Why You Need To Be Extra Careful While Selecting Debt Mutual Funds Now

Listen to Why You Need To Be Extra Careful While Selecting Debt Mutual Funds Now

00:00

00:00

In recent times, the Indian mutual fund investors got the rudest shock when Franklin Templeton discontinued six of its debt schemes abruptly. While many mutual fund houses claimed that the crisis was largely a function of an unprecedented credit environment and lack of adroitness in containing risk at the scheme level, it was certainly not an unforeseen event if you look at the history of mishaps in the debt fund category.

Certain debt fund managers have been engaging in yield hunting to clock a higher rate of return and lure investors. However, this activity does attract very high risk as well. Ideally, debt schemes should aim to strike a balance between risk and return and not turn a blind eye to the obvious credit risk (in the race to garner Assets Under Management (AUM).

Amidst COVID-19 pandemic, going is likely to get even tougher for debt funds. Here's why...

Recently, the Reserve Bank of India (RBI) Governor, Mr Shakitikanta Das in his address at the State Bank of India (SBI) Banking & Economic Conclave, asked banks and Non-Banking Financial Companies (NBFCs) to conduct a COVID-19 related stress test and raise capital.

"The lockdown and anticipated post-lockdown compression in economic growth may result in higher non-performing assets (NPAs) and capital erosion of banks," he said.

Expressing caution he articulated, "Minimum capital requirements of banks, which are calibrated based on historical loss events, may no longer be considered sufficient enough to absorb the losses. Meeting the minimum capital requirement is necessary, but not a sufficient condition for financial stability."

Banks and NBFCs were advised to evaluate the impact of COVID-19 on the key areas of business such as liquidity, capital adequacy, asset quality, and profitability among others. As a key takeaway, the RBI Governor asked them to focus more on governance, risk management, and raising asset quality, while expecting NPAs to rise.

Why have banks come under the weather?

(Source: freepik.com; photo created by ijeab)

COVID-19 has altered the landscape of India's credit markets completely. Credit risk has amplified. Extension of moratorium serves only temporary relief. Likewise, loan recasts do not push NPAs down; it just defers the NPA recognition.

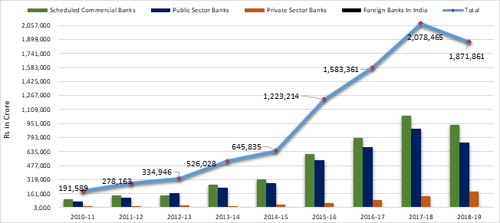

Graph: COVID-19 to send the asset quality in disarray

As per the data available up to Financial Year 2018-19.

(Data source: RBI)

"The uncertainty on the asset quality of banks remains high with almost 30-40 per cent of loan book across various banks under moratorium announced by the Reserve bank of India (RBI)," said rating agency ICRA (a Moody's Investors Service Company) in a statement.

According to ICRA, the gross NPAs of banks are likely to rise to 11.3-11.6% by March 2021. The lockdown has impacted the debt servicing ability of borrowers, the rating agency observes. And with provisioning, the profitability of banks will be adversely impacted.

Similarly, S&P Global Ratings, an international rating agency, expects the gross NPAs to skyrocket to a two-decade high of 14% in the fiscal year 2020-21 (from 8.5% in the previous fiscal year) due to operational outages and recession caused by the coronavirus.

"The Covid-19 pandemic may set back the recovery of India's banking sector by years, which could hit credit flows and, ultimately, the economy," the agency said. Further, the rating agency is of the view that loan recast will only defer NPA recognition and not solve it.

By the same token, India Ratings and Research (Ind-Ra) has said that due to the impact of COVID-19 and associated policy response, the NPAs from top-500 debt-heavy private sector companies could result in an additional Rs 1,67,000 crore. This over and above Rs 2,54,000 anticipated before the onset of the pandemic, thus the taking the quantum of NPAs to Rs 4,21,000 crore. "Given that 11.57% of the outstanding debt is already stressed, the proportion of stressed debt is likely to increase to 18.21% of the outstanding quantum," stated Ind-Ra.

These forecasts arrive at a time when India's economic growth is expected to contract (around 4-5%) in the current fiscal year and a financial crisis brews for several corporates (and individuals).

NBFCs, Housing Finance Companies (HFCs), private sector banks, among others are likely to bear the brunt of the deteriorating credit environment. Similarly, many other sectors such as airlines, hotels, travel & tourism, entertainment, retail, consumer durable, automobile manufacturers and component makers, real estate companies, engineering companies, among others whose balance sheets are highly leveraged are likely to feel the pinch. Thus, coping with debt servicing may be a big challenge.

While the Atmanirbhar stimulus package has opened the credit tap with loans to different sectors and sections of the society, there is risk-aversion that has set in because the money tap is running thin (or dry) amidst the COVID-19 outages and restrictions.

Needless to say, India is likely to see a muted credit growth in FY21. CRISIL has forecasted just 1% credit growth in FY21.

What does this mean for your debt mutual funds?

Debt mutual funds hold a variety of debt papers---across issuers, maturity profile, and ratings. An amplified credit risk environment heightens the risk of investing in certain sub-categories of debt mutual fund schemes. The ones that have compromised on the portfolio characteristics to chase yields may encounter a rude awakening. The low-rated debt papers will face a higher chance of a rating downgrade, and if this indeed materializes then the instances of side-pocketing may go up.

That being said, the capital market regulator has laid down an Operational Framework for the transaction of defaulted debt securities, allowing mutual funds to sell debt papers that have defaulted to distressed funds. Earlier, the stock exchanges suspend trading and reporting of trades on debt securities before the redemption date. However, with effect from July 1, 2020, the restrictions on transactions in such debt securities can be lifted within two days of intimation of the default from the issuer or debenture trustee. The securities have to mandatorily disclose that there was a default in payment of debt obligations.

What should investors in debt mutual funds do?

First, do not assume that short-term credit instruments are safer than long term instruments. That's not always the case.

At present, many debt mutual funds across maturity profiles are grappling with downgraded, toxic debt papers, heightening the investment risk. Hence, make no mistake to approach debt mutual funds looking at just the brand value.

Keep your eyes wide open and watch out for rating downgrades. In the present market condition, even certain short-term bonds could be subject to rating downgrades. Plus, steer clear from Credit Risk Funds.

In my view, given that the COVID-19 pandemic has a far-reaching impact across sectors and industries, analysing the portfolio characteristic of debt mutual funds comprehensively is imperative.

Considering that most of the rally at the longer end of the yield curve has already come about since the time RBI started reducing policy rates, the longer end of the yield curve, thus, could prove less rewarding and riskier (may encounter high volatility) in the foreseeable future.

You'll be better off investing in shorter duration debt funds. But when you do so, keep in mind that it would be imprudent to invest in debt mutual fund schemes whose underlying portfolios are compromised with low rated papers of private issuers.

To select a scheme, essentially assess your risk appetite and investment time horizon, plus factors such as:

-

✓ The portfolio traits and sectoral allocations

-

✓ Maturity profile

-

✓ AUM and the expense ratio of the scheme

-

✓ Returns and risk ratios

-

✓ Interest rate cycle

-

✓ Track record of the fund house and processes and systems followed by it

At present, for an investment time horizon of less than 1 year, it would be better to go with only a pure Liquid Funds that do not have exposure to private issuers and/or Overnight Fund.

Our friends at Quantum Mutual Fund have highlighted the secret behind their debt management strategy, which has helped them provide safety and liquidity to investors who invest in Quantum funds. Don't Worry, Quantum Liquid Fund always aims for Safety and Liquidity.

For an investment time horizon of over a year, you may consider only such funds that own a minimum of 80% in Government of India or PSU debt papers (as an option to a Corporate Bond Fund). For example, Banking & PSU Debt Funds hold 85 to 90% of its assets in instruments issued by major Banks and PSUs

It is time to distance yourself from other debt funds, particularly those holding a predominant portion in debt papers issued by private issuers and low-rated instruments in the hunt for higher yield.

Remember, investing in debt funds is not risk-free.

Alternatively, if you prefer to keep your capital safe, opt for bank fixed deposits.

To sum-up...

It's time that debt fund managers also conduct a stress-test to lessen the impact of a potential downgrade. However, it remains to be seen if debt fund managers will conduct that stress test to strengthen risk management and in the larger interest of investors.

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

PS: If you wish to select worthy mutual fund schemes, I recommend that you subscribe to PersonalFN's unbiased premium research service, FundSelect.

Additionally, as a bonus, you get access to PersonalFN's popular debt mutual fund service, DebtSelect.

Each fund recommended under FundSelect goes through our stringent process, where they are tested on both quantitative as well as qualitative parameters.

Every month, PersonalFN's FundSelect service will provide you with insightful and practical guidance on equity mutual funds and debt schemes - the ones to Buy, Hold, or Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds