Lok Sabha elections 2019 are underway.

Will BJP led NDA get another term?

That's been the general consensus on the Dalal Street though.

Will markets rally if that happens?

In 2014, the markets staged a rally before as well as after Lok Sabha elections.

And who will save the markets if BJP loses like it lost with the 'India shinning campaign' about 15 years ago?

But do you remember the mightiest bull market rally that happened in the UPA-1 era between 2004 and 2007? Whoever invested in markets after they fell post the Lok Sabha-2004 elections would have made a fortune in the following three years.

Similarly, investors shied away from markets in 2009, 2013, and 2016 when the markets perhaps presented exciting buying opportunities. In contrast, many investors missed to cash in their gains in 2007, 2010, and 2017.

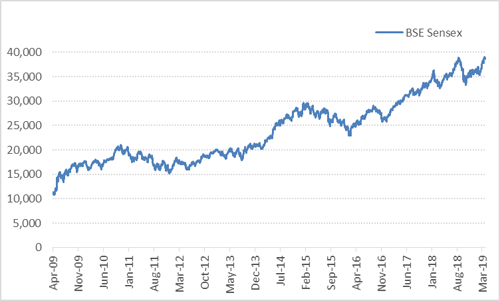

Graph: BSE Sensex-10 year movement...

Data as on April 10, 2019

(Source: BSE)

Predicting markets is purely guesswork. But identifying great investment opportunities, when markets go overboard with their greed or fear and behave irrationally, is a skill. That's a contrarian approach.

Let's understand contra investing in detail...

Before we touch upon contra investing, you might want to read more about the contrarian approach first.

Going left when the whole world is moving right isn't a contrarian approach. Going left because you think, people are WRONG in flocking their ways to right is a contrarian approach.

In simple words, disagreeing with the consensus view just because many people share it isn't a contrarian approach. But disagreeing with the consensus view because you have an equally strong and opposite view, that's a contrarian approach.

If you got the difference, understanding contra investing would be a cakewalk for you.

According to the norms of the capital market regulator, open-ended equity funds investing at least 65% of their assets in equity and equity oriented schemes, and following the contrarian philosophy are classified as contra funds.

Under contra investing, the fund manager focuses on investing against the prevailing market trend in assets that are performing poorly and selling them when they perform well. The approach focuses on identifying neglected stocks that are undervalued today (trading at lower P/E multiple or P/BV), but have a potential of growing in the long-term.

Hence broadly if we observe, contra investing is a subset of value investing. But a noteworthy point is that contra investing is far more complex than value investing, as the objective is picking stocks which are dumped by the market (available at a cheap price) in the short-term, but nonetheless have the potential to gain in the long-term when the market recognises its true potential. Hence by doing so, contra investing aims at sailing against the tide by betting on "out of favour" stocks / sectors, in an attempt to gain in the long-term.

Is contra investing risky?

If you consider various categories of equity mutual funds, contra funds are riskier than multi cap funds since it requires them to go against the market. Contra funds can sometimes take sector specific bets and depending on portfolio weightage, may even become as risky as focused funds.

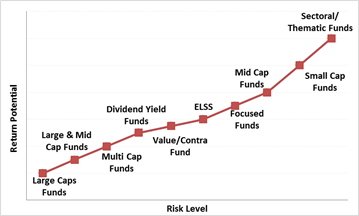

(For illustration purpose only)

Sometimes markets correct themselves quickly due to which a contra fund has to exit a stock more quickly than it had anticipated earlier. On the other hand, there are times when the markets stay irrational for long duration, thereby disturbing the scheme's calculations.

Therefore, besides uncertainties, incurring high costs on account of churning is another risk associated with contra funds.

What investors shall do at this juncture?

First, stop worrying about election outcomes. Let's not waste time guessing the election outcomes.

Election results won't matter to markets beyond 2-3 months. After that, it's just earnings and the overall performance of the economy that will decide the fate of the market.

If you bet on the election outcomes to decide whether you should invest in equity mutual funds, it would be speculation, which is unhealthy for wealth creation.

So what should your investment strategy be in the coming months?

If you think, markets have gone overboard in assuming BJP's victory, you might want to rebalance your portfolio and reduce the exposure to equity.

[Read: Unsure When To Review Your Mutual Fund Portfolio? Read This... ]

On the other hand, if you think NDA government will get a second term and if you are underinvested in equity assets, you might want to increase your exposure. At this juncture, take the SIP (Systematic Investment Plan) route when investing fresh money.

In short, it's time to revisit your original, personalised asset allocation to know if your portfolio is skewed towards any particular asset class.

From a diversification standpoint, contra funds-which are a subset of value funds -can be considered to take exposure to diversified equity funds. That said, before you invest a contra fund pay attention to your overall allocation to equities recognizing your risk appetite, investment objectives and investment time horizon.

Hence if you are investing in contra funds please ensure that:

It's time to check the performance...

Before SEBI classification norms came into effect, mutual funds were using their discretion to qualify a fund as contra or a value. However, according to SEBI categorisation norms, fund houses can now offer either a value fund or a contra fund. Hence, at present, only three contra funds are on offer. Mutual fund houses seem to have favoured value funds over contra funds.

[Read: Is Mutual Fund Categorization Affecting Your Portfolio? Review It Now!]

Table: How have contra funds performed?

Data as on April 02, 2019

(Source: ACE MF)

*Please note, this table only represents the best performing Contra Funds based solely on past returns and is NOT a recommendation.

Mutual Fund investments are subject to market risks. Read all scheme related documents carefully.

Past performance is not an indicator for future returns. The percentage returns shown are only for an indicative purpose.

Speak to your investment advisor for further assistance before investing.

Contra funds might underperform markets in the short run, as they have performed in 2018. Moreover, within this category, the performance of funds offered by various mutual fund houses may vary substantially depending on the portfolio allocations.

For example, SBI Contra Fund had a bad patch in 2018, which seems to have negatively affected even its 3-year performance.

Nonetheless, Invesco India Contra Fund and Kotak India EQ Contra Fund have done fairly well across timeframes.

It's noteworthy that consistency matters a lot at the time of selecting a contra fund.

Therefore, to select a winning contra fund, adopt a combination of quantitative and qualitative criteria.

Quantitative criteria:

-

Performance and risk analysis

This parameter analyses the fund's consistency in performance across various market periods with decent risk-adjusted returns. The fund should be ranked on quantitative parameters like rolling returns across short-term and long-term durations, such as 1-year, 3-year, and 5-year periods, and on risk-reward ratios like Sharpe Ratio, Sortino Ratio, and Standard Deviation over a 3-year period.

-

Performance across market cycles

To ensure that the fund can perform consistently across multiple market cycles, compare the performance of the schemes vis-a-vis their benchmark index across bull and bear market phases. A fund that performs well on both sides of the market should rank higher on the list.

Qualitative Parameters:

-

Portfolio Quality

The portfolio quality of a mutual fund scheme points at how it is likely to perform in the future. Here's what you should pay attention to:

Adequate Diversification - The fund should not hold a highly concentrated portfolio. A concentrated portfolio heightens the risk involved. Hence, the portfolio of a fund should be well-diversified and the exposure to the top-10 stocks should be ideally under 50% while concentration to one particular sector should not exceed 30-35%.

Low Churn - Engaging in high churning of your portfolio can result in trading and high turnover cost. Therefore, consider the portfolio turnover ratio and expenses and penalise funds involved in very high churning.

-

Quality of Fund Management

Further, check the fund manager's experience, the workload, consistency in clocking returns, and proportion of the AUM (Assets Under Management) of the fund house that are actually performing. Therefore, check the following points before investing:

The fund manager's work experience - They should have a decent experience in investment research and fund management, ideally over a decade. But note that experience isn't always enough. Some schemes managed by fund managers with 15-20 years of experience haven't necessarily done consistently well for a long time.

The number of schemes managed - A fund manager usually manages multiple schemes. Thus, you need to check if the fund manager is not loaded with a large number of schemes. If they are managing more than five open-ended funds, that should raise a red flag.

The efficiency of the fund house in managing your money - You need to check if most of the schemes from the fund house are doing consistently well or a handful of them. A fund house that performs well across the board is an indication that sound investment processes and risk management techniques are in place.

Yes, we know that the above list is a lot for an average investor to look at. It involves a lot of number crunching and much of the data is not easily accessible. But if you do need to narrow down on the top funds, these factors are of utmost importance.

Watch this short video on selecting mutual fund schemes:

Here are points to remember when you invest in mutual funds:

-

Clearly identify your financial goals.

-

Recognise the financial goals you wish to achieve and align your mutual fund investment to them.

-

Gauge the time horizon before the financial goals befall.

-

Assess your risk appetite. Only if you have a high-risk appetite and longer time horizon (at least 3-5 years) for the fulfilment of goals, invest more in equity-oriented mutual funds; otherwise, stick to debt mutual funds and other fixed-income investments.

-

Based on your risk appetite, draw up a personalised asset allocation chart and invest accordingly.

-

Keep reviewing your investment so that you're on track to accomplishing your envisioned financial goals.

Editor's Note: If you are open to taking calculated risks and investing in equity funds, PersonalFN can help you pick hidden gems or lesser-known funds that are capable of generating big gains for you.

PersonalFN has released a report 5 Undiscovered Equity Funds With High Growth Potential especially for investors like you.

We, at PersonalFN, have tested the viability of Undiscovered Funds featuring in this report by applying a stringent selection process.

These undiscovered funds can help you counter inflation by a substantial margin.

Subscribe today!

Author: PersonalFN Content & Research Team