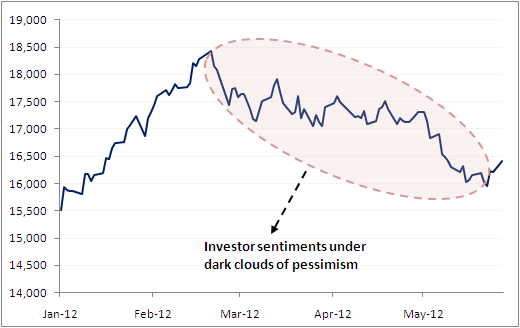

Emotions play a major role in determining the stock market activity. When the investor sentiments are upbeat and there is a wave of optimism amongst the investor community, the stock markets or equity markets move northwards. On the contrary when the nervous investment sentiments prevail and clouds of pessimism hover over the investor community, the equity markets mellow down resulting in drain down of investors’ wealth.

The rollercoaster ride of Indian equity markets

Data as on: May 28, 2012

(Source: ACE MF, PersonalFN Research)

Thus, citing this pessimism in the equity markets and bleaker prospects, the Portfolio Management Services (PMS) providers are now offering equity products with variable costs. In this structure, clients pay fund management fees only to the extent of gains, as against the traditional system where a fixed fee is charged irrespective of return which the fund delivers, in addition to a performance bonus too.

The variable fee structure (also known as the performance linked structure) in PMS ensures that clients do not end up paying when the scheme is reeling under losses. Brokers such as Karvy Stock, Sharekhan and Emkay Global among others, are at present offering such low-cost products to their rich clients, who are charged up to 20% on returns.

Impact on the investors...

While investors may be wooed by the lucrative offerings from the PMS providers during such testing times of the equity markets, investors need to act responsibly and carefully read the fine print in order make sure there are no unfavourable clauses. Care should be taken to check the maintenance fees charged by the PMS provider apart from the performance fees.

Our view:

In our opinion, the PMS providers have come with innovative ideas in a feeble equity market in order to boost the sale of their products. Once the market takes a turn and moves in the northward direction these same PMS providers would come with the traditional PMS products with fixed commissions irrespective of the fund returns or on hybrid models (where PMS providers levy a fixed fee as well as a performance linked fee).

Investors therefore, should make sure that their risk profile matches with that of the product being offered. Investing in equity markets is not a bad proposition but if one lacks the required aptitude to track the equity markets then it is wiser to adopt the indirect route to equity markets i.e., through mutual funds, which follow strict investment mandates (depending upon the type of scheme). However, while investing in mutual funds as well, one should adopt enough prudence and select winning mutual funds. And while you may get lured by performance track record exhibited by your mutual fund distributor / agent / relationship manager, remember there’s more to selecting winning mutual funds, than mere performance. Both quantitative and qualitative aspects should be assessed to have the right funds in your portfolio, which suit your investment objective.

Will the variable cost structure entice you to invest in PMS scheme? Let us know your comments or post them on our our Facebook page / Twitter page.

Disclaimer: This newsletter is for Private Circulation only and not for sale, is only for information purposes and Quantum Information Services Pvt Limited (PersonalFN) is not providing any professional/investment advice through it and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. PersonalFN disclaims warranty of any kind, whether express or implied, as to any matter/content contained in this newsletter, including without limitation the implied warranties of merchantability and fitness for a particular purpose. PersonalFN and its subsidiaries / affiliates / sponsors / trustee or their officers, employees, personnel, directors will not be responsible for any direct/indirect loss or liability incurred by the user as a consequence of his or any other person on his behalf taking any investment decisions based on the contents of this newsletter. Use of this newsletter is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. PersonalFN does not warrant completeness or accuracy of any information published in this newsletter. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This newsletter is for your personal use and you shall not resell, copy, or redistribute this newsletter, or use it for any commercial purpose. The user accepts the terms of use on this web site.

Add Comments

| Comments |

hemanlian@hotmail.com

Jun 17, 2012

Why would you take two credit cards, ineetrst rates less than the fixed-rate loan and it is a higher rate? Use the loan to pay off the highest ineetrst card. . . . . . pay the minimum on the lower two maps, and take the payment that you were doing on the 11% card and send it to the fixed interest rate. This should help ensure that this balance more quickly. If the fixed rate loan is paid, you take the payment and add it to the next higher interest card until paid off and then take those payments and send them to the lowest card. Sense? OR. . . You can do a balance transfer of all three cards to a 0% credit card and go from there. It would only make sense to transfer all three, if you can. |

biuro@icar.pl

Jun 17, 2012

This is getting a bit more subjective, but I much prefer the Zune Marketplace. The interface is colorful, has more flair, and some cool features like Mixview' that let you quickly see related albums, songs, or other users related to what you're listening to. Clicking on one of those will center on that item, and another set of neighbors will come into view, allowing you to navigate around exploring by similar artists, songs, or users. Speaking of users, the Zune Social is also great fun, letting you find others with shared tastes and becoming friends with them. You then can listen to a playlist created based on an amalgamation of what all your friends are listening to, which is also enjoyable. Those concerned with privacy will be relieved to know you can prevent the public from seeing your personal listening habits if you so choose. |

harigopalsharma@gmail.com

May 31, 2012

Thanks for highlighting the SEBI Warning.

We are ourselves victim of mis-selling of PMS by SEBI registered high ranking Service provider (Way 2 Wealth …). One of their goal states that they will consistently attempt to outperform market averages (Nifty) and carefully manage risk …. The results are in total contradiction to their goal.

Our Present status.

Our Portfolios , 2 x 5L ,are nearly two years old and at present have heavily bleeded and the service provider thrives as parasite ,charging regularly their fixed management fee chargeable quarterly.

Our Queries are,

- When the Portfolio has significantly diminished is the service provider justified in charging on original corpus. Shouldn't’t it be on actual at the beginning of quarter.

- We tried to know from our service provider, whether their professionalism has, at all, benefited any client or everyone is suffering in silence, the management hides in SEBI directed cocoon that they are prohibited by SEBI to provide this info. Are they justified? Our understanding is that, SEBI safeguards the Investors.

- Is there a FORUM where investor can voice their grievances and forewarn the investor from such gullible Relationship Managers?

Your response will be highly appreciated and is badly needed.

HG Sharma & Prabha Sharma. |

harigopalsharma@gmail.com

May 31, 2012

Thanks for highlighting the SEBI Warning.

We are ourselves victim of mis-selling of PMS by SEBI registered high ranking Service provider (Way 2 Wealth …). One of their goal states that they will consistently attempt to outperform market averages (Nifty) and carefully manage risk …. The results are in total contradiction to their goal.

Our Present status.

Our Portfolios , 2 x 5L ,are nearly two years old and at present have heavily bleeded and the service provider thrives as parasite , charging regularly their fixed management fee chargeable quarterly.

Our Queries are,

- When the Portfolio has significantly diminished is the service provider justified in charging managerial fee based on original corpus. Shouldn't’t it be on actual at the beginning of quarter.

- We tried to know from our service provider, whether their professionalism has, at all, benefited any client or everyone is suffering in silence. While replying , the management hides otocepha in SEBI directed cocoon that they are prohibited by SEBI to provide this info. Are they justified? Our understanding is that, SEBI safeguards the interest of Investors.

- Is there a FORUM where investor can voice their grievances and forewarn the investor from such gullible Relationship Managers?

Your response will be highly appreciated and is badly needed.

HG Sharma & Prabha Sharma. |

1