How Government Borrowings Would Impact Your Debt Mutual Funds

Rounaq Neroy

Mar 22, 2024 / Reading Time: Approx. 9 mins

Listen to How Government Borrowings Would Impact Your Debt Mutual Funds

00:00

00:00

The interest rates in the Indian economy, as you may know, are near the peak. In FY24 the RBI, so far, has maintained a status quo on the repo policy rate (at 6.50%) as CPI inflation -- barring the spike in July and August 2023 -- broadly remained within the comfort range.

Graph 1: CPI inflation Has Moderated

Data as of February 2024

Data as of February 2024

(Source: RBI, MOSPI)

However, the elevated interest rate environment has nudged the central government to reduce its borrowings. For the fiscal year 2024-25, as per the Interim Budget announcement, both the gross and net market borrowings through dated securities are estimated at Rs 14.13 trillion and 11.75 trillion, respectively.

Table: Government's Gross and Net Market Borrowing

| Fiscal Years |

Projected Gross Borrowing (Rs Tn) |

Project Net Borrowing (Rs Tn) |

| 2023-24 |

15.43 |

11.80 |

| 2024-25 |

14.13 |

11.75 |

| Change |

-8.4% |

-0.4% |

Data as of February 2024

(Source: Budget Speech of the respective years)

Now, both these numbers are less than for fiscal year 2023-24, as seen in the table above. The government borrowing during the pandemic years hit a record (of Rs 14.21 trillion) as expenditure rose amid the challenges thrown.

However, perhaps being conscious of the cost of borrowing involved and now that private investments are happening at scale, the government has lowered its market borrowing numbers. This, according to Finance Minister Ms Nirmala Sitharaman, potentially shall not just help larger availability of credit for the private sector but also keep lending rates under check.

What Does Lower Government Market Borrowing Mean for Debt Markets?

You see, the government characteristically is the largest borrower in the Indian debt market. The public sector entities are mandated to invest in Government securities (G-secs).

The market borrowings provide guidance or direction to bond yields. Given the direct correlation between yields and interest rates, it also sets the tone for interest rates.

Simply put, when the government borrowing is high (which means supply is also high), the yields also move up, and interest rates remain elevated. However, when borrowing is lower (which appears to be the case in fiscal year 2024-25), bond yields and interest rates are also expected to decrease.

Since yields and bond prices share an inverse relation, the government's low market borrowing is likely to press down the benchmark 10-year G-sec yield and drive the price of the bond up.

Effectively, the institutions that intend to borrow from debt markets would issue their debt securities at lower coupon rates. This, in turn, shall reduce their borrowing cost (by way of interest) turning out to be a favourable scenario, particularly for the private players.

The Effect on Debt Mutual Funds

Given that debt mutual funds are influenced by bond yields and interest rates, lower market borrowing of the central bank government -- which means less supply of government securities -- also has a bearing on the debt mutual funds.

Typically, the debt mutual funds that would be impacted positively the most in a scenario of softening yields and interest rates would be ones investing in longer-maturity debt papers. In this case as well, the ones already invested in the ongoing longer maturity debt papers would benefit more than a fresh investment in new debt paper.

Which Type of Debt Mutual Funds Would Benefit?

Well, out of the 16 sub-categories of debt mutual funds, the ones to benefit as yields soften are mainly:

But keep in mind that your investment will not be 100% risk-free or safe (as in the case of a Bank FD with a robust bank), as debt mutual funds are essentially market-linked investment products.

That being said, government securities are by and large, risk-free compared to debt papers issued by private institutions. In the past, as you may know, there have been instances of negative credit surprises or defaults on private debt papers that have negatively impacted debt mutual funds. Hence, as an investor, make sure to carefully evaluate the underlying portfolio of the debt funds before investing and not just go by the historical returns.

[Read: Best Debt Mutual Fund Categories for 2024]

If you are already holding some of the best debt mutual funds from the above categories, you could earn better returns as yields soften as an effect of lower market borrowing by the government.

If you are planning to make fresh investments into the aforesaid sub-categories of debt mutual funds, consider deploying the money before interest rates begin to descend. In the upcoming financial year 2024-25, the RBI is likely to cut policy interest rates (to support growth) if CPI inflation reduces further.

Having said that, when investing, make sure you are considering your risk appetite, broader investment objective, and liquidity needs and that they align well with such debt mutual funds.

When investing in Dynamic Bond Funds and Medium-to-Long Duration Debt Funds, ensure you have a time horizon of at least 3 to 5 years. For Long Duration Debt Funds at least 5 to 7 years, and in the case of Gilt Funds, a slightly longer investment horizon.

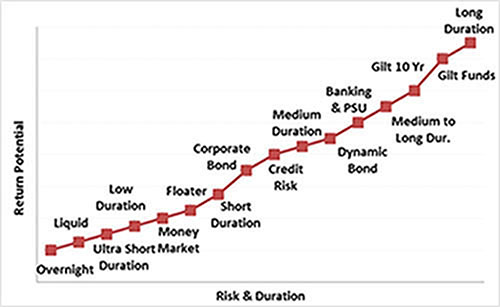

Graph 2: Risk-Return Spectrum of Debt Mutual Funds

For illustration purposes only.

For illustration purposes only.

(Source: PersonalFN Research)

Given that every type of debt mutual fund occupies a distinct place on the risk-return spectrum, you also ought to be mindful of the expected risk exposure. In the case of Dynamic Bond Funds, Medium-to-Long Duration Debt Funds, Long Duration Funds, and Gilt Funds, by and large, you should be willing to assume a moderate-to-high risk.

What About the Taxation of Debt Mutual Funds?

While those who have already invested in the aforesaid debt mutual funds may have earned capital gains, do note that with effect from April 1, 2023, the capital gain arising at the time of redemption -- whether short-term (a holding period of less than 36 months) or long-term (a holding period of 36 months and above) -- is taxed as per investors' tax slab.

The indexation benefit that earlier helped to make the most of the inflation impact on the purchase value of the investment and effectively reduced the LTCG tax liability is now no longer available for Debt Mutual Funds.

[Read: Debt Mutual Funds are Now at Par with Fixed Deposits for Taxation]

As a resident Indian, you have opted for the dividend option (now known as the IDCW option), any dividends received will added to your total income, under the head 'Income From Other Sources' in the computation of total taxable income, and taxed as per you income-tax slab, i.e. as per the marginal rate of taxation (plus the surcharge and cess as applicable). That said, if the dividend amount is more than Rs 5,000 in a financial year, then Tax Deduction at Source (TDS) will be first done (as per Section 194K of the Income Tax Act, 1961) at the rate of 10%.

If you are an NRI investor, the capital gains on debt-oriented mutual funds are subject to Tax Deduction at Source (TDS) at the rate of 20% for LTCG and 30% for STCG. The dividend received by the NRI will be taxed at the rate of 20% (plus the surcharge and cess as applicable).

To sum-up...

Debt as an asset class plays an important role in one's portfolio. Make sure you are strategically investing in debt mutual funds, considering where interest rates and yields are headed. Don't just invest in debt mutual funds looking at historical returns and star ratings. Watch this video to know why you should avoid investing in 5-star or top-rated mutual funds.

Be a thoughtful investor and invest sensibly in debt mutual funds.

To know how much to allocate to debt and align the investments with your envisioned financial goals, speak to your SEBI-registered investment advisor.

Happy Investing!

Note: This write-up is for information purposes and does not constitute any kind of investment advice or a recommendation to Buy / Hold / Sell a fund. Mutual Fund Investments are subject to market risks, read all scheme-related documents carefully before investing.

We are on Telegram! Join thousands of like-minded investors and our editors right now.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.