How to Navigate Your Mutual Funds in Rising Interest Rates

Mitali Dhoke

Jun 10, 2022

Listen to How to Navigate Your Mutual Funds in Rising Interest Rates

00:00

00:00

Inflation across the globe is rising, and it has become challenging for policymakers as they deal with slow economic growth and rising prices. In response to control the rising inflation, central banks around the world may raise interest rates.

After ignoring inflation for a long time and shrugging it off as a temporary phenomenon, the US Fed Reserve had to bite the bullet. In May 2022, the US Federal Reserve announced its biggest interest rate hike over two decades to control the rising prices. It lifted the interest rate by half a percentage point, to a range of 0.75% to 1%.

Even in India, after a long spell of low-interest rates, in an off-cycle move, on May 04, 2022, the RBI announced a 40 bps increase in the benchmark repo rate to 4.40% and a 50 bps hike in the Cash Reserve Ratio (or CRR). The RBI raised the repo rate (the key rate that determines the direction of interest rates in the economy) at the unscheduled policy meeting, marking its first change in the rate in two years and its first rate hike in nearly four years.

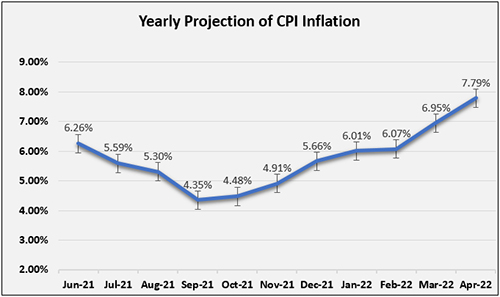

India's Consumer price index-based headline inflation rose further from 6.95% in March 2022 to 7.79% in April 2022, reflecting a broad-based increase in all its major constituents, and remains above the RBI's tolerance band of 6% for the fourth month in a row. Geopolitical spillovers and the rise in crude oil prices have sparked a rise in inflationary momentum that we cannot afford. Inflation will continue to rise as long as the geopolitical turmoil and retaliatory activities continue.

Graph 1: India's Inflation rate (past 1-year data)

(Source: Ministry of Statistics and Programme Implementation)

(Source: Ministry of Statistics and Programme Implementation)

Since the MPC's meeting in May 2022, the global economy has been grappling with multi-decadal high inflation and slowing growth, ongoing geopolitical tensions and sanctions, rising crude oil and other commodity prices, and lingering COVID-19-related supply chain constraints. Global financial markets have been roiled by turbulence amidst growing stagflation concerns, leading to a tightening of global liquidity and risks to the growth outlook and financial stability.

Considering all these factors and the assumption of a normal monsoon in 2022 with an average crude oil price (Indian basket) of US$ 105 per barrel, the RBI has now projected CPI inflation to be at 6.7% in 2022-23 (with Q1 at 7.5%; Q2 at 7.4%; Q3 at 6.2%; and Q4 at 5.8%, with risks evenly balanced. These projections make it clear that CPI inflation is expected to be above the tolerance level of 6% through the first three quarters of 2022-23. According to the MPC, persistent inflationary pressures could trigger second-round impacts on headline CPI.

Given the high level of uncertainty around the inflation trajectory, targeted monetary policy action is required to keep inflation expectations anchored and price pressures from expanding. According to the RBI Governor, the Indian economy is resilient, and the central bank's actions would be measured and focused on lowering inflation to the target level.

As the inflation beast continues to bite into economic growth, the Monetary Policy Committee (MPC), at its meeting held on June 8, 2022, decided to increase the policy repo rate under the liquidity adjustment facility (LAF) by 50 basis points to 4.90% with immediate effect. Further, the MPC decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

These decisions are in accordance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4% within a band of +/- 2% while supporting growth.

However, market participants must keep in mind that these changes in interest rates will affect your mutual fund investments, and you need to navigate your mutual funds wisely to reduce its impact on your portfolio.

The RBI has not given any indication on the extent to which it will raise rates going ahead. The magnitude and pace of increases will be driven by movements in global commodity prices and domestic inflation prints over the next few months. Most market participants believe that RBI will implement substantial hikes in order to control inflation, which raises concerns about their investments.

(Image Source: www.freepik.com)

(Image Source: www.freepik.com)

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds

Impact on your Equity Mutual Funds

The equity market started the new financial year on a sluggish note. Due to weak domestic and global indications, the S&P BSE Sensex declined by 2.6% (or 1,508 points) in April 2022. Many investors are worried about their equity mutual fund investments due to the uncertainty around the quantum of a rate hike by RBI. Inflation that is spiralling out of control is another important driver of increased market volatility.

As interest rates rise, banks hike lending rates, raising the cost of borrowing for businesses. Companies that borrow a lot of money will be stressed since their loans will have a higher interest rate and large companies with very low debt are likely to fare well in such circumstances. It indicates that your large-cap mutual funds will likely perform better in the near future.

Keep in mind that equity as an asset class, particularly through equity-oriented mutual funds, has the potential to generate long-term wealth. The wealth-building potential of equities has been demonstrated by the historical returns created over the last several decades.

As equity markets, by their very trait, will continue to display volatility, investors must recognise that SIPs are an effective means of long-term goal planning. During a correction phase, more units would be allocated to your SIP instalment, and when the market begins to rise again, it would compound your wealth and possibly help you achieve your financial goals.

If you've been SIP-ping into the best and most suitable equity mutual funds, don't make the mistake of pausing or discontinuing your SIPs because of short-term market volatility. It could put brakes on the power of compounding.

If your investment objective is capital appreciation, clock inflation-beating returns, with a long term-approach, diversified equity mutual funds are a suitable avenue. However, the equities are expected to remain highly volatile in the near term, given the headwinds in play. For the time being, reduce your return expectations from equity mutual funds if you are an equity investor.

You might want to think about devising a strategy and staggering your equities exposure. Even if you opt for SIP in mutual funds, remember that it is crucial to select schemes prudently. Due to its purpose to tactically capture opportunities across market capitalisation, multi-cap funds or Flexi-cap funds are a prudent way to diversify across market capitalisation. At the same time, keeping a component of your equity allocation in large-cap funds ensures portfolio stability, and mid-cap funds generate higher returns by assuming very high risk.

Impact on your Debt Mutual Funds

Debt Mutual Funds invest in fixed income securities like corporate or government bonds and money market instruments. These interest-bearing products pay investors a predetermined rate of interest (coupon rate) at regular intervals and return the principal invested at maturity. Interest rate changes have a direct impact on the prices of these securities.

Debt Mutual Funds that invest in short-term securities benefit when interest rates increase. Funds that invest in the short maturity segment witness minimal mark to market impact when interest rates rise. On the other hand, funds focusing on longer duration instruments that have an average maturity typically in a range of 5 to 10 years are highly vulnerable to interest rate risk. These funds could witness high volatility in the near term.

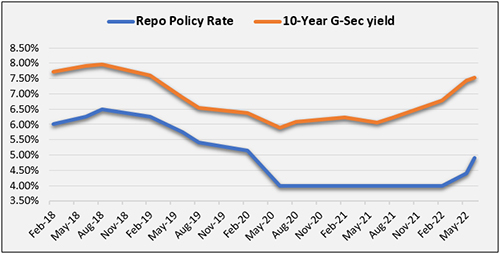

The start of the rate hike cycle, inflationary pressure (particularly oil prices), falling Rupee, higher government borrowings, a worrying debt-to-GDP ratio, and the uncertainties due to the Russia-Ukraine war kept the yields elevated. The 10-year bond yield, which had been slowly climbing in recent months, crossed the 7.5% mark in June 2022, following the RBI's announcement of a rate hike.

Graph 2: The 10-year benchmark yield

(Source: Investing.com, PersonalFN Research)

(Source: Investing.com, PersonalFN Research)

Bond prices and interest rates are inversely proportional, and a rise in yield has a negative influence on bond prices, resulting in a loss of value for investors. As a result, the net asset value (NAV) of debt mutual funds, particularly those with long durations, falls. When bond yields have increased in the past, debt funds in these long-duration categories have fared poorly.

Given the current rising interest rate environment, Debt Mutual Fund investors may choose to stick to short-term debt funds, which have the least amount of mark-to-market impact when rates climb. Please remember that these short-term funds may experience short-term volatility, but they will recover over time.

If you have to park fresh money in debt funds, keep on the shorter side of the duration curve by investing in Liquid Funds, Ultra Short Duration Funds, Low Duration Funds, etc. The lower residual maturity helps the fund follow an accrual strategy where it can earn from coupon payments and roll over the assets on maturity.

What should investors do amidst the rising interest rate?

These macroeconomic elements that affect the market are impossible to control; as investors, all you can do is try to minimise their impact on your investment portfolio. When it comes to mutual funds, however, one thing investors should never do is try to time the market. Rising interest rates will have an influence both on equity and debt markets. Rather than getting caught up in the hype or short-term blips, investors should concentrate on their long-term goals of the market.

Equities are well-known for providing significant gains in the long run. Maintain adequate diversification and ideal asset allocation to weather the storm amidst the period of high inflation and rising interest rates. On the debt side, in increasing interest rate scenarios, you'll get a better return by investing in debt funds that hold bonds with shorter maturities. Remember, you should always be mindful of the credit risk the debt funds carry.

The recent spike in volatility in equity and bond markets has been unsettling for many investors. Remember, markets are cyclical by nature, and periods of strong performance would tend to be followed by periods of under or low performance. Investor needs to focus on their goals, stick to their asset allocation plan, and avoid making decisions driven by short-term trends. Ensure to continue with your investments in a worthy mutual fund scheme and that your SIPs are not discontinued due to a short-term slump in the market.

As a result, to mitigate the effects of the RBI's Repo Rate hike, you should be prudent and wisely navigate your mutual funds in diversified asset classes, as per your suitability based on risk profile, investment horizon, and objectives.

PS: If you wish to select actively managed worthy mutual fund schemes, I recommend that you subscribe to PersonalFN's unbiased premium research service, FundSelect.

As a bonus, you get access to PersonalFN's popular debt mutual fund service, DebtSelect.

PersonalFN recommendations go through our stringent process that assesses both quantitative and qualitative parameters, providing you with Buy, Hold, and Sell recommendations on equity and debt mutual fund schemes. Read here for more details...

If you are serious about investing in rewarding mutual fund schemes, Subscribe now!

Warm Regards,

Mitali Dhoke

Jr. Research Analyst