(Image source: Image by Deedster via Pixabay )

(Image source: Image by Deedster via Pixabay )

The committee members of the RBI in its every Monetary Policy review Meeting, since February 2019, have given their nods for successive rate cuts. In total, a 135-basis point cut has been implemented, with an effective repo rate at 5.15%. The move was taken to help revive the slowdown of the economy.

However, in its fifth bi-monthly Monetary Policy Meeting held in the month of December, the RBI didn't propose a rate cut and retained an accommodative stance. It deliberated extensively on the currently evolving macroeconomic and financial conditions, and the outlook.

Based on its considered assessment, the MPC voted unanimously to keep the policy rate unchanged and decided to continue with the accommodative stance, for as long as it is necessary to revive growth while ensuring that inflation remains within the target.

These decisions were in consonance with the objective of achieving the medium-term target for Consumer Price Index (CPI) inflation of 4.0% within a band of +/- 2% while supporting growth.

Table 1: Series of policy rate cuts in 2019 to address growth concerns

| Month |

Repo Policy Rate |

Policy rate cut (Basis points) |

Monetary Policy Stance |

| Feb-19 |

6.25% |

25 |

Neutral |

| Apr-19 |

6.00% |

25 |

Neutral |

| Jun-19 |

5.75% |

25 |

Accommodative |

| Aug-19 |

5.40% |

35 |

Accommodative |

| Oct-19 |

5.15% |

25 |

Accommodative |

| Dec-19 |

5.15% |

Status quo |

Accommodative |

| Total |

|

135 |

|

Data as of December 5, 2019

(Source: RBI)

The committee is of the view that a continuous rate cut would not help in bolstering the economy unless it is effectively transmitted down the line.

In its assessment, the RBI committee noticed the following and mentioned about the future as well:

Reflecting on easy liquidity conditions, the weighted average call rate (WACR) traded below the policy repo rate (on an average) by 8 basis points (bps) in October and by 10 bps in November.

The monetary transmission has been full and reasonably swift across various money market segments and the private corporate bond market. As against the cumulative reduction in the policy repo rate by 135 bps during February-October 2019, transmission to various money and corporate debt market segments ranged from 137 bps (overnight call money market) to 218 bps (3-month CPs of non-banking finance companies). Transmission to the government securities market, however, has been partial at 113 bps (5-year government securities) and 89 bps (10-year government securities). Credit market transmission remains delayed but is picking up. The 1-year median marginal cost of funds-based lending rate (MCLR) has declined by 49 basis points. The weighted average lending rate (WALR) on fresh rupee loans sanctioned by banks declined by 44 basis points, while the WALR on outstanding rupee loans increased by 2 basis points during this period.

However, transmission is expected to improve going forward as (i) the share of base rate loans, interest rates on which have remained sticky, declines; and (ii) MCLR-based floating rate loans, which typically have annual resets, become due for renewal.

After the introduction of the external benchmark system, most banks have linked their lending rates to the policy repo rate of the Reserve Bank. The median term deposit rate has declined by 47 bps during February-November 2019. The weighted average term deposit rate declined by 9 bps in October as against a decline of just 7 bps in eight months during February-September. This augurs well for transmission to lending rates, going forward.

The overall economy had witnessed a liquidity crunch, thereby impacting the consumer sentiment and real GDP growth moderated to 4.5 per cent year-on-year. There was a sharp increase in retail inflation at 4.6 per cent in October, propelled by a surge in food prices.

The banks still seamlessly and effectively are yet to pass it down to retail investors and even to borrowers----'they have remained sticky'----for banks do not want to lose out on deposits.

The banks point out that the interest rates offered by the government on small saving schemes have higher rate than the bank FD rates, and even offer tax benefits, making the real returns much higher, hence making the small saving schemes attractive. And the government has not taken a stand to reduce interest rates on small savings schemes. Or depositors will move funds from bank fixed deposits to these schemes.

Now, the RBI wants the government to reduce interest rates on small savings schemes to be in-line with the rates offered by banks on deposits and loans for effective transmission of the central bank's rate cuts for uplifting the banking sector.

In turn boosting the lending activity, consumption and easing out on liquidity pressure. Banking sector is the biggest lending sector and Fixed Deposits (FDs) remain one of the sought-after investment avenues. FDs earn an assured rate of return, provides safety of capital, highly liquid for short-term needs, and worthy option for contingency needs.

[Read: Factors to Look At While Investing In Bank FDs]

For the July to September quarter, the finance ministry had announced a reduction of the policy rates. Due to the weakening of economic pressure, the finance ministry has been reluctant to reduce rates since then because it holds the view that it offers better returns to senior citizens, who have most of their savings parked in bank FDs. Furthermore, it will help in infusing more funds in the economy and enable the government to avoid market borrowings.

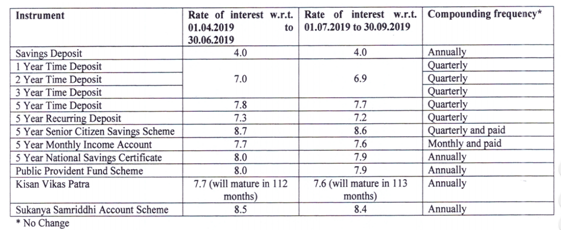

Table 2: Interest rates for small saving schemes

(Source: Department Of Economic Affairs)

(Source: Department Of Economic Affairs)

Every other small saving scheme, including KVP and Sukanya Samriddhi scheme, had been cut by meagre 10 basis point, except the savings deposits.

Graph: How have 10-year G-sec yields pursuant to policy repo rate cuts...

Data as of December 13, 2019

Data as of December 13, 2019

(Source: RBI, PersonalFN Research)

The 10-Year Benchmark Yield in G-Sec slipped from 7.41% on December 12, 2018, to 6.6% on December 12, 2019, within a year. In past few months, the benchmark yields have been down nearly 63 bps YTD on concerns that the fiscal deficit target may be missed.

The finance ministry may reduce rates to match the softening of interest rates in the banking sector with the repo rate cut of RBI, and to reduce the borrowing costs so they are passed on to the consumers to uplift the banking sector.

Add Comments