|

| August 12, 2016 |

|

|

|

|

Impact

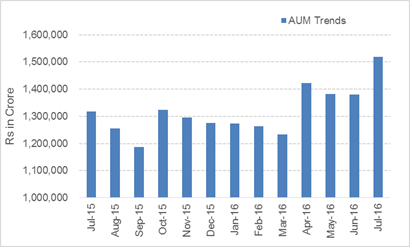

If good rainfall has brought smiles back on the faces of farmers this year, constant inflows of fresh investments have given mutual fund houses a reason to cheer. Between July 2015 and July 2016, AUM (Assets Under Management) of the mutual fund industry has grown at a healthy pace of 15.2%. The asset base of debt funds has expanded from Rs 5.56 lakh crores in July 2015 to Rs 6.70 lakh crores in July 2016 which was a 20.5% rise. While equity AUM grew by 14.5% from Rs 3.94 lakh crore to Rs 4.51 lakh crore between July 2015 and July 2016.

Mutual fund AUM at an all-time high…

(Source: AMFI, PersonalFN Research)

As a result, the AUM of mutual fund houses in India surpassed the Rs 15 lakh crore mark for the first time ever. In July 2016 alone the industry received the net inflows of Rs 1.02 lakh crore.

Factors that contributed to the AUM growth are…

- Banks have been slashing interest rates on deposits. As a result, the household savings are flowing into debt funds.

- Tight fiscal management by the Government and range-bound inflation instilled confidence among investors of debt funds. The stable Rupee value helped too.

- On the other hand, sustained rally in the equity on the back of regular inflows of foreign capital boosted the investor's sentiment.

- Expectations of robust corporate earnings triggered off rallies in equities. Small and midcap funds have benefited immensely from this trend.

It is noteworthy that, unlike in the past, investors putting money in equity funds have followed a disciplined approach. Despite the rising markets, net inflows in equity schemes haven't jumped acutely. It seems investors have opted for Systematic Investment Plans (SIP) offered by mutual funds. Although mid and small cap funds have seen a greater buying interest, there too, money seems to be flowing through the SIP route. Against that, inflows and outflows in income funds have been abrupt and sporadic. This goes to show that, investors have been betting on macroeconomic developments and speculating on the direction of interest rates.

PersonalFN is of the view that you should consider your time horizon before investing in a debt fund, and invest no more than 20% of your fixed income portfolio in long-term debt funds. When it comes to investing in equity schemes, avoid getting carried away by the market momentum. Although the mid and small cap funds have rallied hugely in the last few months, any disappointment in the corporate earnings may nip the ongoing rally.

Rather than concentrating on the market conditions, you should focus on your financial goals and risk appetite before investing your hard earned money.

|

Impact

Although the Government remains optimistic that the implementation of GST will end the "tax terrorism" it is likely to terrify those who consume services heavily. The phrase "Tax Terrorism" was coined to describe that the litigious approach of Indian taxmen that intimidated even the honest taxpayer. India's indirect tax structure has always been complicated. Disputes between the authorities and the taxpayers are common under the current regime due to many factors that primarily include various taxes, different rates, and different tax treatment to similar goods in different states. GST is "one tax" that replaces all others indirect taxes. So no State can provide "additional" incentive to a specific sector using its powers to make its independent tax laws and, consequently, discouraging a particular business, adopting restrictive tax policies won't be possible either. Moreover, implementation of the GST will be supported by the robust I.T. infrastructure. All these factors are likely to minimise the causes of friction between the tax authorities and taxpayers.

However, the flip side is, taxes that are charged at a flat rate at present, such as service tax, are likely to go up once the GST is implemented. Although the Government hasn't taken any decision on the rate of GST, it will be probably in the range of 18% to 20%. As a result, services that are currently taxed at 15% are likely to become expensive.

So those who use their cell phones continuously will have to shell out more on the bills, and similar will be the case with those who regularly dine out.

Investors will suffer once the GST is implemented

If you think only spenders will pay more for services, you are probably misinformed. Once the GST is implemented, you will shell out more even to invest in mutual funds. India is likely to implement the Goods and Services Tax (GST) Act at the start of the Financial Year (FY) 2017-18. So don't be surprised if mutual funds subsequently raise the expense ratios under most of their schemes.

Why is Service tax relevant to mutual funds?

Mutual funds not only provide fund management services, but in this effort, they also utilise services of some other entities such as custodians and brokerage houses. As a result, the expense ratio of the scheme you are invested in also includes the Service tax the Asset Management Companies (AMCs) pay. Any increase in the Service tax rate may force mutual funds to hike their expense ratio. Although a few mutual funds may prefer to absorb the effect, most others are likely to pass on the hike in costs because of the higher tax rate.

Don't bother too much about the expense ratio…

PersonalFN is of the view that, although the expense ratio is an important consideration while selecting a fund for your portfolio, a smart investor would focus more on the fundamental attributes of the scheme. You can never compromise on the quality of the schemes simply because they are cheap. If the fund houses can justify the higher expense ratio by generating superior returns and providing prompt services, investors won't necessarily mind the hike, which may be nominal in nature.

PersonalFN is of the view that, those who want to minimise costs may invest in direct plans offered by the mutual funds. Direct plans help you earn better returns. You may opt for the mutual fund research services offered by PersonalFN if you are unsure about the schemes to invest in. Unless you know which funds to buy, going for the direct plan would be a risky strategy.

|

Impact

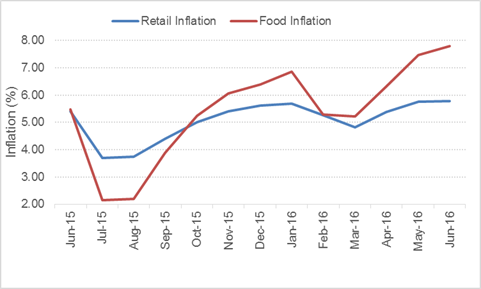

Citing the upside risks of inflation, the RBI has kept policy rates unchanged at its third bi-monthly monetary policy review. However, it has reiterated that its policy stance remains accommodative. The Central Bank also continues to be committed to addressing the liquidity related concerns of the system.

Food inflation poses a threat…

Data as on August 02, 2016

(Source: BSE, PersonalFN Research)

Background to the third bi-monthly monetary policy In Q2 of the Calendar Year (CY) 2016, growth in the advanced economies were plagued with... and the outlook remained hazy. In the U.S., inventories have depleted, considered a negative, however, substantial job market data partially negated the effects of it. Uncertainty increased in Europe with Brexit and the European banking system witnessed some stress, adding to the woes of the European policy makers. On the other hand, Japan remained under pressured due to a stronger Yen. Industrial production had cooled and a considerable rise in the deflationary risks were the biggest challenges and called for the announcement of the monetary and fiscal stimulus.

Background to the third bi-monthly monetary policy

In Q2 of the Calendar Year (CY) 2016, growth in the advanced economies were plagued with... and the outlook remained hazy. In the U.S., inventories have depleted, considered a negative, however, substantial job market data partially negated the effects of it. Uncertainty increased in Europe with Brexit and the European banking system witnessed some stress, adding to the woes of the European policy makers. On the other hand, Japan remained under pressured due to a stronger Yen. Industrial production had cooled and a considerable rise in the deflationary risks were the biggest challenges and called for the announcement of the monetary and fiscal stimulus. For emerging markets, Q2 was a mixed bag. China managed to report stable growth thanks to high stimulus measures initiated by the authorities. Despite a smaller rise in the orders, adverse weather conditions, and lacklustre exports curtailed the manufacturing activity. Although the threat of recession has receded considerably in Brazil and Russia, policy uncertainties and benign commodity prices continue to pose a challenge.

To ready more about this story and Personal FN's views over it, please click here.

|

Impact

In the recent past, a few Non-Banking Financial Corporations (NBFCs) raised money through the issuance of Non-Convertible Debentures (NCDs). Those enjoying good credit ratings witnessed an overwhelming response to their issuances. However, falling interest rates on bank Fixed Deposits and shallowness of the Indian bond market leaves individual investors in the fixed income category with fewer choices. As a result, primary issuances of companies enjoying high credit ratings get a tremendous response. But the problem is, over subscription often leaves many investors high and dry. Moreover, no matter how good a company is, you can't invest in it for a longer time duration as the distant future is always uncertain.

If somebody asks you to invest in an "AAA" rated company for 5 years, you will be comfortable with the offering, if the interest rate is higher than that offered on the bank FDs. However, if someone asks you to bet on the company for 15-20 years, you will probably feel apprehensive, as you don't know what will change for the company in years to come.

The RBI has taken an important decision to end this quality crisis and offer investors a variety of choices. It's decided to open up the secondary market of Government Securities (G-sec) for individual investors. As of now, the market is dominated by the institutional investors such as banks, mutual funds, and insurance companies among others. The ones who have demat accounts can buy and sell G-secs in the secondary market.

To ready more about this story and Personal FN's views over it, please click here. |

|

In the wake of mutual fund houses investing in fixed income securities of companies with a poor credit quality, the Securities and Exchange Board of India (SEBI) had introduced prudential exposure norms. As a part of that, it had imposed a sector cap on investments made by the mutual fund houses. However, now SEBI has loosened these rules a bit allowing debt schemes to invest additional 10% in housing finance companies. Currently, mutual fund houses are allowed to invest upto 25% of their portfolio in fixed income instruments issued by housing finance companies with a provision for making additional 5% investments. With the recently introduced changes, they can now invest upto 35% in housing finance companies.

Justifying the move, SEBI said, "In light of the role of HFCs especially in affordable housing space, it has now been decided to increase additional exposure limits provided for HFCs in financial services sector from 5 per cent to 10 per cent."

PersonalFN believes, although SEBI has enhanced the exposure limit for mutual fund houses investing in the housing finance companies, they will have to be watchful to the balance sheets of such companies. Investors should be wary of debt schemes compromising on the credit quality to earn higher returns.

In DebtSelect, PersonalFN recommends debt schemes that score high on risk management parameters and perform consistently across interest rate cycles.

|

Yield To Maturity (YTM): Yield to maturity (YTM) is the total return anticipated on a bond if the bond is held until the end of its lifetime. Yield to maturity is considered a long-term bond yield, but is expressed as an annual rate. In other words, it is the internal rate of return of an investment in a bond if the investor holds the bond until maturity and if all payments are made as scheduled.

(Source: Investopedia)

|

Quote : "In the world of money and investing, you must learn to control your emotions"- Robert Kiyosaki

|

|

|

|

© Quantum Information Services Pvt. Ltd. All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 101 Raheja Chambers, 213, Free Press Journal Marg, Nariman Point, Mumbai 400021. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667

|