Can Focused Funds Help You Ride the COVID-19 Crisis? Know here…

Listen to Can Focused Funds Help You Ride the COVID-19 Crisis? Know here…

00:00

00:00

Historically, mutual fund houses have launched maximum New Fund Offers (NFOs) in ascending market conditions.

However, now seeing the unwavering participation of investors --- particularly the retail ones in equity-oriented mutual funds (through lump sum and Systematic Investment Plans) --- fund houses are appealing investors with New Fund Offers even amidst the heightened volatility of the Indian equity market and an uncertain macroeconomic environment caused by the COVID-19 pandemic.

[Read: A Spree of New Mutual Funds to Hit the Market Soon. Will They be Worth Considering?]

According to SEBI records, five fund houses have filed draft prospectus so far in June 2020 for launching six schemes in total.

Mahindra Manulife Mutual Fund and HSBC Mutual Fund, in particular, are launching Focused Funds.

(Image source: pixabay.com; photo courtesy - Dmitriy)

(Image source: pixabay.com; photo courtesy - Dmitriy)

Is the atmosphere conducive to launch Focused Funds?

The Securities and Exchange Board of India's mutual fund categorization and rationalization norms, mandate a Focused Fund to invest at least 65% of its total asset in equity & equity related instruments of up to 30 companies.

Moreover, a Focused Fund needs to state where it intends to focus, -- whether large-cap, mid-cap, small-cap or multi-cap. That said, most focused funds follow a multi-cap approach with a large-cap bias.

Focused Funds expose investors to concentration risk. If the conviction bets taken by the fund manager go wrong, investors suffer a loss (although the broader investment objective is to seek long term capital growth through investments in a concentrated portfolio of equity & equity related instruments). There is no assurance that the investment objective of the Scheme will be achieved.

In 2019 as Indian equities clocked +14% absolute returns, Focused Funds grabbed the attention of investors with many of them posting double-digit returns.

But in the year 2020 wealth creation through equities has posed a challenge with the outbreak of COVID-19.

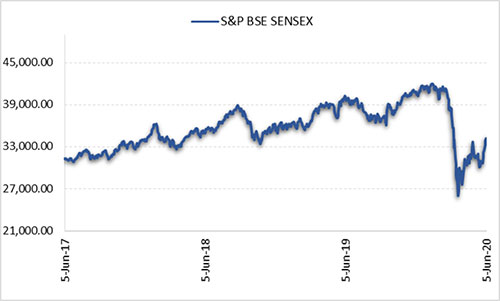

Graph 1: S&P BSE Sensex on a rollercoaster

Data as of June 5, 2020

Data as of June 5, 2020

(Source: ACE MF, PersonalFN Research)

On a year-to-date basis, Indian equities have eroded investor' -- lost -17% (as of June 10, 2020). Likewise, even the mid-cap and small-cap indices have plummeted, nearly -15% and -13%, respectively.

It is only in the last three months that the markets have recovered (around +35% since March lows) hoping that we shall overcome the COVID-19 crisis --as efforts currently are on to develop an effective COVID-19 vaccine, plus the government and RBI are doing the best they can. That said, there are challenges in play and therefore the fight between the bulls and bears continues.

[Read: How Should a Novice Approach Mutual Funds amidst COVID-19]

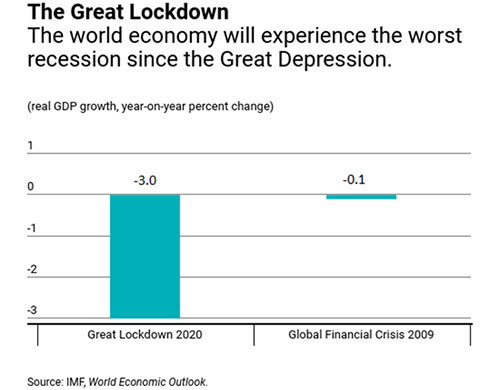

The impact of extended lockdown is expected to severe on the Indian economy.

Graph 2: The impact of COVID-19

(Source: International Monetary Fund Blog)

(Source: International Monetary Fund Blog)

Even though policymakers are providing support, there is substantial uncertainty about its impact on people's lives and livelihood, observes the International Monetary Fund (IMF). We could see the worst global recession - worse than the Global Financial Crisis of 2008 and the Great Depression of the 1930s - warns the IMF.

The international rating agencies such as Moody's, Standard & Poor, Fitch; also have all pencilled a contraction in India's GDP growth for the current fiscal year (but expect a strong rebound next fiscal year if all goes well).

Global rating agency Moody's has slashed India's credit rating from 'Baa2' to 'Baa3', maintaining a negative outlook. This rating downgrade is in view of:

-

- Policymaking institutions facing a challenge in enacting and implementing policies which can effectively mitigate the risk of a sustained period of relatively low growth;

-

- Significant further deterioration in the government's fiscal position; and

-

- Stress in the financial sector.

While the government has taken steps to unlock in phases (Unlock 1.0) from the COVID-19 lockdown (assessing the situation and taking adequate precautions) and restart the economic activity, the numbers of COVID-19 cases continue to rise. People are not following social distancing norms, not that they do not want to but the density of population and lack of civic sense makes it difficult. And speaking of the healthcare system, it is crumbling (India's healthcare spend is just 3.6% of GDP).

The business environment has turned bad to worse. Many companies as a cost rationalisation move, announced pay cuts, job cuts, and/or are deferred salaries. Now, although some companies have begun operations, the guidelines to be followed make it easier said than done for organisations to conduct business normally -- particularly for the ones operating in the red zone and depending on contract workers and migrant labours. With the transport system not entirely opened up (to contain the spread of the virus) commuting is an issue, and 'work from home' is unfeasible and impractical for certain functions of a business organisation.

In my view, it would certainly not be easy to bring back high growth soon -- not at least in the fiscal year 2020-21. For complete normalcy to return post-COVID-19 crisis, it will take quite a while -- maybe a couple of years -- and provided we do not see another wave of Coronavirus or any other catastrophic event. Until then the Indian equity market may not show any decisive trend and will be on a rollercoaster.

The Q4FY20 corporate earnings results haven't been encouraging -- in fact, worse than 6 years ago when the Modi-led-NDA government was elected to power. The earnings data for Q1FY21 and for the ensuing few quarters could be under noticeable strain for most companies amidst the COVID-19 crisis, travel bans, and muted demand. Smaller companies are likely to be more vulnerable due to the unprecedented situation that we are facing today. Highly leveraged companies are likely to find it difficult to service their loans -- considering many of them have halted their operation or are functioning at an extremely sub-optimal level.

Managements of several companies are anyways hinting at a decline in revenue and net profits. If India Inc. quarterly earnings do not sustain or plummet, more instances of corporate governance lapses come to light; it could upset the Indian equity markets and may weigh on the performance of the equity-oriented mutual funds subject to their portfolio characteristics.

Under such market circumstances should you invest in Focused Funds?

"We are already seeing high-quality businesses in the global context, showing recovery. There is no reason why some of the risk-taking investors should not participate in this recovery. High-quality stocks are likely to lead the recovery initially. Further, it makes sense for an investor to build a portfolio with high-quality stocks available at attractive valuations." - Mr Ashutosh Bishnoi, MD & CEO of Mahindra Manulife Mutual Fund speaking to the Economic Times.

In my view, the risk will be very high. If the conviction bets of the fund manager go wrong, a loss will be inevitable.

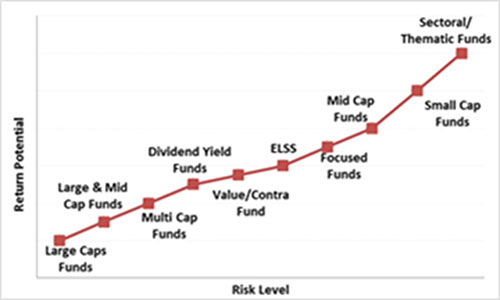

Graph 3: Placement of Focused Funds on the risk-return spectrum

Note: For illustrative purpose only

Note: For illustrative purpose only

(Source: PersonalFN Research)

On the risk-return spectrum, a Focused Fund is placed just a couple of notches below small-cap and mid-cap funds.

Hence, only if you have the stomach for very high risk and an investment time horizon of at least 5 years, you may consider a Focused Fund.

How has the track record of Focused Funds been?

So far Focussed Funds category which has 22 schemes and asset base of Rs 44,866 crore (as of April 30, 2020) has displayed a fairly consistent performance across time frames (see Table below) primarily because of the large-cap orientation of most of the schemes.

Barring a few schemes, focused funds have been largely betting big only on well-established companies and avoiding less researched and illiquid companies. Simply put, fund houses have preferred to take focused exposure in large-cap stocks having relatively stable business models and strong balance sheets, including some index heavy companies.

Table: Report card of Focused Funds

The list above is not exhaustive

Data as of June 5, 2020

Point-to-point returns considered.

(Source: ACE MF, PersonalFN Research)

Five schemes that have done well over the last five years account for 44% of the AUM base. Not only have they managed to do better than their benchmark indices but also outperformed the category average returns noticeably across longer timeframes. The performance across market phases (bulls, bears, and correctives) of focused funds also been satisfactory so far across the last three market cycles. In the present corrective phase, certain schemes have done reasonably well.

However, the current heightened volatility of the market poses a risk for Focused Funds. Certain schemes haven't seen the intense volatility as we are experiencing today, and during the global financial crisis and/or at the time dotcom bubble burst.

The current downturn in markets and businesses is unprecedented. It's been tough for even the most experienced fund managers to assess what is forthcoming. The future is extremely uncertain. How many businesses will survive out this challenging phase is tough to foretell.

Final verdict...

Investing in a Focused Fund with no or poor track record isn't warranted at this juncture. If you are an aggressive investor and want to invest in Focused Funds, restrict yourself only to scheme/s with proven track records across timeframes and market phases.

If you wish to select worthy equity mutual fund schemes, I recommend you to subscribe to PersonalFN's unbiased premium research service, FundSelect. As a bonus, you also get access to PersonalFN's popular debt mutual fund service, DebtSelect.

At PersonalFN, we arrive at top-rated funds using our SMART Score Model.

So, each fund recommended by PersonalFN goes through our stringent process involving both quantitative and qualitative parameters before providing you with Buy, Hold and Sell recommendations on equity and debt mutual fund schemes.

If you are serious about investing in rewarding mutual fund schemes, Subscribe now!

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds