When the PMC Bank crisis came to light, the RBI imposed restriction on the bank and there were limits on the amount that could be withdrawn by the depositors. As a result, the depositors of the bank were under immense stress.

The bank had not disclosed a high exposure loan to HDIL, which is a violation of RBI norms. People were concerned that the bank may go under liquidation and they would lose their hard-earned money.

Shockingly, the PMC Bank was considered one of the leading cooperative banks. The fallout at this well-established bank left depositors of other banks wondering if their bank was safe enough or could it meet a similar fate.

[Read: Should You Park Your Hard-Earned Money in Co-operative Banks?]

Bank deposits are a preferred choice of investment for many individuals despite the low interest rates they offer; mainly because many prefer safety of principal over returns. Thus, the number of deposits with banks continues to rise year after year. But while the deposits have increased, the level of insured deposits as a percentage of assessable deposits has declined from a high of 75% in FY 1982 to 28% in FY 2018.

Currently, the Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the RBI, insures deposits up to Rs 1 lakh of deposit holders across accounts in case a bank goes under liquidation. It must be noted that the amount was last revised in the year 1993 from the earlier Rs 30,000. Keeping in mind the inflation, this amount has outlived its shelf life and therefore, there is a need to hike this insured amount.

Another key reason why DICGC needs to consider revamping the deposit insurance is to protect depositors in current times when the bank frauds are rising and many banks are dealing with high NPAs.

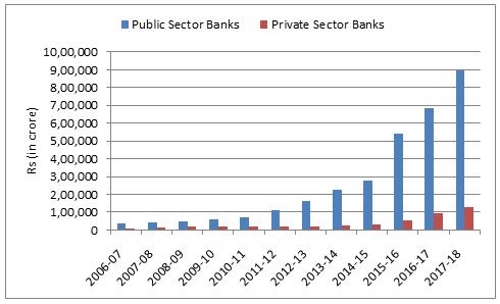

As per the RBI provisional data released by the press information bureau, as on March 31, 2019, the aggregate amount of gross NPAs of PSBs and Scheduled Commercial Banks (SCBs) were Rs 8,06,412 crore and Rs 9,49,279 crore, respectively.

Graph: Gross NPAs of Banks

As per the data available up to Financial Year 2017-18.

(Data source: RBI publications)

The press release states that the NPAs have declined as a result of the Government's 4R strategy of recognition, resolution, recapitalisation, and reforms.

However, the write-offs have increased instead of a reduction in NPAs due to recoveries. Additionally, the bank provisions have gone up, signalling deterioration in asset quality.

Besides, the loan mela which was recently introduced by the finance minister to give a boost to the MSME sector and increase credit outreach may add to the NPA worry. Given the poor state of MSMEs, there is a high risk of these loans turning into NPAs, especially for Public Sector Banks (PSBs). Private Banks have better credit appraisal system and are therefore, likely to be less affected.

[Read: Read This If You Hold Deposits With Public Sector Banks]

The RBI, in its Annual Report 2018-19 also states that incidents of bank frauds have risen by 15% on a year-on-year basis in FY19. India witnessed over 6,800 cases of frauds worth Rs 71,543 crore, mostly relating to cheating and forgery. PSBs accounted for the majority of the frauds.

Banking frauds and the NPA mess do not reveal a very healthy and virtuous picture for the investors, and therefore, the credit risk is very much evident. The safety of depositors, most of whom park their life savings in banks, must therefore be a top priority. Increasing deposit insurance is a vital step in this regard.

As per media reports, the DICGC has started the process to revamp the archaic deposit insurance scheme. After approvals from the finance ministry and the central bank, the insurance limit may be increased and can be different for individual and institutional depositors. DICGC may also consider giving banks an option to pay a higher premium to insure a larger amount.

The discussion is in its initial stages and a decision will only be taken after consulting all the stakeholders. Meanwhile, as an investor, one should always exercise caution and make prudent investment choices. Make sure to diversify your investment across asset classes to minimise the risk and optimise returns. Invest in schemes that provide transparency and safeguard the investor's interest.

PS: If you're looking for "high investment gains at relatively moderate risk", in current turbulent times, consider 2019 Edition of PersonalFN's Premium Report, "The Strategic Funds Portfolio For 2025"

It is based on the Core and Satellite approach of investing, that will that have the ability to generate lucrative returns over the long term via SIP route.

Subscribe now! to potentially multiply your wealth in the years to come.

Add Comments