"If there must be trouble, let it be in my day so that my child may have peace" - Thomas Paine (Founding Father of United States of America and author of 'Common Sense')

Isn't it what every parent wishes for?

As parents, we encourage our little ones to be ambitious. Their goals today are much bigger than what we dreamt of. And achievement of many of these aspirations requires far more focus, especially on education.

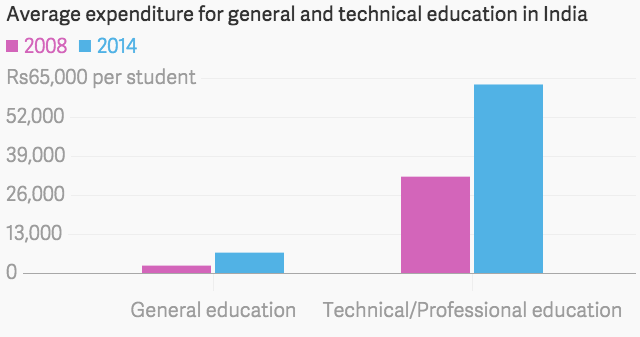

According to the National Sample Survey Office (NSSO) report released in June 2014 the average annual private expenditure for general education (primary level to post graduation and above) has shot up by a staggering 175.82% to Rs 6,788 per student in 2014 from Rs 2,461 in 2007-08

During the same period, the annual cost of professional and technical education went up by 95.69% to Rs 62,841 per student from Rs 32,112 in 2007-08.

(Source: National Sample Survey Office, MOSPI)

(Note: The above image is for illustration purpose only)

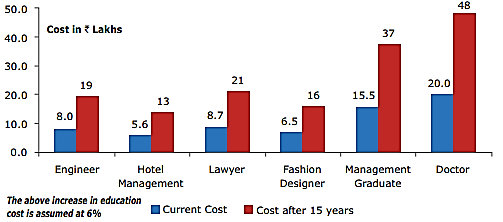

As time passes, the competition will be more severe and dearer. Here's a snapshot on the cost after 15 years at a CAGR of 6% p.a for some of the professional courses.

(Source: Shiksha.com)

(Note: The above image is for illustration purpose only)

Life is full of uncertainties and as responsible parents; we want to ensure our children's needs are always met.

Meeting these ever increasing costs requires financial planning.

One such product is 'Child Plan'. It is an insurance product with an opportunity to invest and save taxes, all at the same time.

Recently, Canara HSBC Oriental Bank of Commerce Life Insurance launched a new Child Plan titled "Smart Junior Plan". It is a non-linked participating savings-cum-protection endowment life insurance plan.

Some of the key benefits of Smart Junior Plan are as follows:

- Enhanced Triple Protection – This benefit gets activated in case of death. On death, the family receives:

- Lump sum benefit

- Waiver of all remaining premiums

- Guaranteed Annual Pay-outs as planned to meet child's education needs

- We have covered this point in detail under Scenario 2 below

- Guaranteed pay-outs for child`s education – Annual pay-outs aligned closely to your child's educational milestones.

- Customization of your investment horizon and key education milestones – Multiple policy term options will ensure that you are able to choose the best suited policy term closely aligned to your child's age and future education milestones.

- Premium payment options – Choice of flexible premium payment terms which can closely align to your savings horizon.

- Smooth build-up of education fund – Addition of regular annual bonuses along with Final bonus (if any), on maturity to ensure that your child's education fund gets built up smoothly.

- Better Value for higher premiums – High sum assured rebate to ensure that you get the extra benefit for making a higher premium commitment for the chosen policy term.

- Tax benefits on premium paid and benefit received during policy term under Section 80C and Section 10(10D), as per the Income Tax Act, 1961, as amended from time to time

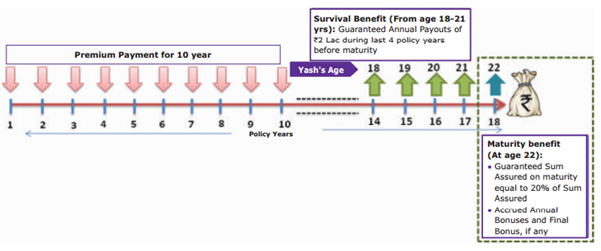

Let us understand the policy with the help of an example:

Yash Gupta is 4 years old His father, Ranjeet is 35. He wants to secure his son's future by investing in Smart Junior Plan. Mr Gupta estimates that he requires a guaranteed benefit of at least Rs 2 Lakh every year for four years when Yash turns 18. He would need a lump sum at age 22 to plan for Yash's higher education/ professional course. He opts for a policy term of 18 years and takes a Sum Assured of Rs 10 Lakh with premium paying term of 10 years. His annual premium is Rs 1,01,400 (before applicable taxes and cess).

Below are two scenarios, illustrating the benefits which will accrue under each of them.

Scenario 1: Survival and Maturity Benefit

Mr Gupta will get a guaranteed pay-out of Rs 2 Lakh every year in the last four policy years before the maturity year. The pay-outs will be made subject to all premiums being paid as and when due. On maturity, Mr Gupta will receive an amount of Rs 2 Lakh as Guaranteed Sum Assured along with accrued annual bonuses and final bonus, if any, as illustrated below.

(Source: www.canarahsbclife.com)

(Note: The above image is for illustration purpose only)

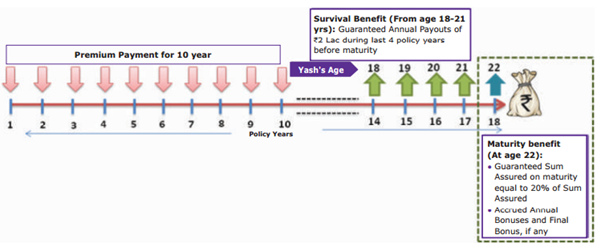

Scenario 2: Death Benefit

Assuming Mr Gupta passes away in the 4th year, after paying the premiums for the first 3 years; his family will receive the following benefits:

- Mr Gupta's family will immediately get a lump sum amount of Rs 10,14,000 which is higher of:

- Sum Assured (i.e. Rs 10 Lakh) or

- 10 times the Annualized Premium (i.e. Rs 1,01,400 x 10 = Rs 10,14,000) or

- 105% of all premiums paid till date of death less underwriting extra premium paid, if any (i.e. Rs 1,01,400 x 3 x 1.05 = Rs 3,19,410)

- In addition, all future premiums, if any, are waived off. Guaranteed Annual Pay-outs of Rs 2 Lakh will be payable as scheduled in the last four policy years before the maturity year. Annual bonuses will continue to accrue for the rest of policy term, as applicable.

- Guaranteed Sum Assured on maturity equal to Rs 2 Lakh along with accrued annual bonuses and the final bonus, if any, will be payable on maturity.

(Source: www.canarahsbclife.com)

(Note: The above image is for illustration purpose only)

To Conclude…

Although the Child Plan seems to be an alluring investment option at the outset; it isn't! In the above example, under scenario 1, the Internal Rate of Return (IRR) or in simple words the yield comes to 3.24% p.a. (after assuming Mr Gupta earns a bonus of Rs 5 Lakh on maturity).

Instead, a well-diversified portfolio of equity mutual funds with an

SIP mode of investing would have fetched far better inflation-adjusted return which would have been tax efficient as well. To address insurance needs, a term insurance plan with an optimal cover could have provided a better cost-to-benefit which would have further saved the outflow in terms of premium paid and facilitated a reasonable contribution to achieve the vital goal of planning for your child's education needs.

Here are 7 steps to plan for your child's education:

- Are you planning local or global education?

- Historical and Current School Fees - An Estimate for Future Inflation

- Always Expect the Unexpected

- Invest Smartly to Build the Corpus

- Remember to Insure Yourself Adequately

- Avoid Pre-Packaged Child Plans from Insurance Companies

- Get Started Right Away

What is your strategy for your child's future? Share your views with us.

Add Comments