Here's Why NPS Subscribers Partially Withdraw their Retirement Savings

Rounaq Neroy

Jun 14, 2023 / Reading Time: Approx. 5 mins

Listen to Here's Why NPS Subscribers Partially Withdraw their Retirement Savings

00:00

00:00

In my earlier piece, I explained how PFRDA, plans to introduce the 'Systematic Lumpsum Withdrawal (SLW)' Option by the end of this quarter making withdrawals flexible for the National Pension System or NPS subscribers. Today, let's see how NPS subscribers have been withdrawing from their accounts thus far.

At present, 60% of the accumulated corpus can be withdrawn in a lump sum by the subscriber at the age of 60 years, and this withdrawal is tax-free. The remaining 40% component is required to be used to purchase an annuity.

But in between, i.e., after joining the NPS, a subscriber can partially withdraw after 10 years not exceeding 25% of the contributions made to the Tier I account by him/her and excluding contributions made by the employer, if any, subject to the terms and conditions, purpose, frequency and limits as specified by the PFRDA for partial withdrawals.

In the last few years, the PFRDA statistics reveal a rising trend in partial withdrawal requests and such applications being processed, particularly after the COVID-19 pandemic.

Table: Number of Partial Withdrawal Cases Reported and Settled

| Year |

No. of partial withdrawal requests received |

No. of partial withdrawal requests processed |

| 2016-17 |

1,213 |

640 |

| 2017-18 |

6,421 |

3,537 |

| 2018-19 |

22,313 |

15,573 |

| 2019-20 |

35,500 |

28,106 |

| 2020-21 |

62,497 |

45,990 |

| 2021-22 |

146,292 |

131,556 |

| 2022-23 |

532,234 |

486,555 |

(Source: Handbook of National Pension System Statistics 2023)

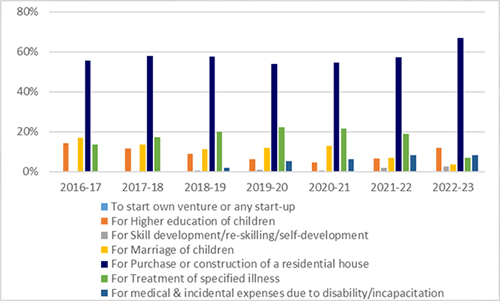

A majority of the partial withdrawal cases have been for the purchase or construction of a residential house, and more so after the COVID-19 pandemic that underscored the need for bigger apartments. Other than that, the demand for housing from nuclear families, which comprise nearly 60% of the total households.

Graph: Reasons for Partial Withdrawals from NPS Account

(Source: Handbook of National Pension System Statistics 2023, data collated by PersonalFN Research)

(Source: Handbook of National Pension System Statistics 2023, data collated by PersonalFN Research)

Similarly, treatment of specified diseases and medical & incidental expenses due to disability or incapacitation has been other reasons for partial withdrawal from NPS. Also, to address higher children's higher education needs and wedding expenses are the key reasons.

(Image source: freepik.com; Image by wirestock on Freepik)

(Image source: freepik.com; Image by wirestock on Freepik)

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Words of wisdom:

Indeed, buying a house and a child's future needs are important financial goals, but by devising a financial plan to address this goal separately and being thoughtful at an early age, the need to withdraw from the retirement kitty would never arise. For medical emergencies or any other exigencies, it is better to have a contingency fund (also known as a rainy-day fund) by keeping around 12 to 18 months of regular monthly expenses in a separate savings account and/or Liquid Funds.

As far as possible, avoid partial withdrawals from the NPS account, even though such withdrawals are tax-free.

Consider the fact that partial withdrawals could imperil the idea of building a respectable corpus for retirement and living the golden years in bliss.

Note that government-backed NPS offering market-linked returns is a meaningful tax-efficient avenue to make systematic investments (with calculated risks) for your retirement --which is an inescapable truth of life and an important financial goal.

How much pension you will receive, depends on the retirement corpus accumulated over the years and the annuity purchased.

Happy Investing!

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

Disclaimer: This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.