Will the New Year 2024 See Home Loan Rates Going Down

Ketki Jadhav

Jan 16, 2024 / Reading Time: Approx. 5 mins

Listen to Will the New Year 2024 See Home Loan Rates Going Down

00:00

00:00

A home loan serves as a vital instrument for many individuals to achieve their dream of homeownership. However, the substantial interest payments on these loans over the years can strain one's finances. The affordable housing sector is facing challenges, with the Equated Monthly Instalments (EMIs) for home loan customers increasing by approximately 20% in 2022 and 2023, surpassing the principal loan amount.

Despite these challenges, there is an expectation for 2024 that interest rates may potentially decrease by 0.5-1.50%. This expected decline is primarily anticipated because of the expected initiation of Repo Rate cuts by the Reserve Bank of India (RBI), driven by a decrease in retail inflation acting as a catalyst.

The term "Repo," derived from 'Repurchase Option' or 'Repurchase Agreement,' denotes the interest rate at which commercial banks borrow funds from the central bank, i.e. the RBI. The RBI uses the Repo Rate as a tool to regulate inflation within the country. In response to inflationary pressures in the market, the RBI increases the Repo Rate. The increased Repo Rate creates challenges for banks seeking to borrow from the central bank, leading to a reduction in the money supply in the market-a measure that helps counteract inflation. Nevertheless, the consequence is a surge in borrowing costs for banks, contributing to an increase in interest rates for retail loans with variable interest rates.

Here is the record of the past Repo Rates and RBI's Monetary Policy Stance in India from 2019-23:

Table: RBI's Monetary Actions in 2019-23

| Month |

Repo Policy Rate |

Policy Action (Basis points) |

Monetary Policy Stance |

| Feb-2019 |

6.25% |

-25 |

Neutral |

| Apr-2019 |

6.00% |

-25 |

Neutral |

| Jun-2019 |

5.75% |

-25 |

Accommodative |

| Aug-2019 |

5.40% |

-35 |

Accommodative |

| Oct-2019 |

5.15% |

-25 |

Accommodative |

| Dec-2019 |

5.15% |

Status quo |

Accommodative |

| Feb-2020 |

5.15% |

Status quo |

Accommodative |

| Mar-2020 (an exceptional off-cycle meeting) |

4.40% |

-75 |

Accommodative |

| May-2020 (an exceptional 2nd off-cycle meeting) |

4.00% |

-40 |

Accommodative |

| Aug-2020 |

4.00% |

Status quo |

Accommodative |

| Oct-2020 |

4.00% |

Status quo |

Accommodative |

| Dec-2020 |

4.00% |

Status quo |

Accommodative |

| Feb-2020 |

4.00% |

Status quo |

Accommodative |

| April-2021 |

4.00% |

Status quo |

Accommodative |

| June-2021 |

4.00% |

Status quo |

Accommodative |

| Aug-2021 |

4.00% |

Status quo |

Accommodative |

| Oct-2021 |

4.00% |

Status quo |

Accommodative |

| Dec-2021 |

4.00% |

Status quo |

Accommodative |

| Feb-2022 |

4.00% |

Status quo |

Accommodative |

| Apr-2022 |

4.00% |

Status quo |

Accommodative |

| May-2022 (Off-cycle meeting) |

4.40% |

+40 |

Accommodative |

| June-2022 |

4.90% |

+50 |

Focus on withdrawal of Accommodative stance |

| Aug-2022 |

5.40% |

+50 |

Focus on withdrawal of Accommodative stance |

| Sep-2022 |

5.90% |

+50 |

Focus on withdrawal of Accommodative stance |

| Dec-2022 |

6.25% |

+35 |

Focus on withdrawal of Accommodative stance |

| Feb-2023 |

6.50% |

+25 |

Focus on withdrawal of Accommodative stance |

| Apr-2023 |

6.50% |

Status quo |

Focus on withdrawal of Accommodative stance |

| Jun-2023 |

6.50% |

Status quo |

Focus on withdrawal of Accommodative stance |

| Aug-2023 |

6.50% |

Status quo |

Focus on withdrawal of Accommodative stance |

| Oct-2023 |

6.50% |

Status quo |

Focus on withdrawal of Accommodative stance |

| Dec-2023 |

6.50% |

Status quo |

Focus on withdrawal of Accommodative stance |

Data as of January 16, 2024

(Source: RBI Monetary Policy Statements, Data Accumulated by PersonalFN)

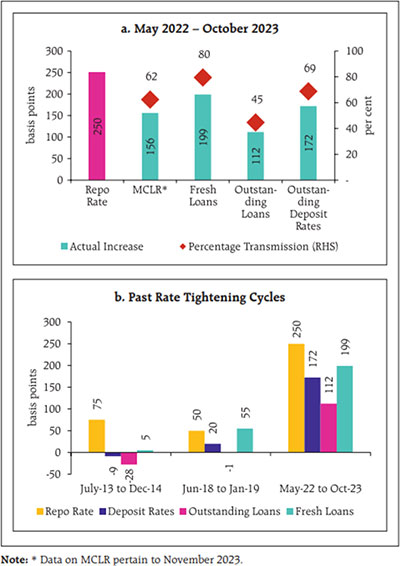

Note, there has been lags in monetary policy transmission. Nevertheless, the RBI in its latest Financial Stability Report observe, Monetary policy transmission to bank lending and deposit rates has been stronger in this cycle compared to previous cycles.

Graph: Monetary Policy Transmission to Bank Lending and Deposit Rates

(Source: RBI Financial Stability Report, December 2023)

(Source: RBI Financial Stability Report, December 2023)

In contrast to countries like the United States, where a majority of individuals prefer fixed interest rates that remain constant throughout the loan period, a significant number of home loan borrowers in India opt for floating interest rates. These rates can fluctuate based on changes in monetary policy. When interest rates decrease, borrowers with variable interest rate loans can experience the advantage of lower EMIs, making loan repayment more manageable. However, this flexibility also implies that they may face the prospect of higher interest rates in the long run if rates increase in the future.

A rise in home loan interest rates corresponds to an increase in the EMI amount. This heightened monthly repayment obligation can impose a challenging financial burden on the borrower. To alleviate this burden, borrowers have the option to extend their home loan tenure. This extension reduces the monthly repayment amount, easing the financial strain. Many banks in India have a practice of automatically extending loan tenures as interest rates rise, often without informing the borrowers. Nevertheless, this extended loan tenure places a prolonged EMI burden on borrowers, potentially leading to continued payments even after their retirement.

Since May 2022, the RBI has been incrementally raising the Repo Rate as a measure to manage inflation and stimulate economic growth. The series of Repo Rate hikes started in May 2022 and continued until February 2023, resulting in a cumulative increase of 2.5%. Consequently, all lending institutions were obligated to raise their interest rates. This upward adjustment has led to a corresponding rise in home loan interest rates, impacting the equated monthly instalments of home loan borrowers.

However, now inflation has noticeably subsided, and the likelihood of a substantial resurgence seems unlikely. As a result, many experts foresee the RBI initiating a reduction in the Repo Rate, potentially commencing in the second quarter of 2024 or perhaps by June or July. This projection is grounded in various contributing factors.

Why are experts expecting a reduction in the Repo Rate and thus in the home loan interest rates?

A significant factor behind the expectation of the reduction in the Repo Rate is the anticipated slowdown of inflation. Moreover, on a global scale, there is an expectation of an easing interest rate cycle, set to commence between March and May in two major economic blocks, the USA and Europe. As you may know, China has already started easing interest rates.

The Reserve Bank of India is expected to consider rate cuts when there is evidence that the Consumer Price Index (CPI) inflation is moving towards the targeted 4%. The decision to implement a rate cut requires majority approval from the six-member Monetary Policy Committee (MPC), which could potentially occur in the first half of 2024, paving the way for rate cuts in the second half of 2024.

So, Home loan borrowers need to exercise patience in the initial months of the year. Rate reduction and any potential reduction in home loan interest rates are not expected to happen in the near future, with indications suggesting that it is likely to take place around the middle of the year 2024.

With that said, with a Repo Rate cut, home loan EMIs would gradually decrease, but the timing depends on the transmission mechanism adopted by your lender. Some lenders may swiftly adjust rates, while others might take a longer duration.

Furthermore, home loan borrowers are categorised based on the nature of the lender. Those who have secured their loans from banks may fall under various interest rate regimes such as BPLR, Base Rate, MCLR, or EBLR. Borrowers from Non-Banking Financial Companies (NBFCs) or Housing Finance Companies (HFCs) operate under a different regime. Hence, the pace and extent of the rate cut will differ across these diverse interest rate structures.

Experts are expecting a reduction in home loan interest rates in 2024 in the range of 0.5% and 1.5%, depending once again on your lender and loan type. Some lenders may pass on only a portion of the repo rate cut, while others may offer more competitive rates to attract new borrowers.

To conclude:

Due to the RBI's Repo Rate hikes to manage inflation, the surge in equated monthly instalments (EMIs) for home loan customers in the last couple of years has placed financial strain on borrowers. However, a turning point may be on the horizon as experts expect a potential reduction in interest rates, driven by expected repo rate cuts by the RBI in the coming months.

2024 holds the promise of potential relief for home loan borrowers. Happy Planning!

We are on Telegram! Join thousands of like-minded investors and our editors right now.

KETKI JADHAV is a Content Writer at PersonalFN since August 2021. She is an MBA (Finance) and has over seven years of experience in Retail Banking. Ketki specialises in covering articles around banking, insurance, personal finance, and mutual funds and has been doing it for over three years now.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.