Retirement Planning: What Should Be Your Asset Allocation Amid High Inflation

Mitali Dhoke

Apr 05, 2023 / Reading Time: Approx. 7 mins

Listen to Retirement Planning: What Should Be Your Asset Allocation Amid High Inflation

00:00

00:00

Inflation is one of the most unsettling economic conditions for investors. The future is hazy, and the only certainty is that our purchasing power will dwindle. This makes investing even more difficult since the usual strategy of investing when the market is cheap and staying out when it is expensive is more difficult to execute in an inflationary climate.

Prices have been rising on everything from food to housing. In February 2023, the Consumer Price Index (CPI), which measures the prices of goods and services, increased to 176.80 points from 176.50 points in January 2023. CPI notched a 6.4% increase in the past one-year period from 166.10 in February 2022.

While inflation is typically connected with rising costs for travel, groceries, and other daily expenditures, many people may wonder: Will inflation affect my retirement nest egg?

Due to inflation, a rupee today can buy fewer groceries and other household staples than it could a year ago. Against the backdrop of high inflation, rising interest rates, recession threats as well as uncertainty over global economic growth, those building a retirement corpus need to consider the following things:

We all think of retirement as the 'golden years' of our lives, when we can sit back, relax, and enjoy the rewards of our hard work. A comfortable retirement, on the other hand, necessitates careful planning, especially since you will no longer have an active source of income. You may also have family responsibilities and other expenses to consider, and with post-retirement life expectancy ranging from 20 to 30 years, financial security for yourself and your family is critical.

Image source: www.freepik.com

Image source: www.freepik.com

Join Now: PersonalFN is now on Telegram. Join FREE Today to get 'Daily Wealth Letter' and Exclusive Updates on Mutual Funds

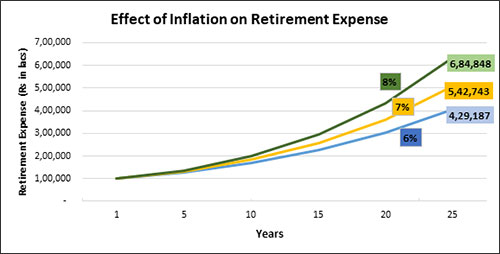

Consider that in retirement, even moderate inflation can drive your annual expenses up over time. Your expected retirement expenses are a key factor in deciding how much you may need to save for retirement. For instance, if you begin your retirement with an annual withdrawal of Rs 1 lac per annum, have a look at the graph to understand what your cost of lifestyle will be after 25 years from now at 3 different rates of inflation.

Graph: Determining the impact inflation costs to an individual's retirement expense

(Source: PersonalFN Research)

(Source: PersonalFN Research)

For illustration purpose only

Inflation is a hidden tax on your investment that gradually erodes the worth of money. When planning for retirement, failing to account for inflation can result in a large shortfall in your retirement corpus. Saving for an appropriate retirement corpus in today's high-inflation environment necessitates effective asset allocation, with equity investments being a significant concern.

How do equity investments assist in building an inflation-proof retirement corpus?

Traditional retirement investment strategies can help you accumulate the necessary corpus, but they are not enough to generate inflation-beating returns.

Mutual fund investments, especially in equities, are an excellent way to start your retirement planning since they assist you in selecting the ideal asset allocation and offer a diversified portfolio that enables you to produce long-term returns that outperform inflation. For example, imagine you require a retirement corpus of Rs 1 crore as on today. After 20 years, at a 7% inflation rate, you will need around Rs 3.61 crore. Thus, the more you delay investing, the more it lessens your possibility of reaching your retirement target.

[Retirement Calculator]

Equity is a valuable asset class that has the potential to outpace inflation in the long run, making it an attractive option for retirement planning. Do note that equities, unlike other asset classes, could help you accelerate towards your retirement goals through the power of compounding.

To ensure that your retirement corpus keeps pace with inflation, it's important that your investments earn at least inflation returns for the most conservative allocation. For example, on average, the inflation rate is 7%. Thus, the return should be at least in the range of 8%-10% post-tax and fees to preserve the purchasing power of your savings and compensate for the increasing cost of living.

Nevertheless, it's important to acknowledge that equity investments carry inherent risks. As such, when determining your asset allocation strategy, it's a crucial factor in your investment goals and risk tolerance levels.

How to choose the right asset allocation for your retirement corpus amid high inflation?

Your portfolio should be a mix of different assets; there should be an ideal equity-debt mix to achieve your retirement goals and secure your financial future. The allocation should be determined based on your risk tolerance, time horizon, cash-flow needs, and taxes.

The time-tested mantra of diversification can hold you in good stead at this point. Note that the effects of inflation on different asset classes are different. Diversification across financial instruments and asset classes like equity, debt, and gold can help your portfolio navigate choppy waters amidst inflation. Diversification during inflation is essential for achieving long-term returns in a low-risk manner.

For example, if you seek to invest in mutual funds, you can choose a mix of equity and debt funds. If you can stomach high risks, you can invest in a mix of large-cap and mid-caps. If your portfolio is tilted too much towards a particular asset class, rectify the same at the earliest. However, factor in your retirement goals and risk tolerance before investing. The right asset mix for retirement is about including equity instruments in a way that creates a balanced portfolio and delivers expected returns while mitigating risks. The earlier you start investing, the more space you have to include equity, earn better real returns, and beat inflation. For less time to maturity, you should focus on getting stable returns rather than higher returns. If the time to maturity is long, you can skew your portfolio more towards equity and can still navigate through short-term market noise while achieving better inflation-beating returns.

To conclude...

As a result, it is critical to start saving for retirement as soon as feasible. When it comes to retirement planning, effective asset allocation is critical, with equity investments having a significant role. However, keep in mind that there is no one-size-fits-all solution for picking an asset allocation mix. It is determined by the individual's goals and preferences. The aim should be long-term wealth creation.

With the beginning of the new financial year 2023-24, take a step towards retirement planning, or later it will become nearly impossible to maintain a good lifestyle post-retirement.

MITALI DHOKE is a Research Analyst at PersonalFN. She is an MBA (Finance) and a post-graduate in commerce (M. Com). She focuses primarily on covering articles around mutual funds including NFOs, financial planning and fixed-income products. Mitali holds an overall experience of 4 years in the financial services industry.

She also actively contributes towards content creation for PersonalFN’s social media platforms in the endeavour to educate investors and enhance their financial knowledge.