Considering Buying Gold This Gudi Padwa? Here’s Why It's an Opportune Time

Rounaq Neroy

Mar 21, 2023 / Reading Time: Approx. 11 mins

Listen to Considering Buying Gold This Gudi Padwa? Here’s Why It's an Opportune Time

00:00

00:00

Are you considering investing in gold on the auspicious occasion of Gudi Padwa? Yes, then this article will provide a sharp insight if that would be a worthwhile decision.

A few weeks ago, the U.S. Federal Reserve Chair, Jerome Powell, signalled that the interest rates are "likely to be higher" against the backdrop of sticky elevated inflation. The market participants quickly inferred that the terminal rate could go up as high as 5.75%-6.00%, upsetting economic growth. Bond yields, as a result, also inched up on the possibility of future rate hikes. Nonetheless, fortunately, the annual headline inflation rate in the U.S. slowed to 6% in February of 2023 ---the lowest since September 2021 ---in line with the market expectations, which led to yields softening once again.

That being said, the failure of two banks -- Signature Bank and Silicon Valley Bank (a California-based bank popular among the start-ups) -- almost one after the other on account of asset-liability mismatch and large withdrawals (after it stated that it needed to raise money), triggered fears of a banking crisis. It evoked the memories of the global financial crisis of 2007-08 (considered to be a serious one since the Great Depression of 1929) and sent flutters worldwide.

Credit Suisse, Switzerland's second-largest bank and considered to be systemically important globally but clattered with frauds and scandals, also ran into a confidence crisis after it announced a "material weakness" in its 2021 and 2022 financial reporting process. The bank had closed the year 2022 with a loss of nearly USD 8 billion, its biggest since the global financial crisis. Credit Suisse, as a result of such adverse financial results and announcements, faced withdrawals close to USD 10 billion in a week. Later, the Saudi National Bank -- Credit Suisse's biggest financial backer -- made it clear in the public domain that it would not provide any more support, i.e. lend, to the Swiss lender.

Eventually, UBS, Switzerland's largest bank (and a long-time challenger to Credit Suisse) sought the opportunity and bought Credit Suisse by paying around USD 3.2 billion (or 3 billion Swiss Francs) in a historic deal orchestrated by the Swiss National Bank (the banking regulator of Switzerland). On this, Switzerland's finance minister, Karin Keller-Sutte, expressed to the media that this was the best possible solution (a buyout of Credit Suisse with the support of the Swiss government, and not a bailout) and that the bankruptcy of a globally important bank would have created irreparable consequences for financial markets.

But the undulations of the banking crisis have already spread worldwide, making depositors and investors nervous. Depending on the cross-border transaction exposure, the problems of asset-liability mismatches of more banks may come to light.

For now, the U.S. Federal Reserve and other central banks (namely, Bank of England, European Central Bank, Swiss National Bank, Bank of Japan, and Bank of Canada) have decided to carry out a joint liquidity operation (through the standing USD swap line arrangements). This according to them would ensure enough liquidity persists, which shall help reduce the strain and meet the credit demand of businesses and households.

What about the risk to banks in India?

The Reserve Bank of India (RBI) is keeping a close watch on the situation. As far as banks in India are concerned, thanks to the prudent regulations of the RBI -- be it the Capital Adequacy Ratio, Statutory Liquidity Ratio, Cash Reserve Ratio, etc. -- that most banks in India are financially healthy.

The RBI's latest Financial Stability Report released in December 2022, states that the net Non-Performing Assets (NPAs) to Net Advances Ratio fell to 1.3% in September 2022--the lowest in 10 years. The remarkable improvement in their asset quality has abetted the profitability of most banks. A considerable improvement has been recorded by Public Sector Banks (PSBs) according to RBI's report. And a stress test conducted by RBI shows that even without capital infusion, banks are fully capable of absorbing macroeconomic shocks.

(Image source: freepik.com; photo courtesy @xb100)

(Image source: freepik.com; photo courtesy @xb100)

The impact of the banking crisis on gold...

Against the backdrop of the Silicon Valley Bank, Signature Bank, and Credit Suisse fiasco, in my view, gold is likely to turn bolder or exhibit its lustre. Given that liquidity conditions need to be kept comfortable, central banks may abstain from raising interest policy rates aggressively and take respite in the fact that headline inflation has somewhat eased.

Notwithstanding, given that the headline inflation is still elevated and above the target range of most central banks, it would bode well for gold.

Graph 1: Inflation scenarios and gold returns

(Source: World Gold Council)

(Source: World Gold Council)

Usually, when inflation is over 6.00%, gold has fared better than most other asset classes shows a World Gold Council (WGC) study. This year in 2023, with chances of stagflation (a period of slowing economic growth, high unemployment and elevated inflation) and a weaker greenback (as a function of repricing of risk), I foresee gold to fare well.

If the world economy witnesses a significant slowdown or slips into a recession ( which is a widespread and protracted downturn in economic activity), against the backdrop of the banking crisis or any other reason, gold would get all the attention (while other assets such as equities and debt could come under pressure).

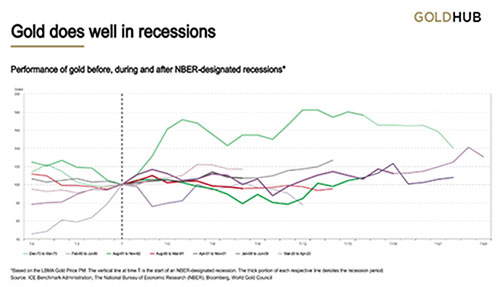

Graph 2: Performance of gold during recessions

(Source: World Gold Council)

(Source: World Gold Council)

Graph 3 above shows that recessions have usually been favourable for gold. In five out of the seven last recessions, gold has delivered positive returns reveals the WGC study.

Graph 3: Bond markets are seeing a recession ahead

(Source: World Gold Council)

(Source: World Gold Council)

The 10-year-less 3-month yield spread inverted in December 2022. If this continues the chances of a recession are higher. If we see a severe downside with stagflation witnessed in 2023, the WGC Outlook 2023 states that gold may have significant upside potential.

In case of a mild recession (i.e., a scenario where inflation halves, the USD weakens, bond yields move slightly higher, China contributes to growth, geopolitical tensions remain, etc.) gold would remain stable with some upside potential.

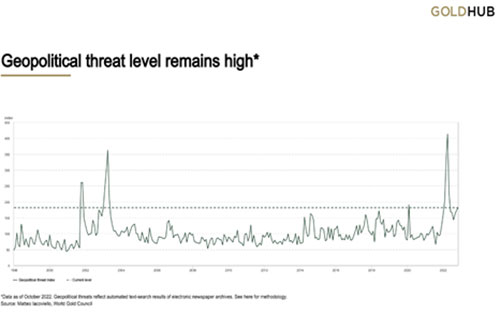

Correspondingly, there are geopolitical tensions in the air...

Graph 4: Geopolitical Threat Index

(Source: World Gold Council)

(Source: World Gold Council)

It's been more than a year since Russia invaded Ukraine, and it doesn't seem to be ending soon. On the contrary, Russia has increased its attack on Ukraine. After the International Criminal Court (ICC) announced that it issued an arrest warrant against Russian President, Vladimir Putin, for war crimes and accused him of personal responsibility, several drone strikes were carried out overnight in several regions of Ukraine.

[Read: 5 Tips to Shield Your Investments Amidst Russia-Ukraine War]

Similarly, North Korea has escalated aggression against the U.S. launching many missile attacks and called for nuclear readiness against the U.S., passing on a message to the navy drill between the U.S. and South Korea.

China-Taiwan relations aren't good, and there are fresh tensions between the two. China also is intimidating India with its build-up and troops entering the disputed areas near the Line of Actual Control (LAC). Currently, the situation along the LAC is "very fragile" and "quite dangerous" in terms of military build-up, observed India's External Affairs Minister, Mr. S. Jaishankar speaking to the media.

India also continues to deal with infiltration from Pakistan at the Line of Control (LOC). In the Middle East and North African (MENA) region as well, there are conflicts.

According to the WGC, if geopolitical tensions flare up, it could lend support to gold investment, as we saw in Q1'22. The current resilience shown by gold in 2022 can be largely attributed to the geopolitical risk (and now the macroeconomic uncertainty) premium, observes the WGC.

How are central banks approaching gold?

Assessing the current situation and the fall out of it on the financial markets and the economy, central banks aren't taking any chances.

Graph 5: The year 2022 gold holdings (in %) of central banks

(Source: World Gold Council)

(Source: World Gold Council)

As a part of the reserve management where gold plays an important role, many central banks are adding gold and holding significant gold reserves.

How should you, as an investor, approach gold?

Approach gold strategically by allocating around 15-20% of your entire investment portfolio to gold ETFs and/or gold savings funds and hold it with a long-term investment horizon (of over 5 to 10 years) by assuming moderately high risk.

In times of macroeconomic uncertainty when equity as an asset class is likely to remain volatile, gold would serve to be an effective portfolio diversifier. Gold is likely to display its trait of being a safe haven and a hedge.

Graph 6: Gold - an effective portfolio diversifier

*Data as of March 17, 2023

*Data as of March 17, 2023

MCX spot price of gold used.

(Source: MCX, ACE MF, PersonalFN Research)

As seen in the graph above, gold has remained relatively firm (clocked +6.4% absolute returns on a YTD basis, as of March 17, 2022), while equities have dipped (generated negative returns thus far), and debt has yielded around +6.00% returns amid a rising interest rate scenario. Very soon gold would make new high and cross Rs 60,000 per 10 grams mark.

Graph 7: Gold has displayed its lustre in the long-term

*Data as of March 17, 2023

*Data as of March 17, 2023

MCX spot price of gold used.

(Source: MCX, ACE MF, PersonalFN Research)

The long-term secular uptrend gold has exhibited cannot be ignored and highlights the importance of owning gold. In the last decade, gold has clocked a CAGR of nearly 7.1% as of March 17, 2027. Going forward too, gold is likely to display its lustre.

So, if you are considering buying gold on Gudi Padwa -- the first day of this 'Chaitra' month that is recognised as the New Year in the Hindu lunar calendar -- go ahead; it would be a wise investment decision.

Happy Investing!

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.