A Smart Way to Invest for Your Child’s Higher Education

Ketki Jadhav

Feb 02, 2023 / Reading Time: Approx. 8 mins

Listen to A Smart Way to Invest for Your Child’s Higher Education

00:00

00:00

Parenting brings a lot of happiness but also comes with numerous responsibilities. No parent wants to see their child struggle financially. It is quite natural for parents to want the best for their children - the best education, the best opportunities, etc. To ensure their children's financial stability, many parents start investing in their children's future education from a young age. Regardless of how old your child is, it is never too early or too late to begin investing towards your child's higher education.

"Education is the passport to the future, for tomorrow belongs to those who prepare for it today."

-Malcolm X

Education provides a strong foundation for a child to become self-sufficient, empowered, and achieve success.

However, obtaining quality education comes with a cost. You may already be aware that the cost of quality education in India as well as abroad is very high and is expected to continue rising, considering the education inflation across the globe.

Therefore, it is essential to have a strong financial plan in place to ensure your child gets access to quality education. Starting early in your planning will give you enough time to accumulate sufficient savings to cover your child's higher education expenses.

Many parents are concerned about financing their child's dreams & aspirations and can spend a considerable amount of time & money fretting over their child's future. Hence, saving and investing for a child's higher education is one of the top-most priorities for most parents.

While many parents still rely on traditional saving options, such as bank fixed deposits and endowment policies, these options may not provide adequate returns to keep up with inflation. These instruments can yield returns of around 5% to 7% per annum, and the interest earned is taxable based on the investor's income tax slab, making the post-tax returns almost negligible. Thus, the constantly rising inflation is the primary reason why traditional financial instruments, like fixed deposits, will possibly not create an adequate corpus for your child's higher education.

In the last few years, there has been an increase in new-age parents buying long-term investment plans that primarily focus on building the child's education corpus. Unfortunately, most of these plans are insurance-based that provide insurance coverage as well as generate returns on investments. Such insurance plans are called Unit-linked Insurance Plans (ULIPs), which, similar to mutual funds, further invest the investments collected from policyholders in equity shares, debt instruments, bonds, etc. However, these plans are not ideal for your long-term financial goals like a child's education, as they are high-cost financial instruments that neither generate decent profits nor provide adequate insurance coverage.

Given the rising inflation, low returns from traditional investment instruments, and the high cost of ULIPs, it is imperative to have a well-designed smart financial plan for your child's higher education.

Investing in a carefully selected mix of best-suited mutual funds is an ideal option to build the corpus for your child's higher education. This approach allows you to invest in the most appropriate assets, and a diversified portfolio of well-chosen mutual funds can yield returns that outpace inflation and help you accumulate wealth over the long term.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Know how much amount you need for your child's higher education:

Quality education in India can cost anywhere from Rs 5 lakhs to 30 lakhs, whereas studying abroad can cost a minimum of Rs 25 Lakhs. With an education inflation rate of 11% to 12% per year, it is expected to increase four to six times over the next 15-20 years, meaning that education in India could cost at least Rs 25 to 35 Lakhs and studying abroad could cost a minimum of Rs 1.25 crore.

It is important to estimate the required education corpus based on your child's potential education plans, whether it be in India or abroad and the type of course they choose. The idea of calculating the estimated corpus is not to scare you but to provide a realistic understanding of the cost.

Prepare a financial plan:

After determining the required amount for your child's higher education, it is time to make a financial plan. As discussed, investing in carefully selected mutual funds can help you achieve your objective in the long term. However, it is important to understand the risk-return spectrum of mutual funds. Make it a point that risk and return go hand in hand; for every return you seek, there is a certain level of risk associated with it.

Source: PersonalFN Research

Source: PersonalFN Research

As you see in the above pyramid, Liquid Funds and Gold Funds are at the lower level of the risk-reward spectrum. That means they carry low risk but, at the same time, may fail to generate above-average returns. Whereas Small-cap Funds and Mid-cap Funds are at the high end of the risk-reward spectrum, carrying high risk with a potential to yield inflation-adjusted returns and create wealth in the long term. That said, remember that high risk does not guarantee high returns.

As Benjamin Graham wisely said, "The essence of investment management is the management of risks, not the management of returns."

Hence, instead of investing imprudently, going by just returns, you must be mindful of the risk involved. While risky investment avenues help you create wealth in the long term, conservative investment avenues help you diversify the risk. Therefore, to achieve your goal of a child's education corpus, you should invest in the right mix of different mutual fund schemes based on your risk profile and investment horizon.

Choose the right mutual fund schemes:

Now that you know what your asset allocation should be like, the next step is to choose the best-suited mutual fund schemes for your child's higher education. Understand that selecting the right mutual fund schemes that align with your investment goal involves the analysis of several qualitative, quantitative, and personal factors.

The quantitative parameters typically include the past performance of the scheme and risk-adjusted returns. Whereas qualitative parameters include portfolio quality, fund manager's style & experience, different ratios, investment system and process at the fund house, and assets under management, among others. Apart from these, the personal factors that need to be considered are your risk appetite, investment horizon, and investment objective.

Maintain financial discipline:

Financial discipline is the key to achieving your long-term financial objectives. Investing regularly in a disciplined manner leads to huge investments over a period and you reach your goal within the targeted time.

Financial discipline is a critical factor in meeting your long-term objectives, like a child's higher education. Hence, the Systematic Investment Plan (SIP) route of mutual fund investment is a great option to address your long-term financial goals.

It not only ensures you invest an adequate amount but also instils financial discipline, which is a necessity to invest for an important goal like a child's higher education. With its sheer power of compounding and rupee cost averaging, SIP makes the best choice for the novice as well as seasoned investors to build a corpus steadily and generate inflation-beating returns over time.

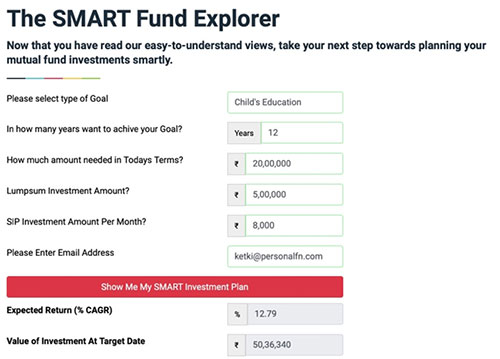

Use the SMART Fund Explorer:

Analyzing the different qualitative and quantitative parameters and planning & implementing your mutual fund investment can be overwhelming, especially for first-time mutual fund investors. At PersonalFN, we understand that not everyone can have the expertise to do the required exercise or enough time to learn the nuances of the market.

Hence, to make your mutual fund investment journey easier yet successful, we have introduced a SMART Fund Explorer that can help you plan your mutual fund investments smartly to achieve your goal of creating a child's higher education corpus.

All you need to do is, visit the SMART Fund Explorer, state your financial goal as 'Child's Education', determine a suitable time frame for achieving your goal based on the child's age, insert the amount you need in today's terms for their higher education, and lumpsum and/or SIP investment you can afford to make. Once you enter all the details correctly, click on "Show Me My SMART Investment Plan".

Considering the details entered, the SMART Fund Explorer will provide you with the expected return (%CAGR) and value of the investment at the target date (which is calculated considering a nominal inflation rate).

This is how the SMART Fund Explorer will look like once you enter all the details:

As you scroll down, you will see two mutual fund investment plans (Plan A and Plan B) offered by SMART Fund Explorer. The plans specifically show the fund categories you should invest in, the asset allocation percentage, potential returns of each category, and weighted annual return contribution. You can choose any of the plans based on your risk profile.

Moreover, you can get instant access to the list of best-suitable mutual fund schemes as per your selected plan by signing up PersonalFN's SMART Fund Explorer. The list of smartly selected and recommended mutual funds by our research team will serve as an opportunity to begin your mutual fund investment journey Smartly.

To conclude:

PersonalFN's SMART Fund Explorer is a brilliant tool that can help you invest in the best mutual funds to accomplish your goal of providing quality education to your child. But instead of just putting your money into the financial plan, make sure you review your portfolio periodically (at least once a year) to make the necessary adjustments if required and keep track of the growth of your investment. It is advisable to keep your child as a nominee for all the savings and investments made for their future so that no one can use these funds for any other requirement in your absence.

To ensure you do not liquidate investments made for your child's higher education during a financial emergency, make adequate provision for contingencies and buy adequate life insurance and health insurance coverage.

KETKI JADHAV is a Content Writer at PersonalFN since August 2021. She is an MBA (Finance) and has over seven years of experience in Retail Banking. Ketki specialises in covering articles around banking, insurance, personal finance, and mutual funds and has been doing it for over three years now.