RBI Holds Repo Rate at 6.50% Again. Here’s Why You Should Invest in Bank FDs Now

Rounaq Neroy

Dec 13, 2024 / Reading Time: Approx 8 mins

Listen to RBI Holds Repo Rate at 6.50% Again. Here’s Why You Should Invest in Bank FDs Now

00:00

00:00

In the last bi-monthly monetary policy held on 6 December 2024, the six-member Monetary Policy Committee (MPC) of the Reserve Bank of India (RBI), decided to maintain the benchmark repo rate steady at 6.50%.

Consequently, the Standing Deposit Facility (SDF) rate remained unchanged at 6.25% and the Marginal Standing Facility (MSF) rate and the Bank Rate at 6.75%.

However, as a measure to address the liquidity in the system, the Cash Reserve Ratio (CRR) was reduced by 50 basis points (bps) to 4.00%.

The decision was made by a 4:2 majority, making this the 11th straight meeting where the RBI kept the rate unchanged.

Further, the MPC also decided to continue with a 'neutral' monetary policy stance and to remain unambiguously focused on a durable alignment of inflation with the target, while supporting growth.

---Advertisement ---

They Won’t Wait Much Longer…

You know that this is only for our premium members like yourself.

A chance to get your existing portfolio reviewed by our investment advisors.

Our advisors already have their plates full.

But they agreed to accept a few portfolios.

All you have to do is let us know in time that you are interested.

Click here to have our investment advisors call you.

----------------------------------------

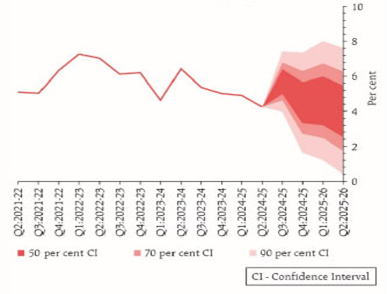

India's CPI inflation (also known as retail inflation) in October 2024 rose to 6.21% (a 14-month high) from 5.49% in the previous month, crossing the RBI's tolerance threshold of 6%. The spike in CPI inflation was mainly driven primarily by higher food prices. This was one of the main reasons for maintaining a status quo once again on policy rate.

Graph: RBI's Quarterly Projection of CPI

(Source: RBI's Bi-monthly Monetary Policy Statement, December 4 to 6, 2024)

(Source: RBI's Bi-monthly Monetary Policy Statement, December 4 to 6, 2024)

Going forward, according to the RBI, food inflation is likely to soften in Q4 with the seasonal easing of vegetable prices and kharif harvest arrivals, and good soil moisture conditions along with comfortable reservoir levels auguring well for rabi production. However, adverse weather events and the rise in international agricultural commodity prices pose an upside risk to food inflation. Even though energy prices have softened in the recent past, its sustenance needs to be monitored. Businesses expect pressures from input costs to remain elevated and growth in selling prices to accelerate from Q4.

Taking all these factors into consideration, CPI inflation for 2024-25 is projected by the RBI at 4.8% (with Q3 at 5.7%; and Q4 at 4.5%). The CPI inflation for Q1:2025-26 is projected at 4.6%, and Q2 at 4.0% (see Graph above). The risks are evenly balanced.

The RBI Governor Shaktikanta Das (whose term ended on December 10, 2024) in his statement said, "The MPC believes that only with durable price stability can strong foundations be secured for high growth. The MPC remains committed to restoring the inflation growth balance in the overall interest of the economy."

Taking cognisance of India's GDP growth slowed to 5.4% (the slowed pace in 7 quarters), the RBI also revised the GDP growth projection for FY25 to 6.6% (with Q3 at 6.8% and Q4 at 7.2%) from the earlier 7.2%. While the growth outlook appears to be resilient in the next year, close monitoring is warranted. According to the RBI, headwinds from geopolitical tensions, volatility in international commodity prices, and geoeconomic fragmentation continue to pose risks to the outlook.

Path to Interest Rates

Well, much depends on the CPI inflation trajectory. The recent spike in inflation highlights the continuing risks of multiple and overlapping shocks to the inflation outlook and expectations. Heightened geopolitical uncertainties and financial market volatility add further upside risks to inflation.

The MPC remains committed to restoring the balance between inflation and growth in the overall interest of the economy. The decision to continue with the neutral stance on the monetary policy provides the RBI flexibility in its monetary policy action to respond appropriately depending on incoming data -- mainly inflation and GDP growth.

The new RBI Governor, Sanjay Malhotra (who took charge on December 11, 2024) has said, "Stability in policy and continuity is very important. Decisions will be taken with public interest to preserve trust in this institution."

Investment in Bank Fixed Deposits

Note that, when there is an increase in the repo rate, banks typically increase the interest rates on bank fixed deposits (FDs). Conversely, a decrease in the repo rate usually translates to lower bank FD rates.

That being said, currently, it appears that we are almost near the peak of the current interest rate upcycle.

Between May 2022 and February 2023, the RBI increased the repo rate by 250 basis points (to tame inflation).

However, as the repo rate has remained stable since then, FD rates plateaued and seem unlikely to increase further in the near term. On the contrary, if inflation cools, the RBI may reduce rates going forward (possibly in the April bi-monthly monetary policy statement, 2025-26).

Thus, the current environment is favourable to invest in bank FDs, particularly for senior citizens and conservative/risk-averse investors. Locking in FDs now shall help benefit from prevailing high rates and earn a decent interest income.

Choosing the Ideal FD Tenure

FD tenures can range from as short as 7 days to as long as 10 years. In the current scenario, it is prudent to opt for shorter tenures - preferably not more than 2 years.

FDs with tenures of 6 months, 1 year, or 2 years provide a meaningful balance of returns, liquidity, and flexibility as per your needs.

At the present moment, locking in your hard-earned money for the long term in bank FD may not be ideal. You need to ensure that your investments keep pace with inflation over the long term.

If you need access to money during emergencies, choose short-term deposits (of 12 to 18 months tenure). Now, while some banks allow early withdrawal of FDs, it often comes with penalties and loss of interest, and therefore, that should not be the way to go about addressing emergency needs.

Here's a look at the interest rates across different public and private sector banks...

Table 1: PSU Bank FD Interest Rates (Rates in % p.a.)

| Banks |

6 Months |

1 Year |

2 Years |

| State Bank of India |

6.25 |

6.80 |

7.00 |

| Bank of Baroda |

5.75 |

6.85 |

7.00 |

| Indian Overseas Bank |

4.75 |

7.10 |

6.80 |

| Canara Bank |

6.15 |

6.85 |

7.30 |

| Union Bank of India |

5.00 |

6.80 |

6.60 |

Interest rates as of Dec 11, 2024

*For investment amounts less than Rs 3 crore

Note: The above list is not exhaustive and not recommendatory

(Source: Websites of respective banks)

Table 2: Private Bank FD Interest Rates (Rates in % p.a.)

| Banks |

6 Months |

1 Year |

2 Years |

| HDFC Bank |

4.50 |

6.60 |

7.00 |

| ICICI Bank |

4.75 |

6.70 |

7.25 |

| Axis Bank |

5.75 |

6.70 |

7.10 |

| Yes Bank |

5.00 |

7.25 |

7.25 |

| Kotak Mahindra Bank |

7.00 |

7.10 |

7.15 |

Interest rates as of: Dec 11, 2024

*For investment amounts less than Rs 3 crore

Note: The above list is not exhaustive and not recommendatory

(Source: Websites of respective banks)

Senior citizens can benefit from an additional 0.50% interest rate on bank FDs.

Keep in mind, that it's essential to exercise caution when considering banks offering significantly higher interest rates than the market average, as higher returns often come with higher risks.

It makes sense to diversify your investment in FDs across banks. As seen in Table 1 and Table 2 above, different banks offer varying interest rates. By diversifying your investments, you can take advantage of higher rates from certain banks while spreading your risk.

Further note that deposits of up to Rs 5 lakhs are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC), per bank per depositor. By diversifying, you can ensure all your deposits fall within the insured limit, minimising risk.

To make the most of your investment and maintain liquidity, Fixed Deposit laddering is a smart strategy. It involves spreading your FD investments across multiple maturity tenures or maturity buckets (e.g. 6 months, 1 year, 2 years) rather than locking all your funds in a single FD. With this approach, you can potentially secure higher returns while ensuring liquidity to cover emergency expenses, without needing to prematurely break long-term deposits.

Tax Implications of Investing in Bank FDs

Interest earned on FDs is considered "Income from Other Sources" and is taxed according to the applicable income tax slab.

Banks deduct TDS at 10% if the total interest earned exceeds Rs 40,000 in a financial year (Rs 50,000 for senior citizens). If you haven't provided your PAN, TDS will be deducted at 20%.

If your income is below the taxable limit, submit Form 15G (for non-senior citizens) or 15H (for senior citizens) at the beginning of the financial year to the respective bank/s to avoid TDS.

Additionally, senior citizens can claim a deduction of up to Rs 50,000 interest income, under Section 80TTB of the Income Tax Act, 1961.

To Conclude...

With the RBI maintaining the repo rate at 6.50% and FD interest rates plateauing, this is an opportune time to lock in prevailing high rates, particularly for senior citizens and conservative/risk-averse investors.

If you follow a thoughtful approach and astutely invest in bank FD now while interest rates are high and almost peaked, you will be able to earn a respectable sum as interest, address your liquidity needs, and add to your financial security.

And as always, it's important to stay mindful of the tax implications and ensure investments are aligned with financial goals and risk tolerance.

Happy investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing.

This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes.