How To Add Nominee in Mutual Funds

Rounaq Neroy

Jun 18, 2024 / Reading Time: Approx. 6 mins

Listen to How To Add Nominee in Mutual Funds

00:00

00:00

The capital market regulator, SEBI in its latest circular dated June 10, 2024, has clarified that non-submission of 'choice of nomination' shall not result in the freezing of demat accounts as well as mutual fund folios.

This surely has facilitated ease of doing investments and done away with the freezing of demat accounts and mutual fund folios of existing investors who haven't made a nomination.

For all new investors/unitholders, the SEBI circular has made it clear that they shall be required to mandatorily provide the 'Choice of Nomination' for demat accounts and/or mutual Folios (except for jointly held demat accounts and mutual fund folios).

'Choice of nomination' means you, the unitholder/investor either explicitly opt-in or opt-out of nomination. In case you decide to opt out for now for some reason, a declaration to this effect needs to be submitted in the prescribed format) before June 30, 2024.

[Read: What Happens If Your Demat Account and Mutual Fund Folios Do Not Have Nominations]

To ensure the smooth transmission of your financial and physical assets to your loved ones, it's in your interest to opt-in for nomination. In this piece, I'll particularly elucidate the process of adding nominees to your mutual fund investments.

How to Add Nominee in Mutual Funds?

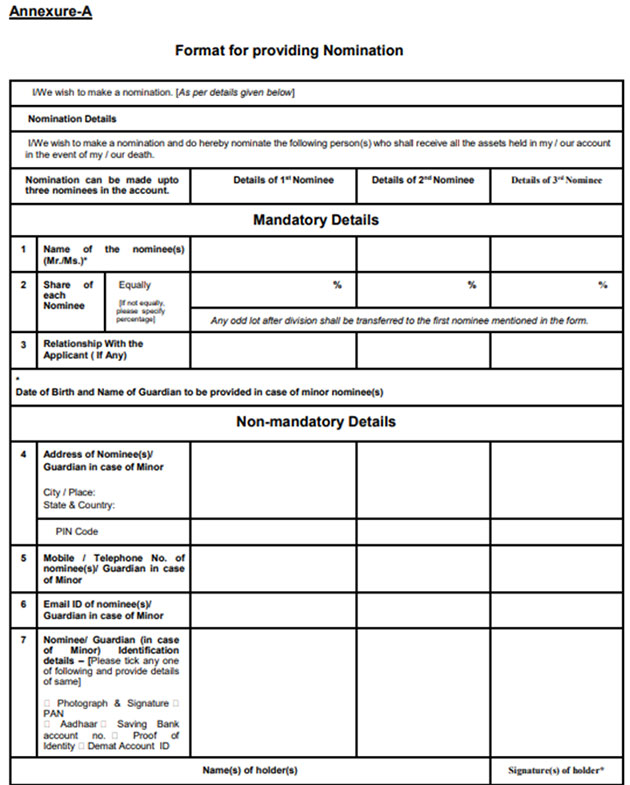

The capital market regulator, in 'Annexure A' of its last circular dated June 10, 2024, has prescribed the format for providing nominations.

You can add multiple nominees for your mutual fund investments, but subject to a maximum of three into one account or folio.

All you have to do is, mention the name of the nominees, their relationship with you (the applicant), and the share of each nominee in the nomination form (as prescribed in Annexure A of the circular dated June 10, 2024). If their share in the nomination is not mentioned, it will be considered equal. These are the mandatory details.

Some of the non-mandatory details are the address of the nominee(s) or guardian in case the nominees are minor, the contact details (mobile/telephone number of the nominee(s) or guardian if the nominee is a minor, address proof and photo id of the nominee(s) or guardian as the case may be.

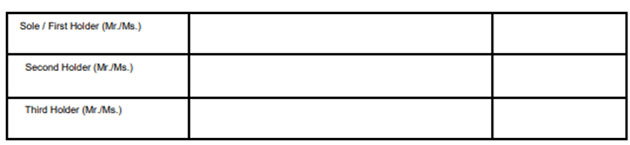

Annexure A (nomination form) is required to be signed by the unit holder (with a handwritten signature). In case the units are held jointly, all joint holders need to sign the nomination form, irrespective of the mode of operation of the account (i.e., whether by 'anyone or survivor' or 'jointly').

(Source: SEBI Circular, dated June 10, 2024)

(Source: SEBI Circular, dated June 10, 2024)

Now, in case the accountholder is unable to sign and affix a thumb impression, then note that the signature of the witness along with his/her name and address will also be required.

The nominee can be added to your mutual fund investment (and demat account) at the time of initial purchase or subsequently.

The nominee can be added by:

-

- Logging into the website of the respective mutual fund house - and therein the investor section with your credentials and mutual fund folio;

-

- Logging into the 'investor services' section of the portal of the mutual fund RTAs, such as CAMS and KFintech or www.mfcentral.com (a centralised platform created by CAMS and KFintech);

-

- Logging into the NSDL website or CDSL website;

-

- Or you could submit a physical copy of the nomination form at the RTA's nearby office, the respective mutual fund houses, or your mutual fund distributor/broker.

Note that in case mutual fund units are held in the demat account, the nomination made with the depository participant becomes applicable.

Here Are Some Ground Rules for Nomination...

Nomination can be made only by individuals in favour of individuals (including minors), central government, state government, a local authority, or any person designated by virtue of his/her office or religious or charitable trust.

Even Non-Resident Indians (NRIs), subject to the exchange control rules in force from time to time, can be a nominee.

However, a Power of Attorney Holder (PoA) and a guardian investing in mutual fund units on behalf of a minor cannot nominate.

Similarly, Hindu Undivided Families (HUFs), body corporates, companies, partnership firms, societies, and trusts (except religious and charitable trusts), cannot make nominations.

Also, the nominee cannot be a HUF, body corporate, company, partnership firm, society, or trust (except a religious and charitable trust).

Can Nomination in Mutual Funds Be Changed?

Yes, nominations once made can be changed subsequently at any time and multiple times.

The cancellation of nomination can be made only by those individuals, i.e. accountholders who hold units and who made the original nomination. The new nomination made shall supersede any prior nomination made by you, the accountholder(s). This applies even to subsequent changes made in the nomination of the demat account.

Does Nominees Acquire Any Title or Beneficial Interest Due to Nomination?

No, the nominee may not necessarily acquire any title or beneficial interest in the property by virtue of this nomination.

The nominee(s) shall receive the units only as an agent and trustee for the legal heirs or legatees as the case may be.

The rights in the units would vest in the nominee(s) only upon the death of the unitholder (in the case of sole holding) and all unitholders (in the case of joint holdings).

Also keep in mind that if the nominee passes away during the lifetime of the investor, the legal heir/s or legal representative/s of such deceased nominee, are not entitled to any right, title or any interest in the financial assets of the investor upon the investor's death solely by nomination.

The Benefits of Nomination

Opting in for nomination for mutual funds, demat and other financial plus physical assets secures the financial future of your loved ones. It also avoids legal hassles for them later after you pass away.

Watch this video to learn about the benefits of nomination:

It is recommended that you opt-in for a nomination for your investments. It shall reduce the legal complexities for your heirs or loved ones, safeguard their financial future, provide you, the accountholder/investor peace of mind, and prevent unclaimed assets or unintended distribution of your assets.

[Read: How to Go About Transmission of Mutual Fund Units In the Event of Death]

Be a thoughtful investor and add a nominee to all your investments today.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. Registration granted by SEBI, Membership of BASL and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.

Disclaimer: This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and use such independent advisors as he believes necessary.