Over the past few weeks, various factors such as the government's borrowing programme, an uptick in inflation, etc. have led to a rise in bond yields. This has driven the prices of bonds lower (since interest rates and bond process are inversely related) and therefore investors may have to be content with lower returns on debt mutual funds as compared to the last few years.

But this should not tempt you to chase higher returns by taking higher credit risk. Remember the main aim of the debt portfolio is to provide stability and manage downside risk during uncertain and volatile market conditions. Earning higher returns is best achieved through your equity portfolio.

If you are looking for a relatively stable, safer, and liquid scheme in the debt mutual fund category, you can consider investing in Banking & PSU Debt Fund. It can offer you the benefit of Corporate bond funds (that invests in top-rated instruments of private issuers), but at lower credit risk.

Image by jcomp - www.freepik.com

Image by jcomp - www.freepik.com

What are Banking & PSU Debt Funds?

Banking and PSU debt funds are mandated to invest in a minimum 80% of its assets in debt instruments of banks, Public Sector Undertakings, and Public Financial Institutions.

Portfolios of Banking and PSU Funds mainly comprise of government and quasi-government securities along with some exposure to top names in the banking industry. These companies enjoy high-credit rating (AAA or equivalent) and government backing, which makes it highly liquid and less prone to credit risk.

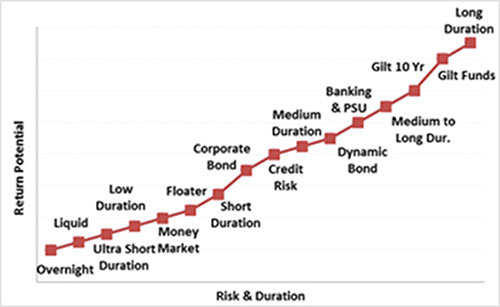

Graph: How is a Banking & PSU Debt Fund placed on the Risk-Return spectrum?

For illustration purpose only

For illustration purpose only

These funds usually invest in debt securities that mature over the short to medium term with some allocation to longer term maturity papers. So if you are looking to invest in securities that have government backing but do not have the long term investment horizon to invest in Gilt funds, then Banking & PSU funds can be a worthy option.

Banking & PSU Debt Funds have the potential to generate higher returns than bank fixed deposits but at the same time carries slightly higher risk. This category is suitable for investors with a moderate risk profile and an investment horizon of 2-3 years.

Table: Performance scorecard of Banking & PSU Debt Fund

Data as on April 09, 2021

(Source: ACE MF)

*Please note, this table only represents the best performing Banking & PSU Debt Funds based solely on past returns and is NOT a recommendation. Mutual Fund investments are subject to market risks. Read all scheme related documents carefully. Past performance is not an indicator for future returns. The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

A combination of multiple rating downgrades and defaults in the past followed by the more recent Franklin Templeton fiasco caused wary investors to shun the once attractive credit risk category of debt fund and opt for safer alternatives such as Banking & PSU Debt Funds. Banking & PSU Debt Fund category not only fares well on liquidity and safety parameters, it also has an impressive performance track record.

Do note that while credit risk in this category is low, it is prone to interest rate fluctuation. When interest rates rise, these funds generate lower returns. Moreover, though Banking & PSU Funds may be termed relatively safer, a slight element of credit risk cannot be ruled out. It shouldn't be considered as complete risk-free option. Therefore, it is important to select Banking & PSU Debt Fund carefully.

Best Banking & PSU Debt Funds to invest in 2021:

Some of the best Banking & PSU Debt Funds that fare well on both quantitative and qualitative parameters based on our analysis and research at PersonalFN are:

- Axis Banking & PSU Debt Fund

- IDFC Banking & PSU Debt Fund

- LIC MF Banking & PSU Debt Fund

- Sundaram Banking & PSU Debt Fund

- Aditya Birla SL Banking & PSU Debt Fund

Here are the facets you need to look into to select the best Banking & PSU Debt Fund:

Quantitative parameters

Check whether the fund has a decent track record of delivering adequate and stable returns across time horizons when compared to the category average and the benchmark index. Furthermore, the fund should be able justify the returns by generating competitive risk-adjusted returns for its investors. To determine whether the fund has rewarded its investors well for the risk they have taken, assess risk-reward ratios like Sharpe Ratio, Sortino Ratio, and Standard Deviation over a 2-year period.

So when you are shortlisting funds for your portfolio, give preference to those funds that stand strong on risk-reward parameters.

Qualitative parameters

The fund should be well-placed to determine the general maturity range for the portfolio after considering the prevailing political conditions, the economic environment (including interest rates and inflation), the performance of the corporate sector, and general liquidity as well as other considerations in the economy and markets.

In addition, ensure that fund resists from taking high credit risk by limiting exposure to moderate and low-rated securities and makes optimal use of portfolio diversification to mitigate risk. The performance of Banking and PSU debt fund is influenced by the coupons and maturity of their portfolio holdings along with the credibility of the issuers they hold in the portfolio, and may have severe impact on valuation in case of an unexpected default by any issuer.

The fund's portfolio should be well-diversified across securities issued by various companies and group of companies. Remember that a concentrated portfolio can expose you, the investor, to higher risk. Additionally, keep a tab on the expense ratio of the fund.

Most importantly, always give higher importance to fund houses that follow robust investment processes and systems along with sound risk management techniques in place.

Watch this short video on the lessons an investor can remember while investing in Debt Mutual Funds.

Outlook for Banking & PSU Debt Funds in 2021

We are witnessing a relentless resurgence of COVID-19 infections that poses a threat to economic recovery. However, in view of the vaccination drive being sped up and expectation of the gradual release of pent-up demand along with growth measures from the government, RBI has retained the GDP growth projection at 10.5% for FY 2021-22.

Given the government's massive borrowing programme to support economic growth, bond yields may continue to harden. Moreover, due to the restrictions imposed to curb the second wave of COVID-19, inflation is expected to witness a spike, which will reduce the chances of RBI cutting rates further.

This factors point out that the present interest rate cycle has bottomed out. Therefore, funds with predominant investments at the longer end of the yield curve could turn riskier (may encounter high volatility) in the foreseeable future.

Banking & PSU Debt funds with shorter portfolio duration of 1-3 years may be better placed to take advantage of the accrual opportunities in this space and help survive rising interest rate conditions. Investors looking for a less volatile fund in the debt fund category and having a time horizon of at least 2 to 3 years can consider investing in Banking & PSU Debt funds.

PS: If you are looking for quality mutual fund schemes to add to your investment portfolio, I suggest you subscribe to PersonalFN's premium research service, FundSelect. Currently, with the subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect.

Under DebtSelect, we give high weightage to schemes displaying worthy portfolio characteristics. We avoid debt mutual fund schemes that aim for higher yields by taking undue higher credit risk with substantial exposure in instruments issued by private issuers.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds