4 Best Tax Saving Mutual Funds for 2025 – Top ELSS Funds in India

Rounaq Neroy

Dec 11, 2024 / Reading Time: Approx 25 mins

Listen to 4 Best Tax Saving Mutual Funds for 2025 – Top ELSS Funds in India

00:00

00:00

If you are aiming to get two birds with one stone, i.e. build wealth and save tax, then investing in some of the best Tax Saving Mutual Funds, also known as the Equity-Linked Saving Scheme (ELSS) is a worthwhile proposition.

As you know, tax saving is an integral part of our wealth creation journey, as a penny legitimately saved from tax, is a penny earned. ELSS, a taxing save avenue, is particularly a meaningful choice if you are willing to take some market-linked risk and the investment objective is capital appreciation over a time horizon of 3 years or more.

In this article, I will reveal which are the 4 best Tax Saving Mutual Funds or ELSS for 2025. But before that let's understand some basics...

What is ELSS?

SEBI defines ELSS (Tax Saving Mutual Funds) as equity-oriented mutual funds that invest a minimum of 80% of their total assets in equity and equity-related instruments in accordance with the equity-linked savings scheme 2005, as notified by the Ministry of Finance.

These funds come with a mandatory lock-in period of 3 years and offer tax benefits.

The 3 years lock-in for ELSS inculcates the needed discipline of staying invested for the long-term considering that your hard-earned money is invested by the fund manager in equity and equity-related instruments with the objective of capital appreciation.

Most ELSS or tax-saving mutual funds hold the mandate to invest flexibly across market capitalisation and sectors. Accordingly, most ELSS hold a diversified portfolio and are usually market-cap and sector-agnostic. As regards style, an ELSS may follow the growth style or value style of investing or a combination of both.

Having said that, enough care should be taken when selecting ELSS or tax-saving mutual funds. This is because not all ELSS are worth your hard-earned money. Watch this video to know which are the 4 Best ELSS or tax-saving mutual funds in India to invest in 2025:

Some ELSS or tax-saving mutual funds may expose you to high risk but disappoint you when it comes to the risk-adjusted returns. It would be imprudent to consider only the past returns or star ratings, as they are in no way indicative of future returns.

Also, it is not necessary that an ELSS with a higher AUM is better. The higher the AUM, the better the scheme would be in terms of delivering its investment objective is a myth.

[Read: Should You Invest In A Mutual Fund Scheme Looking At Its AUM?]

Table 1: Popular ELSS (Tax Saving Mutual Funds) in India

| Scheme Name |

AUM (Rs Crore) |

| Axis ELSS Tax Saver Fund |

36,373 |

| SBI Long Term Equity Fund |

27,847 |

| Mirae Asset ELSS Tax Saver Fund* |

24,896 |

| DSP ELSS Tax Saver Fund |

16,835 |

| HDFC ELSS Tax saver |

15,945 |

| Aditya Birla SL ELSS Tax Saver Fund |

15,746 |

| Nippon India ELSS Tax Saver Fund |

15,666 |

| ICICI Pru ELSS Tax Saver Fund |

14,210 |

| Quant ELSS Tax Saver Fund |

10,799 |

| Canara Rob ELSS Tax Saver |

8,817 |

The list of funds cited here is not exhaustive.

The securities quoted are for illustration only and are not recommendatory.

AUM data as of November 30, 2024

*Mirae Asset ELSS Tax Saver Fund's AUM is as of October 2024, as its portfolio data for November wasn't available at the time of covering this piece.

(Source: ACE MF, data collated by PersonalFN)

Why Prefer ELSS Over Other Tax-Saving Instruments - Advantages of Investing In ELSS

Investing in ELSS offers investors the lowest lock-in period compared to traditional tax-saving instruments, such as the Public Provident Fund (PPF), National Savings Certificate (NSC), Tax-saver Bank FDs, etc.

The NSC and tax-saving FD both have a lock-in period of 5 years, while in the case of the Public Provident Fund (PPF), the lock-in is 15 years. And as regards, the National Pension System (NPS) money is locked in till the age of 60 years.

Table 2: Lock-in Period and Return Potential of ELSS versus Other Tax-Saving Avenues

| Tax Saving Instrument |

Return Potential |

Lock-in period |

| Equity-Linked Saving Scheme |

High* (market linked) |

3 years |

| Unit-Linked Insurance Plan |

Average-to-High# (market-linked) |

5 years |

| National Saving Certificate |

7.70% |

5 years |

| 5-Yr Tax Saver Bank FD |

6.50%$ |

5 years |

| Senior Citizens Savings Scheme |

8.20% |

5 years |

| Public Provident Fund |

7.10% |

15 years |

| Sukanya Samriddhi Yojana |

8.20% |

21 years |

| National Pension Scheme |

Low-to-High@ (market-linked) |

Till 60 years of age |

*Depends on your ELSS selection.

#Depends on the type of asset class orientation of the fund you choose under ULIP.

$ 5-Yr Tax Saver Bank FD interest rate considered is that of SBI.

The current rate of interest as applicable is taken for other tax-saving instruments. Interest rates are subject to change.

@Depends on the scheme chosen under the NPS

In addition, when compared to other popular tax-saving instruments such as tax-saving FD and PPF, ELSS has the potential to reap higher returns for its investors, which makes it a worthy avenue for tax efficiency and long-term wealth creation.

Both individuals and HUFs can invest in ELSS and claim a deduction of up to Rs 1.50 lakh in a financial year under Section 80C of the Income Tax Act, 1961.

Graph 1: Top stock holdings of ELSS (Tax Saving Mutual Funds) in India

The securities quoted are for illustration only and are not recommendatory.

The securities quoted are for illustration only and are not recommendatory.

AUM data as of November 30, 2024

(Source: ACE MF, data collated by PersonalFN)

Who Should Consider Investing In ELSS?

Even though ELSS or Tax Saving Mutual Funds offer various benefits, they may not be suitable for all types of investors. Being equity-oriented, ELSS have the potential to better returns than some traditional tax-saving avenues, however, you should also be ready to assume market volatility and have a high-risk appetite for equities.

The returns you would earn on ELSS will be market-linked, not fixed, and shall depend on how the market as well as the securities in the underlying portfolio of the scheme or tax-saving mutual fund performs.

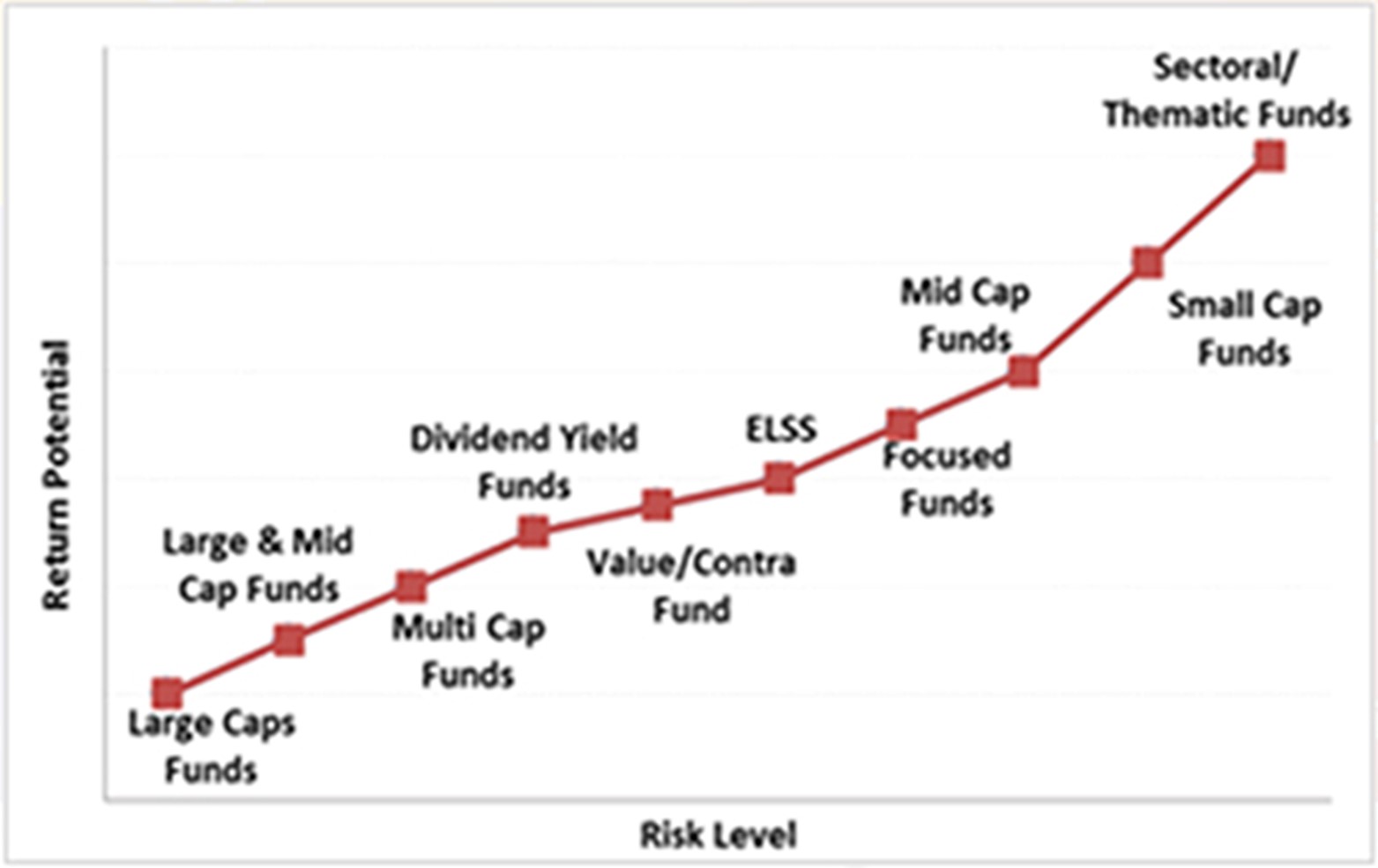

Graph 2: Risk-Return Spectrum of Equity Funds

For illustration purposes only.

For illustration purposes only.

Graph created by PersonalFN Research.

Broadly, those who are young, have a high-risk appetite, looking for capital appreciation (and not interest as in the case with many other traditional tax-saving avenues), wish to clock better real returns (also known as inflation-adjusted returns) in the endeavour to achieve the financial goals, and/or have an investment time horizon of 3 years+ could consider investing in ELSS. Keep in mind that ELSS or Tax Saving Mutual Funds carry high risk (since your money is invested in equities).

Investments in equities take time to grow and generate meaningful returns. There could be short-term underperformance. So, don't limit your time horizon only until the lock-in period; you may have to hold on to the investment beyond the mandatory lock-in period.

If you are a risk-averse investor, steer clear from investing in ELSS or Tax Saving Mutual Funds, and instead consider relatively safer tax-saving instruments such as PPF, NSC, Tax-saver Bank FD, etc.

[Read: Why ELSS Is Your Best Choice to Build Wealth and Save Tax]

How To Select The Best ELSS For Investment

At present, there are over 40 ELSS or Tax Saving Mutual Funds, in India offered by various mutual fund houses. So, there is a plethora and hence selecting the right scheme for the portfolio can be challenging.

When selecting ELSS for the portfolio, it is important to avoid making the decision based on superficial parameters such as the popularity of the scheme, its short-term track record, or the NAV of the scheme.

Instead, one should evaluate the schemes on various quantitative and qualitative parameters to narrow down on those that have consistently performed well.

Here's what you should consider:

✓ Past performance across various time frames (6-months, 1-year, 2-year, 3-year, 5-year, 10-year, since inception)

✓ The performance across market phases (bull and bears)

✓ The level of risk it exposes its investors (as denoted by the standard deviation)

✓ The risk-adjusted returns clocked (as reflected by the Sharpe and Sortino Ratio)

✓ The expense ratio (as it weighs on the returns you make)

✓ The portfolio characteristics (such as the top-10 holdings, top-5 sector exposure, how concentrated/diversified is the portfolio, the market capitalisation bias, sector concentration, portfolio turnover, etc.)

✓ The credentials of the fund management team (i.e., the experience of the fund manager, the number of schemes he/she manages, the track record of the mutual fund schemes under his/her watch, the experience of the research team)

✓ The proportion of AUM of the fund house actually performing (to check the efficiency of the fund house and whether it is an asset manager or a mere asset gatherer)

✓ And on the whole, the investment process & systems are followed at the fund house.

Watch this video:

[Also read: How to Select the Best ELSS for Tax-saving]

Should Individuals Consider Investing in ELSS Under the New Income Tax Regime?

Intending to make the new tax regime attractive for taxpayers, the government during its full Union Budget 2024-25 presented in July 2024, tweaked the income tax slabs, encouraging many to opt for the new tax regime.

Further, the union budget 2024-25 introduced a major change to the capital gain tax on mutual funds.

[Read: Mutual Fund Taxation - Here Are the Key Changes After the Union Budget 2024-25]

However, no changes were made to deductions under Sections 80C, 80D, and 80E, Section 24, as well as HRA and LTA, for those under the Old Tax Regime.

Note, for those whose taxable income is high (over Rs 20 lakh) and are paying home loan EMIs, and insurance premiums for self and dependants, it might still be beneficial to stay in the old tax regime. Such investors can invest in tax-saving instruments, such as ELSS and others, to avail of the deduction under Section 80C.

That being said, even if you opt for the new tax regime considering its benefit, tax-saving instruments can still form a part of one's portfolio for wealth creation purposes, if they align well with your risk profile and financial needs.

Instruments such as ELSS that invest predominantly in equities can help you earn better gains and accumulate a bigger corpus for various financial goals. But you ought to give enough time for funds to grow.

How To Invest In ELSS?

You can invest in mutual funds offline by visiting the nearest branch of a mutual fund house or a mutual fund distributor and submitting a duly completed application form along with other relevant documents such as proof of identity, proof of address, cancelled cheque leaf, and paying the required investment amount.

Alternatively, you can choose to invest in mutual funds online vide some of the best apps or online platforms from the comfort and convenience of your home, office or wherever you are.

[Read: Best Platforms to Invest in Mutual Funds]

Note, that mutual fund platforms offer benefits such as:

-

Help keep track of track of all your mutual funds in one place with the portfolio tracker.

-

Provide portfolio alerts.

-

You get insights on New Fund Offers and other developments in the mutual fund investing landscape.

-

Some even provide research-backed recommendations to build your portfolio.

-

Facilitate an online portfolio review.

Depending on whether you are a seasoned investor or a newbie, choose your platform to invest in mutual funds thoughtfully.

You could also invest through the official website of the respective Asset Management Companies (AMCs).

[Read: How to Invest in Mutual Funds]

When investing in ELSS, you may make a lump sum investment or take the Systematic Investment Plan (SIP) route, but in the case of SIPs, keep in mind that every SIP instalment will be subject to a lock-in of three years.

[Read: The Ultimate Guide to the Best SIP Plans for 2025]

Further, I suggest opting for the Direct Plan over the Regular Plan. The lower expense ratio under the Direct Plan may help you clock slightly higher returns than the Regular Plan.

Similarly, when you are looking for capital appreciation over the long term (3-year+ horizon), choosing the Growth Option over the IDCW Option is sensible.

[Read: IDCW vs Growth Option: Which One Should You Opt for?]

Which Are the Best ELSS (Tax Saving Mutual Funds) For 2025?

With over 40 ELSS available for investment, finding the best scheme is not an easy task. Considering the selection parameters rolling returns, risk ratios and the portfolio characteristics of ELSS, among others as discussed above, at PersonalFN we have identified 4 best ELSS for 2025.

Table 3: List of Best ELSS For 2025

| Scheme Name |

Absolute (%) |

CAGR (%) |

Ratio |

| 1 Year |

3 Years |

5 Years |

7 Years |

SD Annualised |

Sharpe |

Sortino |

| SBI Long Term Equity Fund |

53.56 |

27.14 |

24.33 |

18.07 |

14.52 |

0.35 |

0.72 |

| HDFC ELSS Tax saver |

43.32 |

25.76 |

20.60 |

15.32 |

13.20 |

0.34 |

0.74 |

| Bank of India ELSS Tax Saver |

49.34 |

23.48 |

27.53 |

21.01 |

15.99 |

0.24 |

0.47 |

| Parag Parikh ELSS Tax Saver Fund |

33.51 |

22.20 |

25.67 |

-- |

10.89 |

0.34 |

0.70 |

| Category average |

37.99 |

19.98 |

20.73 |

16.50 |

14.39 |

0.24 |

0.47 |

| BSE 500 - TRI |

35.18 |

18.60 |

19.62 |

16.12 |

14.54 |

0.19 |

0.38 |

| NIFTY 500 - TRI |

35.57 |

18.60 |

19.46 |

15.97 |

14.55 |

0.19 |

0.38 |

Data as of December 9, 2024

The list of funds cited here is not exhaustive.

Returns expressed are rolling returns in % and calculated using the Direct Plan-Growth option.

Standard Deviation indicates Total Risk and Sharpe Ratio measures the Risk-Adjusted Return. They are calculated over 3 years assuming a risk-free rate of 6% p.a.

*Please note, that this table represents

past performance.Past performance is not an indicator of future returns.

The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

(Source: ACE MF, data collated by PersonalFN)

Let us now take a look at what makes these funds the best ELSS (Tax Saving Mutual Funds) for 2025...

Best ELSS (Tax Saving Mutual Fund) for 2025 #1 - SBI Long Term Equity Fund

Incepted 31 years ago, in March 1993, the SBI Long Term Equity Fund (formerly known as SBI Magnum Tax Gain Fund) is one of the oldest and most well-regarded schemes in the ELSS category.

SBI Long Term Equity Fund (SLTEF) follows a value-conscious investment approach, maintaining a well-diversified portfolio of stocks across different sectors and market caps.

SLTEF experienced a prolonged period of underperformance from 2016 to 2019 and again in 2021, primarily due to the value investing style falling out of favour. Despite this, the fund has made a remarkable recovery during the ongoing bull market and now holds a strong position among its peers.

SLTEF has benefited from rallies in Finance, Power, Consumption, and PSU stocks, and currently ranks as one of the top performers across most time periods, significantly outperforming its benchmark.

The recent superior performance has helped improve its returns over the short to medium time frames. Its solid long-term performance has led to substantial growth in its AUM, making it the second-largest scheme in the ELSS category.

Despite exposing its investors to slightly higher risk (as denoted by the) than the category average, the fund has justified its performance considering the risk-adjusted returns. The fund's Sharpe Ratio and Sortino ratio, which measure risk-adjusted performance, are among the best in the category and have comfortably outperformed the benchmark.

SLTEF has shown impressive performance through various market phases. With its focus on fundamentally strong, high-potential stocks, the fund has not only managed to protect against downside risk better than the benchmark during bearish phases but has also delivered solid alpha over the benchmark index.

Table 4A and 4B: Fund Snapshot - SBI Long Term Equity Fund

Portfolio data as of November 30, 2024.

Portfolio data as of November 30, 2024.

Returns and NAV data as of December 9, 2024.

The securities quoted are for illustration only and are not recommendatory.

(Source: ACE MF, data collated by PersonalFN)

SLTEF has the mandate to invest across the market cap and sectors to benefit from diversification. It usually holds around 60-65 stocks in its portfolio spread across market caps and sectors.

In the last one year, SLTEF has been investing in large caps with a focus on the margin of safety. SLTEF follows a value bias to pick stocks trading below their intrinsic value. It also lays emphasis on sectoral themes that are expected to grow over the medium to long term. The fund prefers to hold most of its stocks with a long-term view even if they fail to pay off as expected in the short run.

SLTEF has been managed by Mr Dinesh Balachandran since September 2016. He has an industry experience of over 20 years, primarily as Research Analyst. By qualification, Balachandran is a B.Tech (IIT-B), MS (MIT, USA), and CFA Charter holder.

Best ELSS (Tax Saving Mutual Fund) for 2025 #2 - HDFC ELSS Tax Saver Fund

HDFC ELSS Tax Saver Fund (HTSF) is one of the oldest schemes in the ELSS category. Launched in March 1996, the HDFC ELSS Tax Saver Fund boasts an impressive long-term performance record and has generated a remarkable CAGR of about 23.7% since its inception (as of December 9, 2024).

Its investment philosophy is centred on a blend of growth and value strategies, with a focus on identifying fundamentally strong, high-conviction stocks that offer attractive valuations. Unlike momentum-driven funds, HTSF avoids short-term tactical bets, preferring to hold stocks with long-term potential, even if it leads to occasional underperformance.

HTSF's journey has not been without challenges. The fund faced rough patches, particularly in 2015 and between 2018 to 2021, as its value-oriented strategy fell out of favour. These phases saw the fund struggling to keep pace with its benchmark and more growth-focused peers.

Adding to this, frequent changes in fund management during the past decade raised concerns. However, the fund has since made a strong comeback, especially from 2021 onwards, with its investment strategy paying off as market conditions turned favourable for its high-conviction picks.

Its portfolio is now well-positioned to capitalise on the broad-based equity market rally, and it has re-emerged as one of the top performers in the ELSS category.

With a current portfolio strategy that balances growth and value, HTSF continues to focus on high-conviction stocks offering a margin of safety.

HTSF's volatility is one of the lowest in its category, significantly below that of the benchmark. However, the fund has delivered appealing risk-adjusted returns, reflected by its respectable Sharpe ratio and Sortino ratio, which are among the best in the category and higher than the benchmark index.

HTSF has outshined its benchmark and many of its peers during bullish market phases and limited the losses during the bear market phases. HTSF has consistently demonstrated its ability to deliver solid returns across complete market cycles, making it a dependable choice for long-term investors.

Like other ELSS, HTSF has the flexibility to invest without any market cap or sector bias or restrictions. Accordingly, it aims to create a diversified portfolio spread across major sectors and market capitalisation that offers an acceptable risk-reward balance.

Table 5A and 5B: Fund Snapshot - HDFC ELSS Tax Saver Fund

Portfolio data as of November 30, 2024.

Portfolio data as of November 30, 2024.

Returns and NAV data as of December 9, 2024.

The securities quoted are for illustration only and are not recommendatory.

(Source: ACE MF, data collated by PersonalFN)

HTSF primarily maintains a large-cap-focused portfolio. It emphasises on companies having strong management with an ability to capitalise on opportunities while managing risks. HTSF also considers the track record of corporate governance, ESG sensitivity, and transparency.

HTSF usually holds about 40 to 50 stocks spread across market caps and sectors. At present the fund has 49 stocks in its portfolio, with top 10 stocks accounting for 57.5%.

HTSF aims to be fully invested in equities at all times. The fund's cash allocation is usually well within the 10% mark. This has helped HTSF to benefit from the rallies in the Indian equity market. Note, due to its high-conviction, value-oriented approach, HTSF may face short- to medium-term underperformance, especially when its core holdings are out of favour or during market rallies driven by momentum. But its fundamentally strong portfolio makes it well poised to create wealth for investors over the long term by managing the risk well.

HTSF has been managed by Ms Roshi Jain, since July 2022. Roshi is a Senior Vice President - Equity investments at HDFC AMC and has a collective work experience of over 17 years in equity research and fund management. Her qualifications include CA, CFA, and PGDM (IIM A).

ELSS (Tax Saving Mutual Fund) for 2025 #3 - Bank of India ELSS Tax Saver Fund

Bank of India ELSS Tax Saver Fund (BETSF) was launched in February 2009. It has proved to be a dynamic scheme in the ELSS category with its appealing returns across time frames. Since inception, the fund has clocked a CAGR of around 20.5% (as of December 9, 2024).

Although the BETSF has exposed investors to above-average risk than its peers, it has fared decently well -- in line with the category average -- on a risk-adjusted basis reflected by the Sharpe Ratio and Sortino Ratio. The fund's sizeable exposure to mid and smallcap stocks has led to more volatility compared to the benchmark and category average.

BETSF aims to identify stocks without any sector or market cap bias and has a preference for high-potential stocks having sustainable business models.

The fund adopts a top-down approach and decides the allocation based on the investment environment, valuation parameters, and other investment criteria.

BETSF's strategy of actively seeking opportunities across various market caps and sectors has proven beneficial, especially during the current bull market.

Table 6A and 6B: Fund Snapshot - Bank of India ELSS Tax Saver Fund

Portfolio data as of November 30, 2024.

Portfolio data as of November 30, 2024.

Returns and NAV data as of December 9, 2024.

The securities quoted are for illustration only and are not recommendatory.

(Source: ACE MF, data collated by PersonalFN)

As per the latest portfolio as of November 2024, BETSF holds 49.5% in largecaps and 42.8% in midcap and smallcap stocks for its equity portion. Currently, BETSF has 65 stocks in its portfolio with the top 10 accounting for 29.7%, making the portfolio well diversified. The sector allocation reveals that BETSF has good exposure to banking & finance, capital goods, Information Technology (IT), auto & auto ancillaries, and healthcare as its top 5 sectors.

With such portfolio characteristics, the fund manager has effectively managed to keep volatility at a reasonable level while delivering solid returns. The risk-adjusted returns are at par with the category average and better than the benchmark index.

BETSF has been managed by Mr Alok Singh since April 2022. Alok is the Chief Investment Officer (CIO) at Bank of India Investment Managers. He has over 2 decades of experience in fund management. He is a CFA and PGDBA from ICFAI Business School.

Best ELSS (Tax Saving Mutual Fund) for 2025 #4 - Parag Parikh ELSS Tax Saver Fund

Incepted in July 2019, the Parag Parikh Tax Saver Fund (PPTSF) is one of the youngest schemes in the ELSS category. It is a rising star in the ELSS category in India, as it has built an impressive track record securing its place among the top performers in its segment.

It builds a diversified portfolio of large, mid, and small-sized Indian companies across multiple sectors and industries. It follows a value-driven approach that focuses on high-conviction and quality stocks. It avoids going with short-term momentum or speculative trends.

Moreover, the fund's focus on Environmental, Social, and Governance (ESG) factors adds an extra layer of prudence, appealing to investors who prioritise responsible investing. PPTSF adopts the bottom-up approach to investing.

By adhering to a disciplined buy-and-hold strategy, PPTSF seeks to unlock the full value of its high-conviction investments over time.

With this approach to investing, since its inception, PPTSF has clocked a CAGR of around 24.8% (as of December 9, 2024).

The fund has clocked appealing returns across time periods by managing the risk exceptionally well (as denoted by the Standard Deviation). The risk-adjusted return of PPTSF as reflected by the Sharpe Ratio and Sortino Ratio is almost parallel to the top performers in the ELSS category and outperformed the benchmark index.

During challenging phases like the 2020 market crash, PPTSF effectively mitigated downside risks, standing out as one of the best performers in the category. In the ongoing bull market, it continues to generate substantial alpha, positioning itself among the top quartile of the ELSS category. This highlights PPTSF's ability to perform well in both bullish and bearish market conditions.

Table 7A and 7B: Fund Snapshot - Parag Parikh ELSS Tax Saver Fund

Portfolio data as of November 30, 2024.

Portfolio data as of November 30, 2024.

Returns and NAV data as of December 9, 2024.

The securities quoted are for illustration only and are not recommendatory.

(Source: ACE MF, data collated by PersonalFN)

PPTSF usually holds a compact portfolio of 30-35 stocks. As of November 2024, the fund has 32 stocks in its portfolio, with the top 10 comprising 58.2% of the portfolio.

PPTSF's portfolio is diversified across 11 sectors and has a well-balanced allocation across cyclical and defensive sectors. As regards top 5 sector exposure, PPTSF has stocks from banking & finance, IT, auto & auto ancillaries, power and mining. The top 5 sectors collectively account for 60% of its assets.

Currently, the PPTSF is holding nearly 10% each in cash & cash equivalents and money market instruments (mainly Certificate of Deposits and Treasury bills).

PPTSF is managed by Mr Rajeev Thakkar and Mr Rukun Tarachandani, while Mr Raunak Onkar is the dedicated fund manager for the foreign investment component. The debt portion of the Scheme is managed by Mr Raj Mehta.

Mr Rajeev Thakkar is the Chief Investment Officer and Equity Fund Manager at PPFAS Asset Management Pvt. Ltd. He has rich experience of around 29 years, working in areas like Investment Banking, managing fixed income portfolios, broking operations, PMS operations, and Fund management. He is a commerce graduate B. Com. (from Bombay University), Chartered Accountant, CFA Charter Holder, and Grad ICWA. He has been managing PPTSF since its inception in July 2019.

Mr Rukun Tarachandani has around 10 years of experience in the equity markets. Rukun's qualification includes an MBA (Finance), B.Tech (Information Technology), CFA Charterholder, and CQF (Certificate in Quantitative Finance) holder. Rukun has been managing this scheme since May 2022.

Mr Raunak Onkar, the dedicated fund manager for overseas investments at the AMC, has around 12 years of experience in the capital markets. He is a science graduate with a specialisation in IT (B.Sc - IT) and has a Masters degree in Management Studies with a specialisation in Finance (MMS - Finance).

Mr Raj Mehta, the fund manager for the debt portion of PPTSF has collectively over 11 years of experience in investment research. He holds a Masters degree in Commerce (M.Com), is a Chartered Accountant and has passed CFA level III. He has been managing the debt component of PPTSF since its inception in July 2019.

This completes our list of the 4 best ELSS (Tax Saving Mutual Funds) for 2025.

Make sure you have the appetite for high risk and an investment time horizon of at least 3 to 5 years when investing in ELSS for tax-saving purposes.

By investing in the best ELSS, you can potentially multiply their wealth and accomplish the envisioned financial goals.

Keep in mind that the gain made at the time of redemption (post the 3-year lock-in period) from ELSS or Tax Saving Mutual Funds will be subject to Long Term Capital Gain (LTCG) tax @12.5%, as applicable for all equity mutual funds.

Invest sensibly; be a thoughtful investor.

Happy Investing!

Related links:

3 Best Large Cap Funds for 2025 - Top Performing Bluechip Mutual Funds in India

3 Best Large & Midcap Funds for 2025 – Top Performing Large & Midcap Mutual Funds in India

3 Best Flexi Cap Funds for 2025 – Top Performing Flexi Cap Mutual Funds in India

The Ultimate Guide to the Best SIP Plans for 2025

3 Best Liquid Funds for 2025 – Top Liquid Mutual Funds for 2025

3 Best Medium to Long Duration Debt Funds for 2025

3 Best Dynamic Bond Funds for 2025M

Note: This write-up is for information purposes and does not constitute any kind of investment advice or a recommendation to Buy / Hold / Sell a fund. Returns mentioned herein are in no way a guarantee or promise of future returns. Mutual Fund Investments are subject to market risks, read all scheme-related documents carefully before investing.

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.