Short duration category of funds, Franklin India ST Income Plan and Indiabulls Short Term Fund have performed well in one year and maintained consistency for five years from the list of well-performed schemes in the past.

It is noteworthy that the past performance is not indicative that the scheme will always outperform. Case in point, Reliance Ultra Short Duration Fund did not perform well for over a period of three and five years.

These top performers have managed to outperform the benchmark indices. But that does not mean they will always outperform. And even if they do, there is high risk involved, because to beat the benchmark indices the portfolio of these schemes includes papers which are below "AA - ratings" or are unrated.

Based on the issuer/corporate's financial stability, earnings record, creditworthiness, etc., is a debt paper rated by credit research agencies. AAA is the highest quality and often meant to be the safest. But due to their failure to fulfil the debt obligations, several corporates have been downgraded. So, one should not ignore the risk associated with debt instruments.

Recent downgrading of IL&FS and DHFL due to default in payments is a live example and major fund houses were holding debt papers from these corporates. And as an investor, having a portfolio with exposure to such schemes can prove detrimental.

According to Moneylife, mutual fund houses have more than Rs 16,000 crore exposure to IL&FS, DHFL, and Essel Group companies. You would be surprised to know that some funds with shorter maturities have invested a substantial part of their portfolio in DHFL papers.

As per the portfolio disclosed on 31 January, 2019, DHFL Pramerica Ultra Short Term Fund has invested 35% of its assets in DHFL papers while the exposure of JM Short Term Fund, JM Low Duration Fund, and BOI AXA Ultra Short Term Fund have been 22%, 22%, and 14%, respectively.

Especially senior citizens should stay away from this because they may lose out on their capital. For a senior citizen, the major concern is the preservation of capital with a steady inflow of income. Even though debt fund investments are considered to be safer than equity fund investments, they are definitely not risk-free. It would be a grave mistake to consider it safe to invest in short-term debt funds.

On the contrary, bank FDs as an asset class is a safer investment instrument over a period of one year. Ultra-short and Short-duration bond funds are debt funds that invest in instruments with shorter maturities, ranging from 1-3 years.

[Read: Factors To Look At While Investing In Bank FDs]

Short-term debt funds aren't a defence strategy against default risk if the fund manager isn't recognising the risk, acknowledging it, and taking prudent steps to protect investors' interests.

So, remember:

-

Investing in debt funds isn't risk-free.

-

Do not invest in schemes only because they have outperformed their benchmarks in the recent past.

-

Consider your financial goals, risk appetite, and time horizon before investing in any debt-oriented scheme.

-

Following your personalised asset allocation is the key.

-

Ideally, you should invest only in schemes that have a maturity profile resembling with your time horizon, to avoid unpleasant surprises.

-

Invest only in debt schemes offered by mutual fund houses that follow robust investment processes and have adequate risk management systems in place.

PS: If you are planning for your blissful retirement, don't miss out on PersonalFN's Retire Rich service. This is a new and exclusive service with the sole intent of securing your retirement.

You will even gain the benefit of investing in Top 5 funds along with a DIY (Do It Yourself) retirement solution, where you can start planning for your retirement and potentially build a substantial corpus that could sustain you in the golden years of your life.

Add Comments

| Comments |

yefuchen.yc@gmail.com

Mar 29, 2019

i believe there is a correction to be made here... "Recent downgrading of IL&FS and DHFL due to default in payments"

DHFL has never defaulted on any payment till date.. this is incorrect information.. kindly rectify this..

|

1