|

| March 20, 2015 |

|

| Weekly Facts |

|

Close |

Change |

%Change |

| S&P BSE Sensex* |

28,261.08 |

-242.22 |

-0.85% |

| Re/US $ |

62.52 |

-0.01 |

-0.02% |

| Gold Rs/10g |

26,140.00 |

-60.00 |

-0.23% |

| Crude ($/barrel) |

54.29 |

-2.89 |

-5.05% |

| F.D. Rates (1-Yr) |

7.25% - 8.75% |

Weekly change as on on March 19, 2015

*BSE Sensex as on March 20, 2015

|

Impact

Many of you as policyholders may be victims of mis-selling by insurance agents. The thirst to earn luring commissions is what induces them to play a variety of tricks to fool people and garner more business. And if you go to the insurance company complaining about a dishonest agent or a broker; most likely, insurance company would reply in a circumspect manner dismissing its responsibility. All you may get is sympathy and lack not much redressal.

But now to crack the whip, the Insurance Regulatory and Development Authority (IRDA) has recently issued new guidelines on appointment of insurance agents. The said guidelines which come to effect from April 1, 2015 are expected to bring about a number of changes the way insurance policies are sold.

So, what do the new guidelines say?

The new guidelines have introduced even more stringent code of conduct and also have given clear direction on appointment and the termination of an agent. Now, insurance companies would be held responsible for all acts and omissions of their agents. Moreover, if insurance agent fails to observe the code of conduct prescribed by IRDA, the insurance company would be held responsible for that too. In any such case, insurer will have to pay a penalty which may be as high as Rs 1 crore. Also, the IRDA has said any person acting as an agent in contravention to the provisions of the Insurance Act would be liable to a penalty of up to Rs 10,000.

The IRDA has also specified ‘Do's' and ‘Don'ts' for insurance agents. PersonalFN has herein below given some of the high impact ones...

Do's:

- Make the prospect aware of importance of disclosing all material information while buying insurance

- An agent must make the prospect aware of the information needed for insurance contract

- Ensure all relevant documents are available while filing the proposal form

- An agent must disclose his commission, if asked for

- Bring to notice of the insurer all facts that might affect the underwriting process

- Should explicitly recommend the insured to provide a nominee for the policy

- Provide assistance to policyholders for any matter involving the servicing of policy

Don'ts:

- Insurance agents should not provoke prospects for concealing material information

- Agents should not use any multi-level marketing for soliciting and obtaining business

- Agents need to refrain from intervening in insurance proposals introduced by other agents

- They are expected to refrain from offering different rates, advantages, terms and conditions other than those offered by the insurance company

- They should also not induce prospects to cancel new policies with an intent of getting new business

The new guidelines issued by the IRDA are in accordance with the provisions of recently passed Insurance Bill.

PersonalFN is of the view that, the new guidelines may help curb mis-selling, as insurance companies would be held responsible now for non-compliance of agents. Strong rules pertaining to code of conduct, appointment and disqualification of agents may provide policyholders more legal defence in case of mis-selling. Moreover, since insurance companies have to pay fine for misdeeds of their agents they would proactively discourage mis-selling. Agents too would serve policyholders better with a penalty clause set for them in case if they contravene the Insurance Act.

PersonalFN has always believed that, insurance should be viewed from an indemnification point of view and not to reap profits. It is vital for you to buy an optimal insurance cover in the interest of your financial wellbeing. While you buy life insurance, keep your insurance and investment needs separate. Don't fall for investment-cum-insurance plans as they sub-optimally cover risk for the premium charged. Term insurance remains one of the most cost effective ways for protecting your dependants from the financial loss. Charting a financial plan would help you understand how much insurance you need. So, feel free to talk to our investment consultant at PersonalFN for prudent guidance on financial planning and insurance.

Do you think insurance companies would now take proactive steps to discourage mis-selling? Share your views

|

Impact

The Budget 2015-16 set the foundation to provide social security by announcing array of schemes. A step in that direction which can leave individuals with a bigger nest egg for retirement, the Government now is considering making substantial changes to the law ruling Employee Provident Fund (EPF).

It has suggested doing away with mandatory 12% contribution by employees, in certain cases, while retain the obligation for employers. Also the labour ministry is planning to expand scope of wages beyond the basic pay. Thus contribution to EPF would not be just restricted only to 12% of their basic pay, but also be extended to include allowances. Furthermore, the Government also wants to expand the coverage of EPF even to companies employing less than 20 people. Also, there is a proposal to provide more strength to appellate tribunal and impose penalties and make effective recoveries from defaulting companies.

PersonalFN is of the view that although everything discussed above is just in a ‘proposal' stage so far, if it gets through, may have a significant impact on take home salaries of employees. It would also mean a higher burden of salary on the employer.

Hence if you are salaried individuals it would be imperative to take cognisance, as it has an effect on your household budget. Nonetheless, from a long term point of view, to plan your retirement, it would be positive since it can leave you with a greater nest egg. But you should not rely only on your EPF account for your retirement and invest in various investment avenues in accordance to your financial plan. A well-crafted retirement plan may help you address most of your worries pertaining to retirement. Please remember, retirement planning is an on-going, lifelong process that takes enormous commitment and discipline to receive the final pay-off. So engage in prudent retirement planning!

|

Impact

World cup mania is intensifying in India as Indian team has entered quarterfinals with a clean sweep in league matches. Likewise, as market rally has sustained over last 16-18 months, there is a great zeal among mutual fund houses to garner fresh money. They are not leaving any stone unturned to increase their asset base. After having launched dozens open ended and close ended actively managed equity funds, now fund houses have turned to Exchange Traded Funds (ETFs).

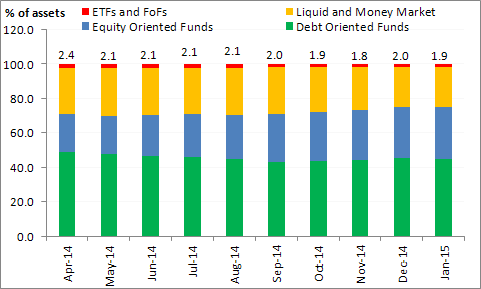

Are ETFs popular in India?

Although Exchange Traded Funds (ETFs) have been very popular in developed markets, they are yet to gain acceptance in India. ETFs and Fund of Funds (FOF) together don't form even 5% of total Asset under Management (AUM) of mutual funds in India.

Exchange Traded Funds- Not-so-popular in India

(Source: AMFI, PersonalFN Research)

ETFs are actively traded index funds that replicate a targeted index. Their aim is not to outperform the underlying index, but to match the returns generated by the index in a cost effective way. The main reason for their being popular in developed markets is lower possibility of underperformance. In India, the concept has not become popular primarily because actively managed funds have performed well by and large. Almost half the assets managed under ETFs are focus on movement of Gold prices in India. Moreover, the ETFs have not been as cost effective as they are expected to be in India.

To read more about this news and PersonalFN's views on it, please click here.

|

Impact

In the budget speech finance minister, Mr Arun Jaitley said that a very important dimension to our tax administration is the fight against the scourge of black money. Hence it was also mentioned that a Bill for a comprehensive new law to deal with black money would be introduced in the current session of the parliament and key features of the new law on black money were also articulated.

The union budget 2015-16 also made Permanent Account Number (PAN) mandatory for any purchase or sale exceeding the value of Rupees 1 lakh. Thus now if you are out to buy gold (be it bars, coins and / or jewellery) exceeding a value of Rs 1 lakh, quoting PAN will be mandatory for you.

To know more about this story and to read our views, please click here

|

- While Assets under Management (AUM) of Indian mutual fund industry in equity schemes is on the rise (thanks to sharp market rallies), some players of the industry are exiting. It appears that their investments in Indian market are not reaping the desired results. The Indian mutual fund industry seems to be undergoing a phase of consolidation where those exiting are finding buyers within the industry.

After, Fidelity, Morgan Stanley, ING, Daiwa, and PineBridge; it is believed that now JPMorgan Mutual Fund wants to exit its mutual fund business in India. It is said that high cost structures, slow decision making and appetite to grow AUM at the expense of profitability may be making it difficult for AMCs to run their businesses productively.

PersonalFN is of the view that, investors should be watchful to such developments. When AMCs are sold, you must pay attention to who's buying the business. Whether to continue or to discontinue from the scheme should depend on a number of factors such as track record of the fund house that is taking over the schemes, effectiveness of its risk management processes and team strength of the fund house. Investing in process driven and consistently performing funds is important for generating superior returns on your portfolio in the long run.

|

Multi-Level Marketing: It is, “a strategy that some direct sales companies use to encourage their existing distributors to recruit new distributors by paying the existing distributors a percentage of their recruits' sales. The recruits are known as a distributor's "downline." All distributors also make money through direct sales of products to customers. Amway is an example of a well-known direct-sales company that uses multi-level marketing.”

(Source: Investopedia)

|

Quote : "Derivatives are financial weapons of mass destruction." - Warren Buffett

|

|

|

|

© Quantum Information Services Pvt. Ltd. All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Pvt. Ltd. 101, Raheja Chambers, 213, Nariman Point, Mumbai - 400021. Tel: +91 22 6136 1200

Website : www.personalfn.com CIN: U65990MH1989PTC054667

|