How You Can Use the NPS Calculator to Determine Your Retirement Corpus

Mitali Dhoke

Jan 21, 2025 / Reading Time: Approx. 10 mins

Listen to How You Can Use the NPS Calculator to Determine Your Retirement Corpus

00:00

00:00

Planning for retirement is one of the most crucial financial goals in life, yet it is often overlooked until later stages. Imagine stepping into retirement with a sense of complete financial security, knowing you have built a corpus that ensures a steady income for the rest of your life. Sounds like a dream, right?

The National Pension System (NPS) has emerged as a reliable option to build a substantial corpus for your golden years. Introduced by the Government of India, NPS is a low-cost, tax-efficient retirement savings scheme that caters to the financial needs of individuals after retirement. With market-linked returns and flexibility, NPS has emerged as a popular choice among Indian investors.

To make the most of this scheme, the NPS calculator is an invaluable tool that provides clear insights into your potential retirement savings. In this article, we will explore the key features of NPS, how to build a corpus, and how to effectively use the NPS calculator for retirement planning.

[Read: Retirement Planning 101: Key Strategies for a Comfortable Retirement]

Contributions made regularly during your working years, combined with the power of compounding, can lead to significant growth, ensuring a comfortable and worry-free retirement. To help individuals plan their retirement effectively, tools like the NPS Calculator provide clarity on how much you need to invest, the estimated corpus you can accumulate, and the potential pension income you can expect.

Understanding the National Pension System (NPS)

The National Pension System is a government-backed voluntary retirement savings scheme designed to provide financial security to individuals post-retirement. The Pension Fund Regulatory and Development Authority (PFRDA) regulates and administers NPS under the PFRDA Act, 2013.

NPS is mandatory for Central Government employees who joined service on or after January 01, 2004. Whereas NPS voluntary model is available to all the citizens of India including those residing abroad, between the age of 18 and 70 years.

Here are the key features of NPS:

-

Flexibility: NPS allows individuals to decide their contributions based on their financial capacity and goals. Contributions can be made monthly, quarterly, or annually. It offers the flexibility to invest in a mix of equity, corporate bonds, and government securities, offering you control over your asset allocation.

-

Tax Benefits: Contributions to NPS qualify for tax deductions under Section 80C and Section 80CCD(1B) of the Income Tax Act, making it an attractive option for tax-saving purposes. Individuals can avail themselves of tax deductions of up to Rs 1.5 lakh and an additional Rs 50,000, respectively, making NPS a tax-friendly investment.

-

Low Cost: With low fund management charges, NPS ensures that more of your money is invested for growth.

-

Market-linked Growth: NPS investments benefit from market-linked returns, potentially delivering higher growth compared to traditional fixed-income instruments. Professional pension fund managers manage investments in NPS and offer market-linked returns.

-

Annuity Purchase and Withdrawal: At maturity, you can withdraw up to 60% of the corpus as a lump sum, while the remaining 40% is used to purchase an annuity, ensuring a regular income stream post-retirement. NPS permits partial withdrawals for specific purposes such as children's education, medical emergencies, or purchasing a house.

These features make NPS an ideal choice for building a retirement corpus that can sustain you financially during your golden years.

[Read: Which Pension Plan Suits You Best? UPS vs. NPS - Explained]

How NPS Helps Build a Retirement Corpus

Building a retirement corpus involves disciplined contributions, effective asset allocation, and leveraging the power of compounding. Here's how NPS facilitates this process:

-

Regular Contributions: The foundation of a retirement corpus is systematic contributions. With NPS, you can contribute as little as Rs 500 per month, ensuring accessibility for all income groups.

-

Compounding Growth: NPS investments grow through compounding, where returns generated are reinvested, leading to exponential growth over time.

-

Strategic Asset Allocation: Depending on your risk appetite, you can allocate funds across equities, bonds, and government securities, optimising your portfolio's growth.

-

Long Investment Horizon: With an extended investment period until the age of 60 or beyond, NPS allows sufficient time for wealth accumulation.

The power of compounding plays a pivotal role in building a substantial retirement corpus through NPS. By starting early and contributing regularly, individuals can accumulate a significant amount by the time they retire.

For instance, Mr Ramesh is 30 years old and has a retirement age of 60 years, which allows an investment horizon of 30 years. Let us assume the expected rate of return is 8% p.a.

Calculation: Using an NPS Calculator, Ramesh's total contributions over 30 years will be:Rs 5,000 × 12 months × 30 years = Rs 18,00,000

At an expected annual return of 8%, the power of compounding will grow his corpus to approximately Rs 74.4 lakh by the age of 60.

Upon retirement, Ramesh opts to use 40% of his corpus for an annuity plan (a mandatory NPS rule). This leaves him with:

Assuming an annuity rate of 6%, Ramesh will receive a monthly pension of Rs 14,900 in addition to his lump sum withdrawal.

Why This Works:

-

Regular monthly contributions ensure consistent growth

-

Returns are reinvested, exponentially increasing the corpus over time

-

Contributions and withdrawals are tax-efficient, maximising savings

By starting early and leveraging the flexibility of NPS, Ramesh successfully builds a substantial corpus, securing his financial future. This highlights how NPS can be a reliable partner in achieving long-term retirement goals.

By leveraging these features, individuals can systematically build a substantial corpus to meet their post-retirement financial needs.

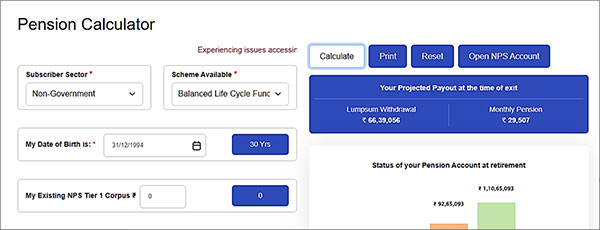

What Is the NPS Calculator?

The NPS calculator is an online tool designed to estimate the maturity corpus and pension amount based on your input. Offered by the NPS Trust, it simplifies the complex calculations associated with retirement planning. By using the calculator, you can:

-

Visualise your retirement savings growth

-

Determine the monthly pension amount based on your annuity selection

-

Plan your contributions to achieve a target corpus

The calculator factors in key variables such as your age, contribution amount, investment duration, and expected returns to provide accurate estimates, making it a critical component of retirement planning.

(Source: Pension Calculator NPS)

(Source: Pension Calculator NPS)

How to Use the NPS Calculator

Using the NPS calculator is straightforward. Below is a step-by-step guide to help you determine your retirement corpus:

Step 1: Access the NPS Calculator

Visit the official NPS Trust website at npstrust.org.in and navigate to the NPS calculator.

Step 2: Enter Personal Details

Provide the following details:

-

Current Age: Your age will determine the investment horizon until retirement

-

Retirement Age: The default retirement age is 60, but you can extend it to 75

Step 3: Specify Contribution Details

Input your expected monthly or annual contribution. Ensure the amount aligns with your financial capacity and retirement goals.

Step 4: Choose Investment Return

Select the expected annual return on your investments. The calculator offers options based on historical returns for equity, bonds, and government securities.

Step 5: Annuity Options

Decide the percentage of the corpus you want to allocate for purchasing an annuity. The minimum requirement is 40%, but you can choose a higher percentage.

Step 6: Annuity Return Rate

Enter the expected rate of return on the annuity. This determines your monthly pension amount post-retirement.

Step 7: Calculate

Click the 'Calculate' button to view the results. The calculator will display:

Example Scenarios

To illustrate how the NPS calculator works, let's consider three example scenarios:

Scenario 1: Moderate Contributions and Returns

Results:

Scenario 2: Higher Contributions and Returns

Results:

Scenario 3: Lower Contributions with Longer Horizon

Results:

Key Benefits of Using the NPS Calculator

-

The calculator provides a clear roadmap for achieving your retirement goals.

-

Adjusting variables like contributions and returns allows you to experiment with different scenarios.

-

By visualising potential outcomes, you can make informed decisions about asset allocation and contribution levels.

-

Online accessibility ensures you can use the calculator anytime to review and adjust your plan.

To summarise...

The NPS calculator is a powerful tool that simplifies the complexities of retirement planning, helping you estimate your potential corpus and monthly pension with ease. By understanding the key features of NPS and leveraging the calculator's functionalities, you can create a robust financial plan tailored to your retirement goals.

Start early, contribute consistently, and let the NPS work for you, ensuring a financially secure and stress-free retirement.

We are on Telegram! Join thousands of like-minded investors and our editors right now.

MITALI DHOKE is a Research Analyst at PersonalFN. She is an MBA (Finance) and a post-graduate in commerce (M. Com). She focuses primarily on covering articles around mutual funds including NFOs, financial planning and fixed-income products. Mitali holds an overall experience of 4 years in the financial services industry.

She also actively contributes towards content creation for PersonalFN’s social media platforms in the endeavour to educate investors and enhance their financial knowledge.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.