In a falling interest rates environment yields drop and bond prices rise. Debt fund investors enjoy double-digit returns in such interest rate phases.

In a falling interest rates environment yields drop and bond prices rise. Debt fund investors enjoy double-digit returns in such interest rate phases.

Exactly this happened between April 2014 and December 2016, when the Reserve Bank of India (RBI) reduced rates by 175 basis point to 6.25% from 8%. It was one of the best periods for long-term debt funds over the past decade.

With the decline in bond yields, long-term debt funds or income funds generated returns in excess of 12% compounded. Over 65 schemes delivered double-digit returns. The set of over 150 debt schemes generated an average return of 10%.

Given the massive returns over this period, do you feel debt funds are safe?

If yes, then consider this – As many as 82 debt mutual fund schemes delivered a return under 4% in the year ended November 27, 2017.

As many as 23 schemes entered the negative territory. Had you invested in debt schemes based on the above past returns, it would have led to a sheer disappointment.

The past one year has been a tumultuous period for long-term debt investments. This period marked the end of a massive rally bond funds enjoyed that started in April 2014.

Is this the end of the bond market rally?

As yields move in a cycle, the exuberance debt schemes enjoyed—thanks to falling interest rates—seems to be over now.

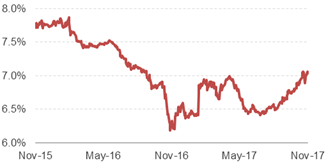

Exactly a year ago, the 10-year Government Security benchmark yield bottomed out to 6.2% as on December 1, 2016. Since then yields have been volatile, but rising. As a result, the valuation of bonds fell, dragging down the NAV of mutual funds invested in these securities.

Currently, the macro environment does not seem very conducive for lower yields.

10-Year G-Sec Benchmark Yield

Data as on November 28, 2017

(Source: RBI, PersonalFN Research)

Demonetisation and the excess liquidity in the system was a major cause of the drop in yields.

After bottoming out to 6.2% a year ago, the 10-year G-Sec benchmark yield spiked in February 2017. Yields declined had considerably on the back of excess liquidity because of demonetisation, but shot-up to as much as 7% when the RBI changed its policy stance from accommodative to neutral at its policy meet in February 2017.

However, as inflation began to ease and economic growth faced a setback, the probability of a rate cut seemed highly likely. Lowering inflation improved the market sentiment and investors went back on a buying spree. The benchmark yield dropped once again to the 6.5% level.

As expected, the RBI cut rate in August 2017. But soon, the declining inflation started to move up on the back of rising crude oil prices, rise in income under the 7th pay commission, and implementation of the Goods and Service Tax (GST). Retail inflation had bottomed out to 1.5% in June 2017 and has been rising since then. Higher inflation reduces the chances of the RBI cutting rates further.

Thus, despite an expected rate cut of 25 basis points by the central bank, yields have inched upwards since then. Steadily, yields peaked to nearly 7% in November 2017. The 7%+ levels were last seen in September 2016.

The sentiments in the Indian debt market are hurt on concerns that the path to fiscal consolidation could be disrupted (owing to mammoth expenditure by Government), especially when growth is flagging and Current Account Deficit on rising imports is widening yet again.

The fiscal deficit data released for the first-six months of the current fiscal year (i.e. April 2017 to September 2017) touched 93.1% of its full-year budgeted estimate (of Rs 5.46 trillion). During the same period of the last fiscal year, the deficit was 83.9% of its full year budgeted estimate (of Rs 5.34 trillion). The increase in Government expenditure is on account of early presentation of the budget and the subsequent front-loading.

Inflation in housing and household goods & services too reported an uptick. The central bank was proved right when it said the awards of 7th CPC and the resultant increase in real wages in the rural and organised sector will send ripples to household goods, healthcare, recreation, clothing, and footwear.

A rating upgrade boosts market sentiments, but not for long

A rating upgrade by Moody’s——a world-renowned credit rating agency——helped cool-off the rising yields. However, this was short-lived, and yields moved back up within a week.

With Moody’s upgrade of India’s rating from “Baa3” to ‘Baa2’ changed the global outlook from ‘stable’ to ‘positive’. In contrast to Moody’s, Standard & Poor’s, another renowned global rating agency, kept its sovereign rating for India unchanged at ‘BBB-minus’. ‘BBB’ rating is a notch above junk status

Unless India successfully deals with tougher issues such as job creation, rising fiscal deficit, and flagging growth, debt markets may continue to be volatile.

Bank interest rates are on a decline

To add insult to injury, over past few months, most major banks cut their Savings Bank interest rates. In some cases, the savings interest that you earn may be as low as 3%-3.5% per annum (p.a.). Interest rates offered by major banks on 1-year fixed deposits, too, have dropped to as low as 6.25%. In such low interest rate regimes, Indian savers are scurrying for better income generating options.

Though debt schemes may look like a better alternative, during such times, selecting the category of debt mutual funds first becomes crucial.

How should you structure your debt fund portfolio?

PersonalFN is of the view that, investing aggressively at the longer end of the yield curve could prove imprudent. To put it simply, investing in long-term debt funds (holding longer maturity debt papers) can be perilous, since already most of the rally has been captured at the longer end of the yield.

In fact, short-term maturity papers are turning attractive and fund houses, too, are aligning their portfolio accordingly. Yet, if you wish to take the risk (hoping a rate cut), invest vide dynamically managed bond funds (with an investment time horizon of over three years). An investment horizon of over three years will give you an additional tax advantage.

Ideally, you will be better off if you deploy your hard-earned money in short-term debt funds; but ensure you’re giving due importance to your investment time horizon, asset allocation, and diversification. Consider investing in short-term debt funds for an investment horizon of 2-3 years.

You may also consider arbitrage schemes for short-term investments.

If you have an investment horizon of 3 to 6 months and up to 2 years, ultra-short term funds (also known as liquid plus funds) would be the most suitable.

And if you have an extreme short-term time horizon (of less than 3 months), you would be better off investing in liquid funds. These funds earn a higher return and are less volatile. Under the instant redemption facility, available for certain liquid schemes, it takes under 30 minutes to transfer the redemption amount to your bank account.

Do not forget that investing in debt funds is not risk-free. Therefore, consider the 5-facets while investing in debt funds.

Prudent investing and financial discipline are vital ingredients to long-term financial well-being.

If you need research-backed recommendations to select the best debt mutual fund schemes for your portfolio, you can access 7 high-performing, time-tested readymade portfolios with a decade-long market-beating track record. PersonalFN’s model mutual fund portfolio service ‘FundSelect Plus’ has completed a decade and we are offering subscriptions at a massive 75% discount!

Apart from four equity-oriented portfolios, you get access to three readymade debt mutual portfolios. The debt portfolios have been formulated using the investment tenure as the cornerstone. Depending on your investment horizon, which could be anywhere from less than 3 months, 3-12 months, or more than 12 months, you can choose the portfolio of your choice.

PersonalFN’s track record speaks for itself, as all three portfolio have comfortably overachieved their respective benchmarks. Don’t miss out on special offers. Subscribe now!

Add Comments