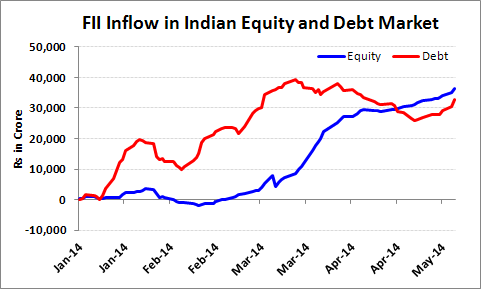

Post-election surveys have predicted that BJP-led NDA may win comfortably. Hopes of getting a stable government pushed Indian equity market indices to new highs. Foreign Institutional Investors (FIIs) have turned bullish towards India, making it one of the best performers among emerging markets. Since the beginning of 2014, FIIs have invested around Rs 36,400 crore in Indian equities. On the other hand, Indian debt was considered to be unattractive until last few days. Yield on 10-year sovereign bond recently crossed 9% mark. But things are changing fast. The inflows in debt have also gone up substantially. In just first half of May 2014, FIIs have bought Indian debts to the tune of around Rs 6,315 crore. As a result, the Yield on 10-year sovereign bond eased to about 8.70%, in spite of creeping inflation. Such conditions might tempt you to speculate on interest rates and yields. However, PersonalFN believes doing so would put your finances at risk. Let's find out why...

India back in demand...

Data as on May 13, 2014

(Source: ACE MF, PersonalFN Research)

Formation of a stable government at the centre would be a definite positive for Indian debt markets. But it wouldn't change the outlook of the Indian debt market, unless fundamental forces turn positive. We first need to look at factors that had made Indian debt unattractive. Those include:

- High inflation

- Unfavourable policy rates

- Huge borrowing by the Indian government

- Poor fiscal management (suggested by high fiscal deficit)

- Possibility of a downgrade on sovereign rating of India

- Political uncertainty

- Relatively attractive yields on the U.S. treasuries

Out of aforementioned factors that affected Indian debt, only last two factors seem to have turned slightly positive for now. Federal Reserve in the U.S. is unlikely to raise interest rates soon. As a result U.S. treasury yields might remain soft.

Many concerns still remain unattended. The next government coming to power may initially deal with number of challenges. The new policies that it formulates may have pleasant or unpleasant impact on the markets. Given that Mr Chidambaram has tried to show an improvement in last fiscal deficit by postponing many subsidies, the new government may need to borrow more in the current financial year. Retail inflation or CPI, at 8.59% in April, has reached a 3-month high. The expected unfavorable monsoon due to El-Nino effect may have inflationary impact on food prices. The RBIs target is to bring CPI to 8% in the current year and 6% by next financial year. High inflation may not let RBI cut policy rates soon. This may keep interest rates high and may continue to impact the capex cycle which is yet to turn positive. Manufacturing growth also remains weak.

So what to expect?

Since RBI follows inflation-targeting approach, it is unlikely that, RBI would lower rates in a hurry. RBI may ignore falling manufacturing growth and weaker performance of the overall economy for now. Unless the new government, irrespective of whoever forms it, takes promising measures to contain fiscal deficit, debt markets would remain vulnerable. Unless retail inflation reduces convincingly, it would be difficult for RBI to reduce policy rates.

Debt investors, including FIIs would closely track policies of the new government. Developments such as introduction of Direct Tax Code (DTC) and Goods and Services Tax (GST) would be positive. Rationalisation of tax structure may help bridge the gap between revenues and expenditure of the government.

As far as the question of containing inflation is concerned, along with government initiatives, factors such as monsoon, international crude oil prices, and movement of rupee would be closely tracked. If FII flows continue to remain robust, RBI may have to buy dollar aggressively to contain upward movement of Rupee. In such a scenario equivalent money would be released in the system. However, this may not add to sudden inflationary pressure as rising rupee may make import of crude oil cheaper; and partial de-regulation of diesel would help pass on the benefit. On the other hand, weak monsoon would push inflation upwards. Having said this, any excess liquidity in the system would add to inflationary pressure. To arrest that RBI may continue with curbs on borrowing. This may keep rates on short maturity instruments in a range with upward bias.

End Note:

Short term debt funds still look more attractive than long term debt funds. PersonalFN is of the view that, instead of speculating on movement of interest rates and yields, you should look at your time horizon before investing in a debt fund. Short term debt funds might be attractive but if your time horizon is just 2 months; they still remain risky for you. Long term debt funds including gilt funds expose you to interest rate risk. Only degree varies. Stable government may change the perception of investors but that to translate into confidence, the ground realities have to change.

This article was originally authored by Personalfn for its partner website Equitymaster.com

Add Comments