(Image source: freepik.com)

(Image source: freepik.com)

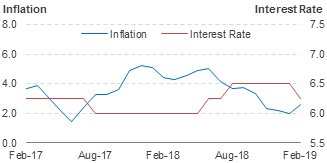

It appeared that weak consumer spending and rural distress were weighing on the inflation data, as both rural and urban inflation readings were low.

Graph 1: CPI Inflation has mellowed down. But will it remain low for long?

Data as of February 2019

(Source: MOSPI, RBI, PersonalFN Research)

Amidst flagging economic growth (India's GDP tumbled to 6.6% in the December 2018 quarter), the government is now looking at the RBI to reduce policy rates in order to reinvigorate economic growth.

Will RBI reduce policy rates in its 1st Bi-monthly Monetary Policy Statement for 2019-20?

Well, the clamour for a rate cut is on a rise. A number of economist and brokerages expect the central bank to cut repo policy rates, even as 'core inflation'--which excludes food and fuel prices --appears sticky at 5.5%.

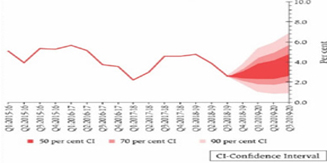

Graph 2: RBI's quarterly projection for CPI inflation (y-o-y)

(Source: RBI's 6th Bi-Monthly Monetary Policy Statement for 2018-19)

In its last, i.e. the 6th Bi-monthly Monetary Statement for 2018-19, the repo policy rate under the liquidity adjustment facility (LAF) was reduced by 25 bps from 6.5% to 6.25% with immediate effect. This was done in consonance with the objective of achieving the medium-term target for CPI inflation of 4.00% within a band of +/- 2 per cent while supporting growth.

The Monetary Policy Committee (MPC) also decided to change the monetary policy stance from 'calibrated tightening' to 'neutral'.

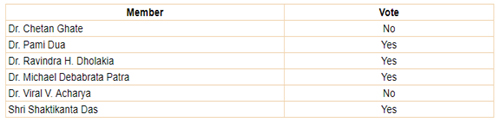

Table: How did the six-member MPC vote in the last policy meeting?

(Source: Minutes of the Monetary Policy Committee Meeting February 5-7, 2019)

Out of the six-member MPC, four members, including RBI Governor, Mr Shaktikanta Das, voted in favour of a policy rate cut, while only two members voted in favour of keeping policy rates unchanged. So, the majority were in favour of a policy rate cut.

The path to inflation and interest rates going forward...

The central bank has projected headline inflation to remain soft in the near term reflecting the current low level of inflation and the benign food inflation outlook.

Beyond the near-term, the RBI is of the view some uncertainty warrants careful monitoring. The central bank has observed:

-

First, vegetable prices have been volatile in the recent period; reversal in vegetable prices could impart upside risk to the food inflation trajectory.

-

Secondly, the oil price outlook continues to be hazy.

-

Thirdly, a further heightening of trade tensions and geopolitical uncertainties could also weigh on global growth prospects, dampening global demand and softening global commodity prices, especially oil prices.

-

Fourthly, the unusual spike in the prices of health and education needs to be closely watched.

-

Fifthly, financial markets remain volatile.

-

Sixthly, the monsoon outcome is assumed to be normal; any spatial or temporal variation in rainfall may alter the food inflation outlook.

-

And finally, several proposals in the union budget for 2019-20 are likely to boost aggregate demand by raising disposable incomes, but the full effect of some of the measures is likely to materialise over a period of time.

Many of RBI's projections have come true.

The Reserve Bank has revised the path of CPI inflation downwards to 2.8% in Q4:2018-19, 3.2-3.4% in H1:2019-20 and 3.9% in Q3:2019-20, with risks broadly balanced around the central trajectory.

The CPI inflation for March 2019 will be released only after RBI's 1st Bi-monthly Monetary Policy Statement for 2019-20.

In my view, the RBI under the new Governor, Mr Shaktikanta Das, may perhaps give in to pressures amidst the clamour for a rate cut. The repo policy rates could be lowered by another 25 basis points (bps) in the April policy - the 1st Bi-monthly Monetary Policy Statement for 2019-20 (scheduled on April 4, 2019) taking courage from low inflation reading, which is well within its comfort zone, to support growth. That said, the central bank would take cognisance of the fact the core inflation is sticky.

The investment strategy to follow while investing in debt mutual funds now...

Investing aggressively at the longer end of the yield curve could prove imprudent, although the RBI has taken an accommodative stance already and may honour with another rate cut of 25 bps. Investing in long-term debt funds (holding longer maturity debt papers) can be risky in the foreseeable future. If inflation moves, it will then limit RBI's scope of reducing policy rates further. Currently, shorter maturity papers are more attractive.

So, ideally you'll be better off if you deploy your hard-earned money in short-term debt funds; but ensure you're giving due importance to your investment time horizon, asset allocation, and diversification.

Consider investing in short-term debt funds for an investment horizon of up to 2 years.

If you, as an investor, have an investment horizon of 3 to 6 months, ultra-short duration funds would be the most suitable.

And if you, the investor, have an extreme short-term time horizon (of less than 3 months), you would be better off investing in overnight funds. And if you wish to take slightly more risk, consider a liquid fund. But avoid liquid funds that have a very high exposure to Commercial Papers (issued by private entities).

Don't forget that investing in debt funds is not risk-free.

Remember, a sensible and astute investment strategy paves the path to wealth creation and is always good for your long-term financial well-being.

Happy Investing!

This article first appeared on Certified Financial Guardian.

Add Comments