All You Need to Know about the Newly Launched Bharat Bond ETF 2032

Listen to All You Need to Know about the Newly Launched Bharat Bond ETF 2032

00:00

00:00

Edelweiss Mutual Fund has launched another scheme in the Bharat Bond series. The new fund offer (NFO) of Bharat Bond ETF will mature in 2032 and is open for subscription from December 03, 2021 to December 09, 2021. Earlier the fund house had launched Bharat Bond ETFs maturing in 2023, 2025, 2030, and 2031.

The minimum investment amount is Rs 1,000, and in multiples of Re 1 thereafter during the NFO period. A Demat account is mandatory to invest in Bharat Bond ETF – 2032. Investors who do not have a Demat account have an alternative to invest via Bharat Bond ETF Fund of Fund – 2032.

Bharat Bond ETF – 2032 will follow a buy-and-hold investment strategy tracking the constituents of Nifty Bharat Bond - April 2032 index. It will invest in AAA-rated (highest rating) public sector bonds maturing within 12 months prior to the maturity of the index.

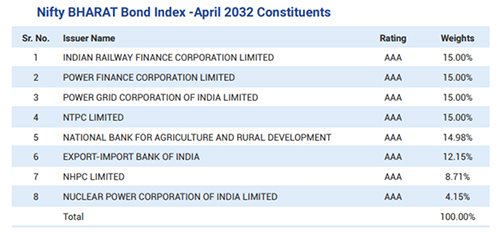

The index constitutes eight central public sector enterprises (CPSEs), such as Indian Railway Finance Corporation (IRFC), Power Finance Corporation, Power Grid Corporation, NTPC, NABARD, among others. The exposure to single entity is capped at 15% in the index.

Table: Constituents of Nifty Bharat Bond Index - April 2032

(Source: Bharat Bond ETF - April 2032 Presentation)

What are the benefits of investing Bharat Bond ETF – 2032?

1) Stable and predictable returns

Bharat Bond ETF – 2032 will hold securities till maturity. Therefore, the impact of mark-to-market loss on the fund will be low. The indicative yield of the underlying index, i.e. Nifty Bharat Bond - April 2032 index, is 6.87%. If you hold the scheme till maturity, your returns will be in line with the portfolio's current yield to maturity (YTM).

2) Low credit risk

The fund will invest in securities issued by public sector companies. These securities enjoy high credit rating since they have government backing. Therefore, from the credit quality perspective, these funds are relatively safe. The low credit risk makes Bharat Bond ETF – 2032 suitable for investors with a low-risk profile.

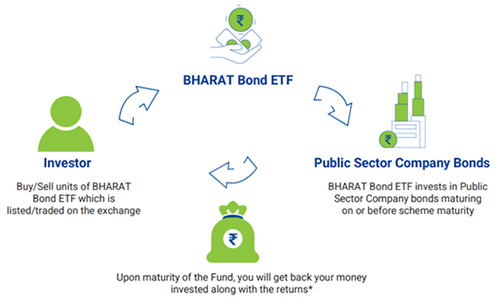

Illustration: How Bharat Bond ETF works?

(Source: Bharat Bond ETF - April 2032 Presentation)

3) Low cost of investment

Being a passively managed scheme, the cost of management of Bharat Bond ETF – 2032 is very low. The expense ratio of the ETF is just 0.0005%, whereas that of Fund of Fund is 0.05%.

4) Traded on exchanges

Bharat Bond ETF – 2032 is an open-ended scheme; therefore, it enjoys better liquidity compared to fixed maturity plans (FMPs) that are close-ended. Investors can purchase or redeem units on stock exchanges at any time.

5) Taxation efficiency

Bharat Bond ETF 2032 is more tax-efficient compared to traditional investments such as Bank FDs. Gains on Bharat Bond ETF – 2032 is taxable similar to other debt mutual funds. Investors in the highest tax bracket can benefit from indexation if they invest for 3 years or more. In this case, gains are taxable at 20% with indexation benefits. Indexation allows you to adjust the purchase price of your investment with inflation, and thereby lower your tax on returns. Gains on short-term investments (less than 3 years) are taxable as per your income tax slab.

(Image source: www.freepik.com)

What are the risks associated with Bharat Bond ETF – 2032?

As mentioned earlier, when you invest in Bharat Bond ETF – 2032, you will lower the impact of interest rate volatility if you hold it until maturity. However, if you redeem your units before the maturity date, your returns may be lower and can even expose you to capital loss, depending on the prevailing market conditions. Therefore, consider investing in Bharat Bond ETF – 2032 only if you can hold the investments until maturity.

Another disadvantage is that, interest rates are currently at a multi-year low, your investment will be locked-in at the current rate in the Bharat Bond ETF – 2032. Therefore, you would potentially earn lower returns than if you lock-in returns when the interest rates are high. That said, if you need to address a financial goal, you should not delay planning your investment.

Should you invest in Bharat Bond ETF – 2032?

Interest rates are currently at a multi-year low with the expectation of rise in inflation. It is expected the interest rates will start to climb upwards in the near future. However, when it will happen is unclear at this juncture.

Omicron, the latest variant of COVID-19, has compounded the uncertainty about the expectation of a hike in interest rate. In the current uncertain interest rate environment, it is advisable to invest in debt funds where the maturity of the portfolio matches your investment horizon.

Bharat Bond ETF – 2032 is offering a yield that is more attractive compared to the current interest rate on the fixed deposits of most banks with similar maturity. Additionally, investors can benefit from the low cost of investment and high quality of instruments in the portfolio. If you need to address a financial goal that has a time horizon similar to the maturity tenure of the scheme, you can consider investing in Bharat Bond ETF – 2032 as a part of fixed income portfolio.

If you have a shorter investment horizon, investors can consider Target Maturity Funds of varying maturity such as Edelweiss Nifty PSU Bond Plus SDL Index Fund - 2026 and ICICI Pru PSU Bond plus SDL 40:60 Index Fund - Sep 2027, etc.

If you do not have long term horizon, invest in shorter maturity debt funds, such as Liquid funds, Short duration funds, Banking & PSU debt funds, etc. or a combination of these.

Select debt mutual funds that invest predominantly in securities issued by the government and public sector entities. Refrain from investing in schemes where the debt fund manager engages in undue yield hunting. Lastly, remember that investment in debt mutual funds is not risk-free. Therefore, make it point to invest in congruence with your investment time horizon and risk tolerance.

If you are serious about building a winning debt fund portfolio I suggest subscribing to PersonalFN's DebtSelect. Under DebtSelect, we give high weightage to schemes displaying worthy portfolio characteristics. We avoid debt mutual fund schemes that aim for higher yields by taking undue credit risk with substantial exposure in instruments issued by private issuers.

With DebtSelect, you will get unrestricted access to our research team's analysis and recommendations on different types of debt funds, covering factors such as profile and suitability of the fund, performance and other aspects. PersonalFN's DebtSelect provides insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell.

Subscribe to DebtSelect today!

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds