6 NBFCs Offering Better Interest on Fixed Deposits

Mitali Dhoke

Nov 07, 2022

Listen to 6 NBFCs Offering Better Interest on Fixed Deposits

00:00

00:00

Fixed Deposits have long been unable to provide decent returns that can even meet inflation. Also, there have been more attractive investment options available in the market that can help in wealth creation faster. During the last 10 years, fixed deposit (FD) investors saw their returns declining drastically from the highest interest rate level of 9% offered in 2014 to 5.4% and below since 2020. Decadal low FD interest rates were a cause of huge financial stress for people like senior citizens whose primary source of regular income comes from FDs. Nevertheless, eventually, there are signs of good days ahead, as banks and NBFCs (Non-banking financial institutions) have started to increase FD interest rates, albeit marginally.

Fixed Deposits are a good option for conservative/risk-averse investors, who may require funds in short to medium term to fulfil their goals. Additionally, given the uncertainty and volatility in the equity market on the back of macroeconomic factors and geopolitical tensions, fixed deposits ensure the utmost safety of your invested capital. The principal amount invested in Fixed Deposits (FDs) doesn't fluctuate like the capital invested in equities or Mutual Fund (MF) schemes or any market-linked investment avenues.

Consequently, the interest rates on FDs are now fast changing. So is it the right time to go back to basics and invest in FDs as our parents did? Let us discuss the current FDs interest rate scenario.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

Why are interest rates on Fixed Deposits increasing?

The rising inflation has been a cause of concern not only for the Indian economy but across the globe. As a result of the rising inflation, several countries have hiked their policy rates in an effort to curb it and stabilise the economy.

The policy rate hike cycle, which started for India in May 2022, has continued since then, and the cumulative increase in rates by the central bank is 190 bps till the last Monetary Policy Committee (MPC) meeting. This has largely been driven by the fact that inflation does not seem transitory, and the rate hike will assist in taming the soaring inflation. Thus, the RBI has raised interest rates by almost by 1.9% in a short period of time.

Table 1: RBI Repo Rate History

| Month |

% Change in Rates |

Repo Rate |

| September 2022 |

0.50 |

5.90% |

| August 2022 |

0.50 |

5.40% |

| June 2022 |

0.50 |

4.90% |

| May 2022 |

0.40 |

4.40% |

| Total |

1.90 |

|

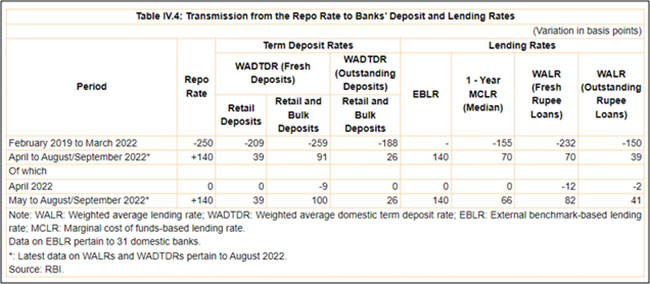

Repo Rate is the interest rate at which the central bank of a country lends money to commercial banks and helps to maintain liquidity in the market and manage cash flow in the economy. The Monetary Policy Committee (MPC) of the RBI convenes bi-monthly to make changes to the repo rate according to prevailing economic conditions. Notably, any change in RBI's repo rate will have an impact on the lending and deposit rates of the bank. When policy rates start rising, the lending rates see quicker transmission, while the rate transmission is slower in Deposit rates.

(Source: RBI Monetary Policy Report - September 2022)

(Source: RBI Monetary Policy Report - September 2022)

A fact is that while the RBI has raised policy rates straight for 4 times in a row in 2022, bank deposit rates still haven't increased in congruence; there is a lag - particularly in the case of retail deposits. As there was sufficient liquidity available in the system, banks/NBFCs did not feel the need to lure investors by raising deposit rates much.

However, the recent changes in policy rates announced by the RBI have impacted the bank's fixed deposit. While a number of banks have revised interest rates on fixed deposits in the past three weeks, Non-banking Financial Companies (NBFCs)/Housing Finance Companies (HFCs) are not far behind.

Should you consider investing in Fixed Deposits by NBFCs?

NBFC (or Non-banking Financial Company) is a registered company regulated by the Reserve Bank of India under the RBI Act of 1934. If you want to grow your savings with an NBFC fixed deposit, choose a registered NBFC. In general, NBFCs offer higher interest rates than bank fixed deposit interest rates, and this is due to the credit risk that is associated with NBFCs.

Although FDs by NBFCs offer a higher interest rate, the investor must be aware of the risks it carries. Bank FDs are considered safer, especially as each depositor is insured up to a maximum of Rs 5 lacs for both principal and interest amounts held by them in the bank FD. This ensures that the investors' deposits remain secured even if a bank faces liquidation. Fixed deposits by NBFCs, on the other hand, do not offer any such cover. In addition, Fixed deposit by NBFCs have a higher credit risk or default risk than bank FDs.

Given that, the credit rating agencies such as CRISIL and ICRA award safety ratings to different NBFCs, based on their reputation and credentials. NBFC fixed deposits with ratings of AAA from credit rating agencies like CRISIL, CARE, and ICRA are considered safer deposits with low risk. When investing in fixed deposits, to avoid losing on your interest payments or principal; it is best to select NBFCs with a strong reputation and high safety ratings.

The average rate of interest for bank FDs earlier was in the range of 2.75% to 6% on average. As a result, senior citizens are unhappy with their return on bank deposits even though Senior citizen FDs are provided with slightly higher interest rates. Recently, the hike in rates by RBI has translated most banks and NBFCs to revise the interest rates offered on FDs across various tenures.

Table 2: List of NBFCs offering Higher Revised Interest Rates (w.e.f October 2022)

| NBFCs |

Tenure (in months) |

FD Interest rates for Individuals (p.a) |

Ratings |

| For general citizens (%) |

For senior citizens (%) |

| HDFC Ltd. |

12-23 |

6.35 |

6.60 |

FAAA/Stable by CRISIL and MAAA/Stable by ICRA |

| 24-35 |

6.65 |

6.90 |

| 36-59 |

6.85 |

7.10 |

| Bajaj Finance |

12-23 |

6.55 |

6.80 |

FAAA/Stable by CRISIL |

| 24-35 |

7.25 |

7.50 |

| 36-60 |

7.40 |

7.65 |

| Mahindra Finance |

12 |

6.25 |

6.50 |

CARE AAA/Stable |

| 24 |

6.60 |

6.85 |

| 36 |

7.25 |

7.50 |

| ICICI Home Finance |

12-18 |

6.15 |

6.40 |

AAA/Stable by CRISIL, ICRA and CARE |

| 18-24 |

6.40 |

6.65 |

| 24-36 |

6.70 |

6.95 |

| LIC Housing Finance |

12 |

6.75 |

7.00 |

AAA/Stable by CRISIL |

| 24 |

7.00 |

7.25 |

| 36 |

7.25 |

7.50 |

| Shriram Transport Finance |

12 |

7.00 |

7.50 |

AA+/Stable by ICRA |

| 24 |

7.50 |

8.00 |

| 36 |

8.05 |

8.55 |

(Source: PFN Research)

As mentioned above, these are the few NBFCs offering higher interest rate across tenures. The FD rates in several banks are still around 5.5-6% p.a, indicating it is well below the inflation rate. It will be a few more months before FD rates reach the current inflation rate. Globally, inflation is still high due to multiple reasons, from supply-side constraints to the ongoing Russia-Ukraine war. So, the possibility of another rate hike in December 2022 is imminent. Also, the liquidity conditions in the market are expected to remain tight for the next few months. Thus, there is a good chance that the FD interest rates will increase in the coming months.

Amongst the corporate/NBFC deposits, consider the AAA-rated ones as mentioned in the table above, typically HDFC Ltd., Bajaj Finance, Mahindra Finance, ICICI Home Finance, and LIC Housing Finance. Given that the interest rates for senior citizens are slightly higher, they may consider investing in these fixed deposits with a suitable tenure. Ensure that you invest in fixed deposits based on your risk tolerance level, your investment horizon and objectives. If one is willing to take a bit higher risk, then the AA+(stable) rated fixed deposits can also be considered. You may consider the Shriram Transport Finance FD, which is currently assigned an AA+(stable) rating by ICRA.

However, do keep in mind that inflation and taxation may considerably dwarf your fixed deposit returns. Thus, unless FD real returns (i.e., returns post-taxation) beat the inflation rate, they will not turn out to be a worthy investment in the true sense. An investor needs to make a sound decision while investing in fixed deposits, especially when the interest rate cycle is an uptrend. Since FD rates stand to change if RBI increases the repo further, you may stand to lose if you lock your corpus in a long-term FD in one go. You may consider a strategic way of investing in FDs which is called FD laddering.

FD Laddering is a way of staggering out your investment into multiple fixed deposit accounts to earn high returns. This means that the corpus is invested in multiple tranches at every interest rate hike. This will not only help in benefiting from the additional interest rate hikes and getting average returns but will also allow liquidity to a certain extent.

To conclude...

Fixed Deposits' interest rate hike is good news for risk-averse investors and has come after a very long gap, where the interest rates on FDs were quite low to the point of being insignificant. FDs are viewed as risk-free investments by many investors. It's true that the principal amount in FDs remains stable, and investors earn a fixed interest rate during the investment period. However, as mentioned earlier, FDs are not completely risk-free and the inflation inefficiency of FDs over time hinders wealth accumulation.

Since Fixed Deposits provide capital safety; investors should consider FDs as one of their investment options rather than the only means of accumulating wealth. Even if FD returns are nominal compared to other dynamic investment avenues, they are still a good addition to an investment portfolio to spread the risk and earn risk-free returns. When planning your savings, it is important to consider your own goals. Whether you are considering a bank or NBFCs Fixed Deposit, make sure you research thoroughly and choose a plan that meets your requirements.

Warm Regards,

Mitali Dhoke

Research Analyst